- Festive holidays, dispatch challenges weigh on trading

- Sponge iron, semis prices decline by INR 500/t w-o-w

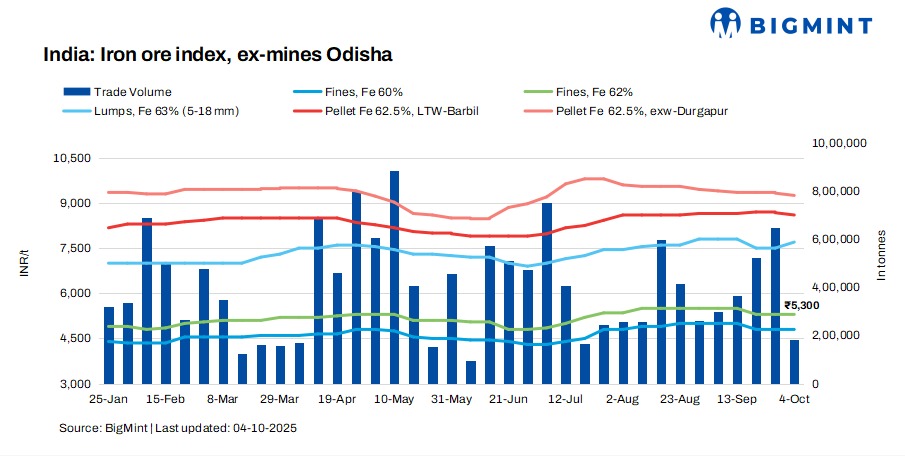

Odisha iron ore prices remained stable this week, as market activity was subdued due to ongoing festive holidays and limited production across major mining regions. Market participants highlighted that the availability of material in the spot market remained tight, while miners refrained from offering fresh quantities amid ongoing dispatch challenges.

Price update

BigMint’s Odisha iron ore fines (Fe 62%) index remained stable w-o-w at INR 5,300/tonne (t) ($60/t) ex-mines on 4 October 2025. Only a few sellers were offered higher-grade material in the market, further keeping trades limited.

BigMint recorded around 200,000 t of iron ore deals this week, concluded directly by the steelmakers. Meanwhile, lumps prices saw a slight uptick, with some material sold in the recent auctions.

At JSW’s iron ore auction on 29 September, 55,300-t CLO (Fe 61/63%) — 7,900 t (5-18 mm, Fe 61%) and 15,800 t (5-18 mm, Fe 63%) — were sold at base prices of INR 7,100/t and INR 7,700/t, respectively. Meanwhile, Vedanta’s 29 September auction witnessed 11,275-t (10-40 mm, Fe 56.5%) lumps unsold (base price INR 5,143/t).

Market highlights

According to sources, “There is hardly any fresh material entering the market. Most miners are busy clearing pending orders, and dispatches are getting delayed due to production gaps and logistics constraints.”

Market participants further highlighted that the lack of offers kept prices stable, despite weak sentiments in the downstream steel market. Sponge iron and billet prices remained under pressure, affecting steelmakers’ procurement confidence. A sponge producer added, “Steel prices are not showing any strong recovery, and mills are cautious in purchasing iron ore in bulk. Only need-based buying is happening at present.”

Buyers also mentioned that several smaller plants are struggling to secure a consistent material supply, with some waiting for earlier bookings to be dispatched. A buyer informed BigMint, “The scarcity of iron ore has made it difficult to plan production schedules. We are managing with whatever limited material is available.”

Meanwhile, sources informed that the central ministry’s 15-member committee is likely to meet next week to review the iron ore pricing mechanism and consider possible adjustments to export duties. The market is closely watching the outcome of this meeting for future price direction.

Factors affecting iron ore prices

Pellet prices edge down w-o-w: Pellet (6-20 mm, Fe 62.5%) prices in Odisha’s Barbil inched down by INR 50/t ($0.5/t) w-o-w to INR 8,600/t ($98/t) loaded to wagon. Pellet (Fe 62.5%, 6-20 mm) prices in Durgapur fell by INR 50/t ($0.5/t) w-o-w to INR 9,250/t ($104/t) exw on 3 October.

Sponge iron prices fall w-o-w: According to BigMint’s assessment, sponge iron C-DRI (FeM 80%) prices in Rourkela decreased by INR 500/t ($6/t) w-o-w to INR 25,500/t ($287/t) on 4 October.

Billet prices drop w-o-w: Meanwhile, steel billet (100*100 mm) prices in Rourkela dropped by INR 500/t ($6/t) w-o-w to INR 35,500/t ($400/t) today.

Rationale

- T1- Two (2) deals for Fe 62% fines were recorded in the publishing window, and were considered for price computation. These were given 50% weightage for index calculation.

- T2 – BigMint received eighteen (18) offers and indicative prices under the T2 category (offers, indicative, and bids) in this publishing window. Thirteen (13) were taken into consideration and given 50% weightage. To check BigMint’s iron ore assessment, pricing methodology, and specification document, click here.

Outlook

BigMint’s analysis indicates that iron ore prices in Odisha are expected to remain firm next week. Any further changes in prices will likely be determined by the outcomes of the upcoming ministry meeting.

Leave a Reply