- Fe 55-60% deals remain limited with lack of offers

- DMG show-cause notice to 65 mines for dispatch

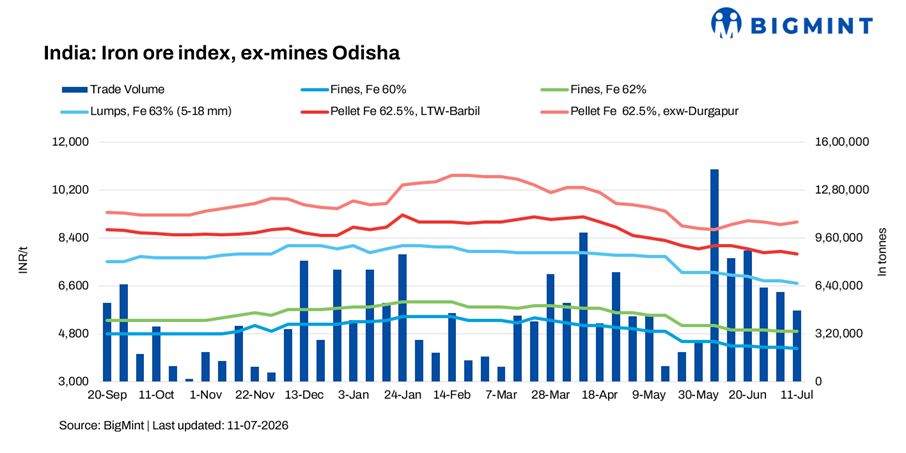

BigMint’s Odisha iron ore fines (Fe 62%) index remained stable w-o-w at INR 4,900/t ($51-52/t) ex-mines on 11 July 2026. Iron ore prices in Odisha continued to remain on the softer side this week as trading activity stayed largely concentrated in Fe 60% and above grade material, while deals involving Fe 55-60% ore remained limited due to the ongoing uncertainty surrounding material dispatch.

Auctions, deals

BigMint recorded deals for around 475,000 t of iron ore outside of auctions, concluded by steelmakers via traders and miners.

In SAIL auctions held this week, around 104,000 t of iron ore (Fe 58.71-62%) was booked at prices ranging between INR 3,625-5,750/t. The prices were on an ex-mines/FOR loaded into rake basis, inclusive of royalty, DMF, NMET, and additional premium charges.

Rationale

- T1- Two (4) deals for Fe 62% fines were recorded in the publishing window, and three were considered for price computation. This was given 50% weightage for index calculation.

- T2 – BigMint received eighteen (18) offers and indicative prices under the T2 category (offers, indicative, and bids) in this publishing window. Sixteen (16) were taken into consideration and given 50% weightage. To check BigMint’s iron ore assessment, pricing methodology, and specification document, click here.

Market highlights

According to market participants, miners largely maintained their offer prices for Fe 60+% iron ore, although a few suppliers extended discounts to regular customers for bulk purchases in an effort to sustain sales. Supplies of medium to high-grade iron ore were reported to be comfortable, allowing buyers to source cargo without significant difficulty.

A trader based in Odisha said, “Availability of higher-grade material has improved compared to the previous week. Most miners have resumed normal supplies, but demand is still limited because steelmakers are purchasing only what is immediately required.”

The supply situation for higher-grade iron ore has largely returned to normal, while lower-grade material continues to witness restricted availability from miners. As a result, trading activity remained heavily skewed towards Fe 60% and above material.

Another market participant commented, “The biggest concern at the moment is not availability but dispatch. Following the recent DMG circular issued to miners, many buyers are waiting for more clarity before committing to large-volume purchases.”

Meanwhile, the recent correction in semi-finished steel and downstream finished steel prices has continued to weigh on market liquidity. Weak margins in the steel sector have reduced buyers’ appetite for fresh raw material purchases.

In recent developments, Odisha Directorate of Mines & Geology (DoMG) has stepped up enforcement measures to curb annomaly in mineral dispatches, with a particular focus on grade manipulation. The move comes amid concerns that practices such as dilution, blending, misclassification and mis-declaration of iron ore grades have resulted in lower royalty collections and reduced auction premium realisation for the state.

An annexure to the notice lists more than 60 mining leases across major iron ore-producing regions, including Joda, Koira, Keonjhar, Jajpur Road and Baripada, where deviations between approved and dispatched grades were observed during Q1 FY’27.

Factors affecting iron ore prices

Pellet prices show mixed trends w-o-w: Pellet (6-20 mm, Fe 62.5%) prices in Odisha’s Barbil inched down by INR 100/t w-o-w to INR 7,800/t ($81/t) loaded to wagon on 3 July. Pellet (Fe 62.5%, 6-20 mm) prices in Durgapur increased by INR 100/t to INR 8,900/t ($93/t) exw.

Sponge iron falls w-o-w: According to BigMint’s assessment, sponge iron C-DRI (FeM 80%) prices in Rourkela fell by INR 400/t ($2/t) w-o-w to INR 24,300/t ($255t) on 11 July.

Rebar prices fall m-o-m: Rebar (12-25mm, IF Route, Fe 500, IS 1786) prices decreased by INR 1,000/t w-o-w to INR 40,500/t ($425/t) exw Rourkela on 11 July.

Outlook

As per BigMint’s analysis, the Odisha iron ore market is expected to remain cautious in the near term, with trading activity dependent on dispatch clarity, steel market sentiment, and the outcome of the upcoming OMC auctions.

Leave a Reply