- Lower grades clear at floor prices amid ample supply

- Sarda Energy emerges as top bidder, followed by Ultratech

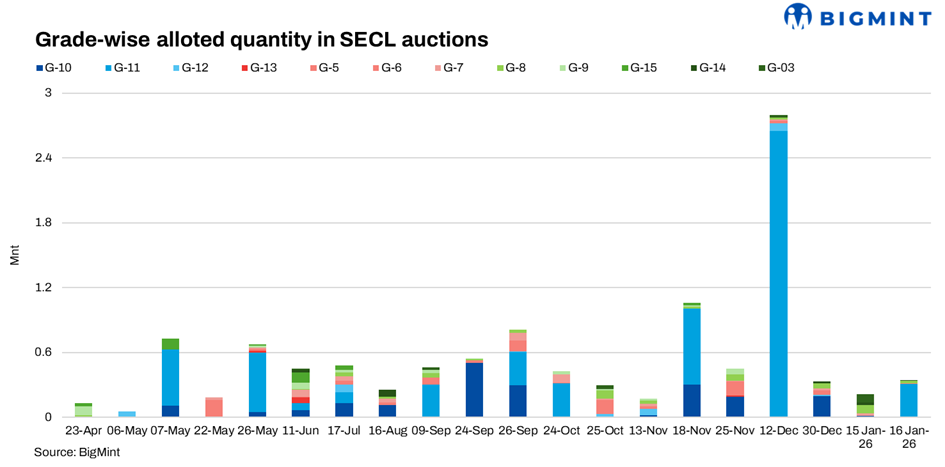

South Eastern Coalfields Limited conducted non-coking coal auctions on 15 and 16 January 2026, offering a combined 2,038,050 tonnes (t), with cumulative bookings of 556,750 t. On 15 January, SECL offered 806,050 t, of which 217,200 t were booked, while on 16 January, 1,232,000 t were offered, with allocations totalling 339,550 t. Buying remained selective, with clear divergence between mid-grade and lower-grade coal. Participants focused on grades with stronger industrial applicability, while floor-linked grades largely cleared without premiums, indicating adequate supply and cautious procurement.

15 Jan auction: Mid-grade strength contrasts with floor-linked clearances

On 15 January, SECL allocated 217,200 t. G3 emerged as the most sought-after grade, with 80,050 t sold at an average winning price of INR 4,472/t against a floor price of INR 4,128/t, translating into a premium of around 8.3% amid steady demand from sponge iron and industrial users.

From a buyer perspective, Sarda Energy and Minerals Limited led lifting with 40,000 t of G3. UltraTech Cement lifted 22,000 t across G3 and G7, while SMC Power Generation lifted 20,000 t of G8. Buying patterns reflected targeted procurement rather than volume accumulation.

Mine-wise, Churcha OC dominated allocations with 80,050 t of G3 at INR 4,472/t. Amgaon OC supplied 50,000 t of G8 at INR 4,066/t, while Rajendra UG delivered 17,500 t of G7 at INR 3,040/t. Overall, premiums were clearly concentrated in G3 and G8.

16 Jan auction: Bulk G11 clears near floor, selective premiums persist

The 16 January auction saw higher volumes, with 339,550 t allocated. G11 accounted for the bulk of sales, with 309,850 t clearing at an average winning price of INR 1,419/t against a floor of INR 1,418/t, indicating a marginal premium of around 0.1%. The outcome reflected ample availability and steady but non-aggressive demand.

Kusmunda OC dominated the auction, supplying the entire G11 volume of 309,850 t at INR 1,419/t. Beherabandh UG contributed G8 volumes at INR 2,980/t, while Kurja UG supplied G5 at INR 3,597/t.

Buyer participation was broad but fragmented. Jai Bhole Enterprises emerged as the largest buyer with 21,000 t of G11. Utkal Alumina lifted 16,000 t, while Global Minerals and Sagar Traders lifted 12,000 t each. UltraTech Cement lifted 6,400 t across G11 and G8, reflecting mixed-grade procurement.

Takeaway

The January SECL auctions highlighted a segmented domestic coal market. Mid-grade coal, particularly G3 and G8, continued to command meaningful premiums driven by industrial demand visibility. In contrast, bulk lower-grade and utility-linked coal cleared close to floor prices, reflecting comfortable supply and cautious buying behaviour. Overall, bidding remained disciplined, indicating controlled restocking rather than any demand-led rally.

Leave a Reply