- Around 2.5 mnt iron ore book in OMC auction

- New offers by miners expected in next week

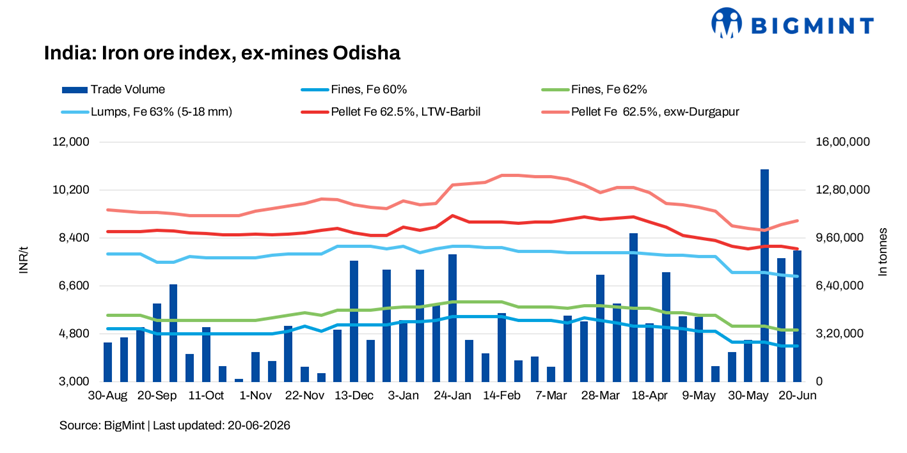

BigMint’s Odisha iron ore fines (Fe 62%) index remained stable w-o-w at INR 4,950/t ($52/t) ex-mines on 20 June 2026. Iron ore prices in the Odisha market have witnessed a decline of INR 100-200/t across the grades over the past week, driven by persistent weakness in the downstream steel sector and subdued buying activity from steelmakers.

Market activity remained healthy as steelmakers and traders actively booked material through auctions and private miners ahead of the approaching monsoon season.

Auction and deals:

OMC auctioned around 2.01 mnt iron ore fines (Fe 51-65%) on 19 Jun’26. Around 1.543 mnt (76%) iron ore fines received bids at INR 3,500-5,850/t with around INR 100/t premium on base prices. The weighted avg bids against last months rose by INR 50/t. Earlier, the miner inched down base prices by INR 50-100/t m-o-m.

In OMC’s auction for 1.14 mnt of iron ore lumps (Fe 60-65%) on 19 Jun’26, around 1.03 mnt (90%) were booked at INR 4,750-7,3-00/t, with premiums of upto 19% over base prices. Weighted average bids fell by INR 250/t m-o-m. Earlier, OMC had kept base prices stable for this month. The sharp decline in CDRI prices — by INR 1,000/t m-o-m to INR 25,200/t exw-Rourkela — led to the fall in bids.

BigMint recorded around 875,000 t iron ore deals ahead of the auction this week concluded by steelmakers via traders and miners.

Rationale

- T1- Five (5) deals for Fe 62% fines were recorded in the publishing window, and three (3) were considered for price computation. This was given 50% weightage for index calculation.

- T2 – BigMint received twenty one (21) offers and indicative prices under the T2 category (offers, indicative, and bids) in this publishing window. All were taken into consideration and given 50% weightage. To check BigMint’s iron ore assessment, pricing methodology, and specification document, click here.

Market highlights:

According to market participants, buying interest has been supported by seasonal inventory replenishment. Steelmakers are increasing their stock levels in expectation of logistical challenges during the rainy season, when mining operations and material transportation are often disrupted.

A steelmaker said, “We are securing additional iron ore volumes before the monsoon. Although steel demand remains weak, maintaining adequate raw material inventory is essential as supply risks typically increase during the rainy season.”

Despite the ongoing procurement activity, market sentiment remains cautious. Participants noted that the downstream steel market continues to face weak liquidity and subdued demand, limiting the scope for any significant increase in iron ore prices.

A buyer informed, “The finished steel market is not providing enough support for raw material prices. Demand remains moderate, and mills are carefully managing costs.”

Several miners concluded bulk transactions with regular customers ahead of the OMC auction, ensuring steady offtake. However, many producers have currently placed fresh offers on hold and are expected to revise their pricing strategies over the next few days based on auction outcomes and market response.

A miner mentioned, “We are evaluating market conditions and auction trends before releasing new offers. Price direction will become clearer once fresh bookings emerge in the coming week.”

While lump ore prices softened slightly this week, market sources believe miners are unlikely to implement aggressive price reductions for sized ore. The recent decline is being closely analyzed, with market participants suggesting that supply-side support and seasonal demand could prevent a deeper correction.

Factors affecting iron ore prices

Pellet prices mix w-o-w: Pellet (6-20 mm, Fe 62.5%) prices in Odisha’s Barbil fell by INR 100/t w-o-w to INR 8,000/t ($84/t) loaded to wagon on 19 June. Pellet (Fe 62.5%, 6-20 mm) prices in Durgapur increased by INR 150/t to INR 9,050/t ($95/t) exw.

Sponge iron showed stable w-o-w: According to BigMint’s assessment, sponge iron C-DRI (FeM 80%) prices in Rourkela fell by INR 100/t ($1/t) w-o-w to INR 25,2o0/t ($26/6t) on 20 June.

Billet prices stable w-o-w: Meanwhile, steel billet (100*100 mm) prices in Rourkela inched up by INR 100/t ($1/t) w-o-w to INR 38,500/t ($450/t) on 20 June.

Rebar prices decline m-o-m: Rebar (12-25mm, IF Route, Fe 500, IS 1786) prices fell by INR 200/t ($2/t) w-o-w to INR 41,800/t ($441/t) exw Rourkela on 20 June.

Outlook

As per BigMint’s analysis, greater clarity on Odisha’s iron ore market is expected next week as miners announce revised offers and additional trading activity takes place. Continued inventory building by steelmakers ahead of the monsoon will remain a key factor influencing market dynamics in the near term.

Leave a Reply