- Fresh offers awaited in market, few bulk deals at revised prices

- Sharp hike in pellet and semi-finished prices supports some deals

Iron ore prices in the Odisha region remained largely under pressure in the week ended 3 April, with limited transactions reported by regular market participants. The market is currently in a transitional phase as the first week of the new fiscal year unfolds, and fresh offers from miners are still awaited. Most miners are closely evaluating prevailing market dynamics before announcing revised prices, which are expected to emerge in the coming days.

Price update

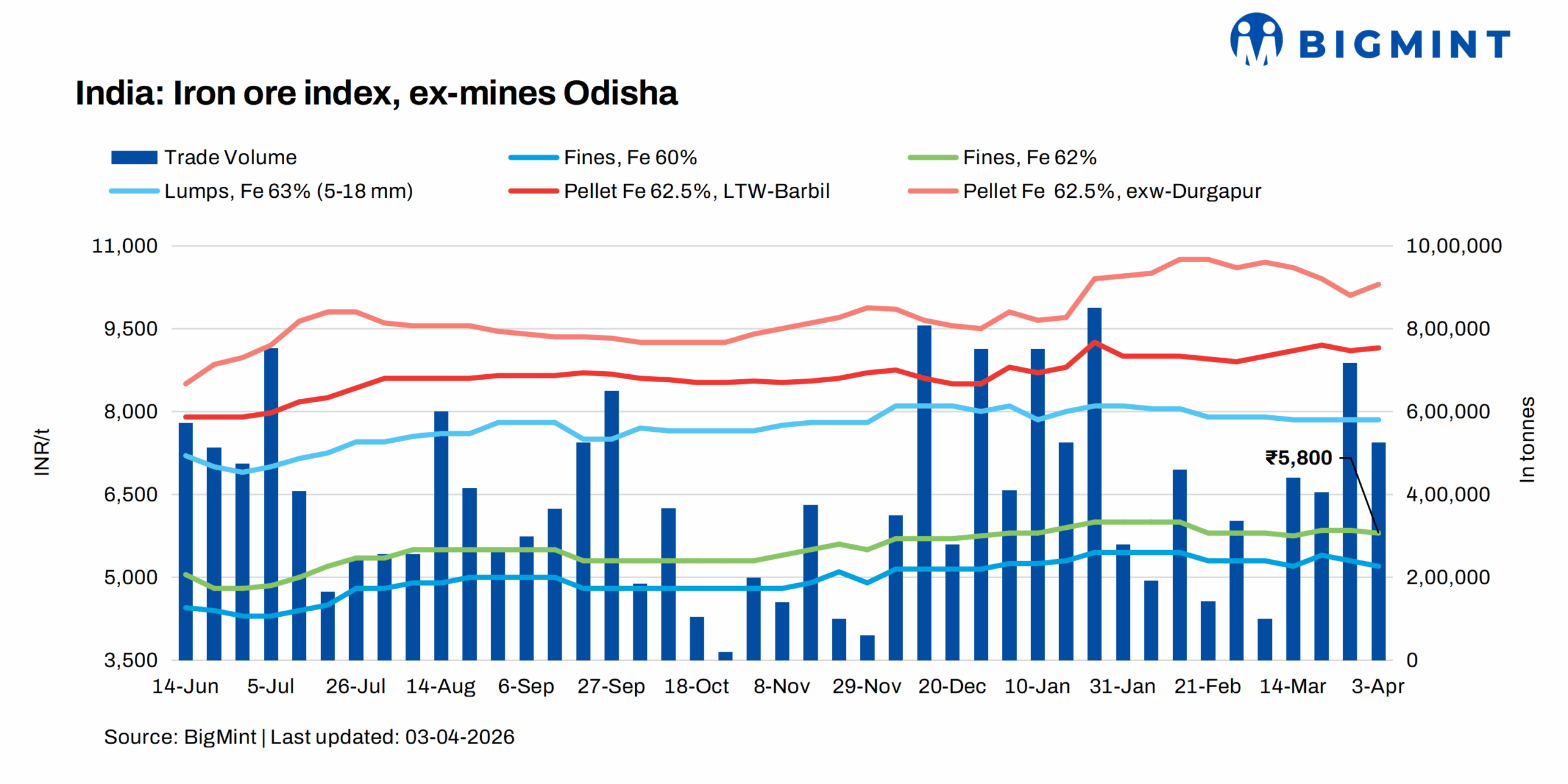

BigMint’s Odisha iron ore fines (Fe 62%) index decreased by INR 50/t w-o-w at INR 5,800/t ($63/t) ex-mines on Friday (3 April). It recorded deals for around 525,000 t this week, concluded directly by steelmakers with private miners and traders.

A few deals were concluded in the iron ore auction via SAIL, JSW, and AMNS this week. Around 150,000 t of iron ore was sold in auctions by these miners.

However, a few miners have already revised their offers and have begun accepting new orders at updated price levels. Despite this, buying activity has remained cautious. According to market participants, prices in the eastern region have softened slightly, primarily due to buyers’ reluctance to procure material at elevated rates.

Market highlights

A trader based in the region commented, “Buyers are hesitant right now as they expect more clarity on prices. Most of them are not willing to take positions at higher levels, especially when they anticipate some correction or stabilization in the near term.”

On the demand side, supportive sentiments from the sponge iron and downstream steel segments have helped keep the market somewhat active. A few bulk deals were reportedly concluded by miners, driven by improved realizations in semi-finished steel products.

A steelmaker noted, “Even though iron ore prices are not moving much, the strength in sponge iron and billet prices is encouraging some procurement. But overall, we are still cautious with fresh bookings.”

Buyers also highlighted that sufficient inventory levels are limiting immediate procurement interest. A buyer informed, “We already have enough stocks booked in previous months, so we can afford to wait for better price visibility.”

Additionally, while some miners are revising offers, actual material lifting is expected only after a couple of weeks. In the interim, traders have become more active, supplying material in the absence of fresh miner offers.

Market participants expect better clarity on pricing trends by next week or the following week, as more deals begin to surface.

Factors affecting iron ore prices

Pellet prices show mixed trend: Pellet (6-20 mm, Fe 62.5%) prices in Odisha’s Barbil increased by INR 150/t w-o-w to INR 9,150/t ($99/t) loaded to wagon on 3 April. Pellet (Fe 62.5%, 6-20 mm) prices in Durgapur rose by INR 200/t to INR 10,300/t ($111/t) exw.

Sponge iron prices surge w-o-w: According to BigMint’s assessment, sponge iron C-DRI (FeM 80%) prices in Rourkela sharply increased by INR 2,000/t ($22/t) w-o-w to INR 29,000/t ($313/t) on 3 April.

Billet prices up w-o-w: Meanwhile, steel billet (100*100 mm) prices in Rourkela also rose by INR 1,700/t ($18/t) w-o-w to INR 41,700/t ($450/t) on 3 April.

Rationale

- T1- Two (2) deals for Fe 62% fines were recorded in the publishing window, and one (1) was considered for price computation. These were given 50% weightage for index calculation.

- T2 – BigMint received eighteen (18) offers and indicative prices under the T2 category (offers, indicative, and bids) in this publishing window. Sixteen (16) were taken into consideration and given 50% weightage. To check BigMint’s iron ore assessment, pricing methodology, and specification document, click here.

Outlook

According to BigMint analysis, iron ore prices are likely to remain largely unchanged, although some aggressive trades may emerge once fresh offers are officially release.

Leave a Reply