- Sharp downtrend in downstream steel prices

- Bulk bookings expected in upcoming OMC auction

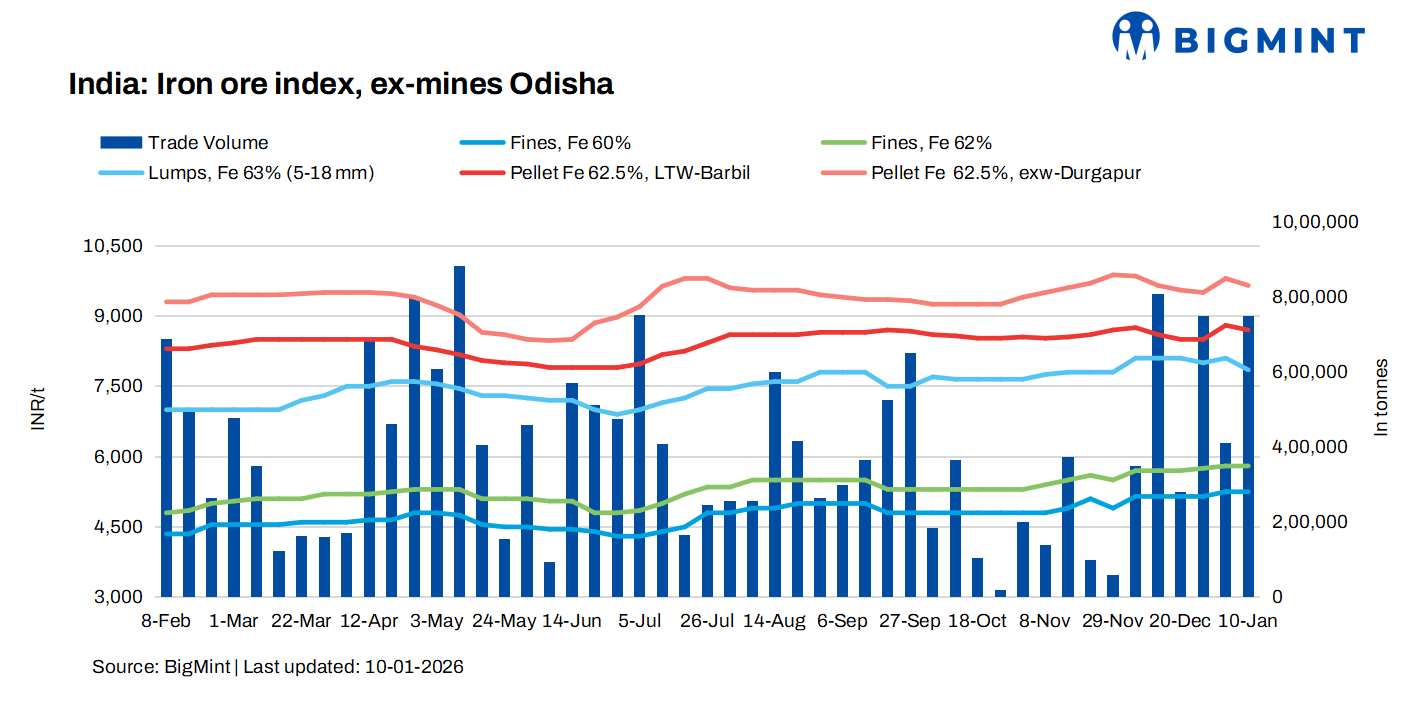

Iron ore prices in the Odisha market remained largely stable this week, as assessed on 10 January, particularly in the fines segment, while lump prices witnessed a slight correction following weakening seen in the downstream steel market. Market participants indicated that overall trade activity continued as buyers stocked up on need-basis, with bulk transactions largely absent during the week.

Price update

BigMint’s Odisha iron ore fines (Fe 62%) index remained stable w-o-w at INR 5,800/t ($64/t) ex-mines on Saturday. BigMint recorded deals for around 750,000 t this week, concluded directly by steelmakers. The major trades were concluded in the iron ore fines segment.

Market highlights

According to sources, miners revised their offers marginally, mainly reducing lump prices in response to reduced buying interest from steelmakers. An Odisha-based trader informed, “Lump demand has softened as sponge iron and semi-finished steel prices have been continuously declining after last week’s sharp hike. This has forced miners to adjust lump prices slightly.”

In contrast, demand for iron ore fines remained healthy. Several miners concluded active trades during the week, supported by steady consumption from pellet plants. A miner said, “Fines demand is comparatively strong, and buyers are regularly lifting material to meet their immediate production requirements. There is no inventory pressure as of now.”

Buyers, however, adopted a cautious stance, citing volatility in downstream prices. Sponge iron and billet prices have corrected sharply in recent days, prompting steelmakers to avoid aggressive raw material procurement. A sponge iron producer said, “We are purchasing only requirement-based quantities. We are waiting for clarity on steel prices.”

Some miners reported that buying interest remains firm despite cautious sentiment. Buyers are consistently booking material on a need basis, ensuring stable movement, especially in fines.

Meanwhile, a few buyers indicated that bulk bookings are likely to be seen in the upcoming OMC auction, particularly for higher-grade material. Another market participant said, “Bulk bids are expected in the next OMC auction, but currently only a limited number of buyers are active in the spot market.”

An exporter said that lower-grade iron ore prices saw a sharp upward trend over the last few days amid limited availability of materials and some active bookings for sourcing for pending export shipments.

Factors affecting iron ore prices

Pellet prices fall w-o-w: Pellet (6-20 mm, Fe 62.5%) prices in Odisha’s Barbil dropped by INR 100/t ($1/t) w-o-w at INR 8,700/t ($96/t) loaded to wagon on 10 January. Pellet (Fe 62.5%, 6-20 mm) prices in Durgapur fell by INR 200/t ($2/t) to INR 9,650/t ($107/t) exw.

Sponge iron prices down w-o-w: According to BigMint’s assessment, sponge iron C-DRI (FeM 80%) prices in Rourkela decreased by INR 800/t ($9/t) w-o-w to INR 25,000/t ($277/t) on 10 January.

Billet prices decline w-o-w: Meanwhile, steel billet (100*100 mm) prices in Rourkela decreased by INR 1,600/t ($18/t) w-o-w to INR 38,900/t ($431/t) on 10 January.

Rationale

- T1- Six (6) deals for Fe 62% fines were recorded in the publishing window, and three (3) were considered for price computation. These were given 50% weightage for index calculation.

- T2 – BigMint received twenty-two (27) offers and indicative prices under the T2 category (offers, indicative, and bids) in this publishing window. Seventeen (17) were taken into consideration and given 50% weightage. To check BigMint’s iron ore assessment, pricing methodology, and specification document, click here.

Outlook

Iron ore fines prices are expected to remain firm on steady demand. Lump prices may see a mild correction depending on downstream steel price movements.

Leave a Reply