- Expansion pipeline widens across BF, induction routes

- Flat steel growth broadens capacity expansion beyond construction demand

Data Deep Dive: India’s steel expansion cycle is broadening across both long and flat product segments, with regulatory approvals indicating that capacity additions are being driven simultaneously by secondary producers and large integrated mills.

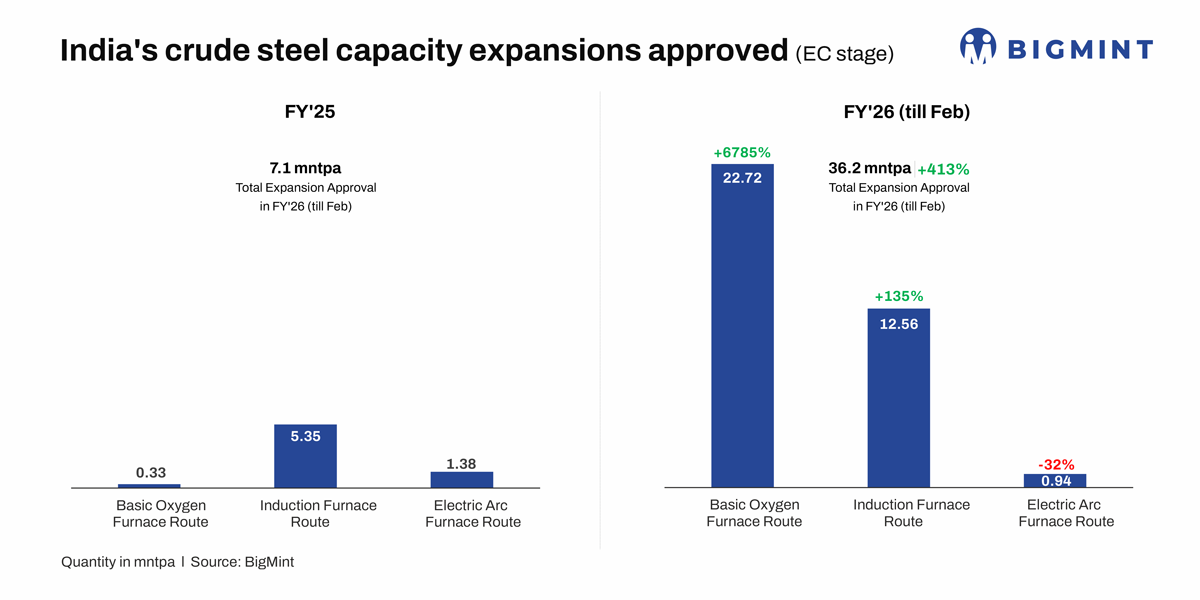

BigMint data tracking expansions approved under the environmental clearance and consent-to-establish pipeline shows that around 48.84 million tonnes (mnt) of crude steel capacity has been cleared for development in FY26 (till February).

The technology mix reflects a balanced expansion across routes, with 26.52 mnt of capacity approved via the blast furnace-basic oxygen furnace route and 22.3 mnt through electric routes, including induction furnace and electric arc furnace capacity. This indicates that the next phase of capacity growth will be driven by parallel expansion in both integrated and secondary steelmaking.

Environmental clearance remains a critical step in the project pipeline. Under India’s regulatory framework, projects must first receive Terms of Reference, followed by environmental clearance before applying for consent to establish and, eventually, consent to operate. The EC–CTE process serves as a leading indicator of future capacity creation, typically translating into operational capacity over a multi-year horizon.

Flat steel expansion gathers pace

The product mix shows that flat steel capacity expansion has accelerated alongside long products. Approvals indicate around 16.21 mnt of flat steel capacity, including hot-rolled coil and plate, compared with 22.41 mnt of rolling long capacity.

While long products continue to lead, flat steel is now a significant component of the pipeline. Within this, hot-rolled coil accounts for the bulk of additions, pointing to a clear build-out of upstream flat steel capacity.

The data indicates that the expansion cycle is no longer confined to construction-linked steel. Rising flat steel capacity reflects growing alignment with manufacturing, automotive and downstream processing demand, and is expected to support both domestic consumption and export positioning.

Long products remain central to volume growth

Long products continue to anchor incremental capacity additions. With 22.41 mt of rolling long capacity approved, expansion remains closely tied to infrastructure demand across roads, railways, housing and energy.

We expect infrastructure spending to remain the primary driver of steel consumption growth in the medium term, even as flat steel gains share in the expansion pipeline.

Dual industry structure becomes more pronounced

The expansion pattern highlights a clear dual structure within the industry. Integrated producers are driving much of the blast furnace-based capacity and flat steel expansion, while secondary mills continue to dominate additions through electric routes and long products.

Approvals reflect this divergence. Large integrated players such as ArcelorMittal Nippon Steel India, Neelachal Ispat Nigam, and JSW Steel have received clearances for substantial BOF-based capacity additions, while secondary producers including Action Ispat & Power, Riron Power, and Godawari Power & Ispat are expanding through electric routes.

We expect this dual structure to persist, with integrated mills focusing on scale and flat steel, while secondary producers continue to drive dispersed capacity growth in construction steel.

Despite rising flat steel capacity, the expansion remains structurally linked to the direct reduced iron route. A significant portion of electric route capacity additions continues to rely on sponge iron as feedstock, implying sustained demand for DRI, pellet feed and beneficiated iron ore.

India already produces more sponge iron than any other country, and the expansion of induction furnace capacity suggests that the DRI-based ecosystem will remain central to the secondary steel sector.

Implications for the iron ore market

The expansion pipeline carries important implications for the iron ore market. The combined growth of DRI-based and integrated steelmaking capacity will increase demand for high-grade iron ore and processed feedstock.

The pipeline already includes substantial investments in beneficiation and pelletisation, indicating deeper backward integration across the value chain. As new capacity comes online, domestic iron ore consumption is expected to rise steadily, tightening export availability while strengthening India’s integrated iron ore-to-steel supply chain.

Approvals remain concentrated in eastern and central India, particularly in Chhattisgarh, Odisha and Andhra Pradesh, which together account for the bulk of capacity additions. These regions benefit from proximity to iron ore reserves, established industrial ecosystems and improving logistics infrastructure, reinforcing their position as the core of India’s steel expansion.

Outlook

India’s steel sector is entering a broad-based expansion phase, with capacity additions spanning both long and flat product segments. We expect demand from infrastructure and construction sectors to continue driving incremental volumes, while rising flat steel capacity supports manufacturing and export growth.

If current approvals translate into commissioning over the next few years, the pace of capacity addition could begin to outstrip demand growth in certain segments, particularly in long products where expansion remains concentrated among secondary mills.

This could lead to periodic pressure on capacity utilisation and margins, especially during phases of weaker infrastructure spending, even as integrated producers remain better positioned to leverage flat steel demand and export markets.

The industry is evolving into a dual growth model, combining integrated flat steel expansion with fragmented secondary capacity in long products, as India moves toward its long-term target of 300 mnt crude steel capacity by 2030-31.

Leave a Reply