- EBITDA increases by 7% y-o-y to record Q1 high of INR 572 crore

- Capacity expansions remain on track, supporting 35 mnt/year roadmap by FY’28

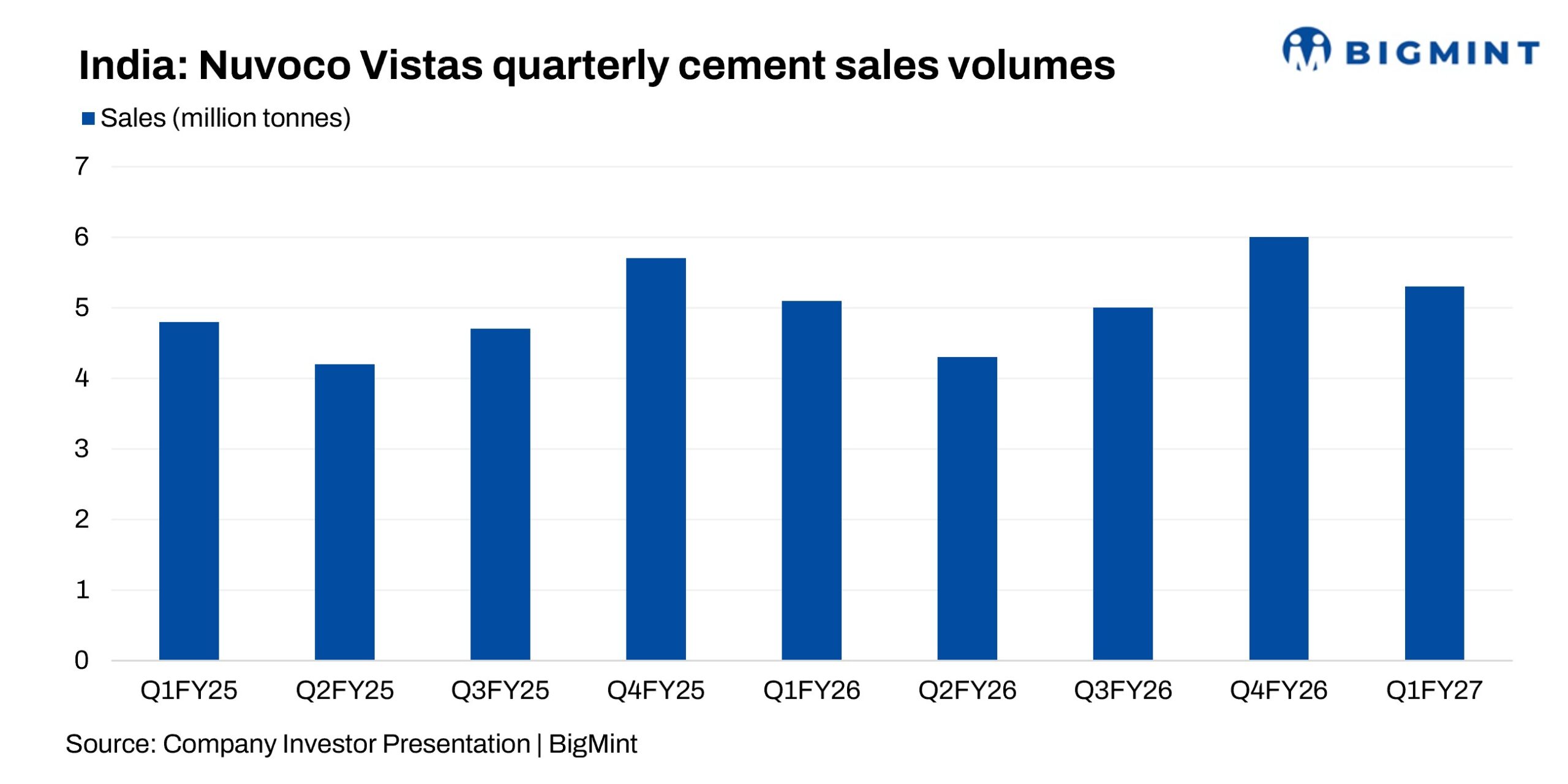

Nuvoco Vistas delivered a resilient operational performance in Q1FY’27, supported by higher cement volumes, improved price realisations, and disciplined cost management despite seasonal demand weakness, geopolitical uncertainties, and logistics disruptions. Cement sales volumes increased 5% y-o-y to 5.3 million tonnes (mnt), while EBITDA rose 7% y-o-y to INR 572 crore, marking the company’s highest-ever first-quarter EBITDA.

Stronger pricing, an improved geographical sales mix, and higher contribution from premium cement brands helped offset rising operating costs, according to the company’s investor call held on 14 July 2026.

Expansion projects remain on schedule

The company continues to advance its expansion roadmap during the quarter, reinforcing its target of achieving 35 mnt/year of cement capacity by FY’28.

- Limla grinding unit: The company commissioned its 2 mnt/year cement grinding unit at Surat, Gujarat, ahead of schedule in July 2026. The project strengthens its presence in western India while releasing capacity at its Rajasthan plants to better cater to northern markets.

- Kutch integrated plant: Construction of the 3.5 mnt/year clinker unit remains on track. Refurbishment of major equipment, including the Vertical Roller Mill (VRM) gearboxes, has been completed, with trial preparations planned during H1FY’27.

- Grinding unit, waste heat recovery (WHR): Civil works for the 2.5 mnt/year grinding unit and waste heat recovery (WHR) system are progressing steadily, with major reinforced cement concrete (RCC) works completed.

- Sachana bulk terminal: Construction of the bulk cement terminal and dedicated railway siding at Sachana, Ahmedabad, is progressing as planned and is expected to be commissioned in Q2FY’28, enhancing distribution efficiency across Gujarat.

Infrastructure spending expected to support cement demand

Nuvoco remains optimistic on India’s cement demand outlook and expects industry demand to grow by around 7-8% in FY’27, driven by government infrastructure spending, housing, commercial real estate, and industrial investments. While monsoon-related disruptions are likely to moderate demand during Q2FY’27, the company expects construction activity and cement dispatches to improve in the second half of the fiscal year.

Pricing gains offset rising input costs

Improved cement prices remained one of the key earnings drivers during the quarter. Average realisations increased by nearly INR 320/t q-o-q, supported by better market pricing, favourable geographical sales mix, and continued premiumisation.

Premium products continued to gain traction, with Concreto reaching annual sales of nearly 4 mnt, while Duraguard Microfiber and Uno each crossed 1 mnt annually. Together, premium products now contribute close to 5 mnt annually, supporting profitability and strengthening the company’s product portfolio.

Cost inflation remains a key challenge

Despite stronger pricing, operating costs remained elevated during the quarter. Power and fuel costs increased by around INR 40/t, raw material costs by INR 35-40/t, while packing bags and freight expenses each rose by nearly INR 50/t. Lower seasonal volumes also pushed fixed costs higher by INR 30-40/t, resulting in an overall cost increase of approximately INR 230/t compared with the previous quarter. Nevertheless, higher realisations helped the company protect margins.

Fuel optimisation continues despite changing energy mix

Fuel procurement remained focused on cost optimisation. The company maintained fuel costs at around INR 1.52 per million kcal, in line with internal guidance. During the quarter, coal’s share in the fuel mix increased to around 63% from 53% in the previous quarter, while the contribution of alternative fuels declined, reflecting procurement optimisation based on prevailing market conditions.

Logistics challenges impacted freight costs

Logistics remained a key operational challenge during Q1FY’27. Limited railway rake availability, priority movement for the power sector, and temporary shortages of trucks and diesel disrupted clinker and cement transportation. Consequently, a higher proportion of clinker was transported by road, leading to higher freight costs. Nuvoco expects logistics conditions to improve gradually as railway availability normalises.

Eastern India outlook remains positive

Management expects market conditions in eastern India to improve over the next 18-24 months, supported by slower clinker capacity additions and improving capacity utilisation. Higher utilisation is expected to strengthen pricing discipline and improve profitability across the region.

Capex programme remains on track

The company reaffirmed its expansion-led capital expenditure plan, with INR 900 crore earmarked for FY’27 and around INR 950 crore planned for FY’28. Investments will primarily support the Kutch integrated project, the Sachana bulk terminal, and other strategic initiatives aimed at strengthening manufacturing capacity and distribution efficiency.

Outlook

The company anticipates that ongoing capacity additions, improving product mix, and continued infrastructure-led demand are expected to support operational efficiency and strengthen its competitive position as it progresses towards its 35 mnt/year cement capacity target by FY’28.

Leave a Reply