- ADC12 alloy imports plunge over 50% y-o-y

- Passenger vehicle sales surge to record highs in Oct

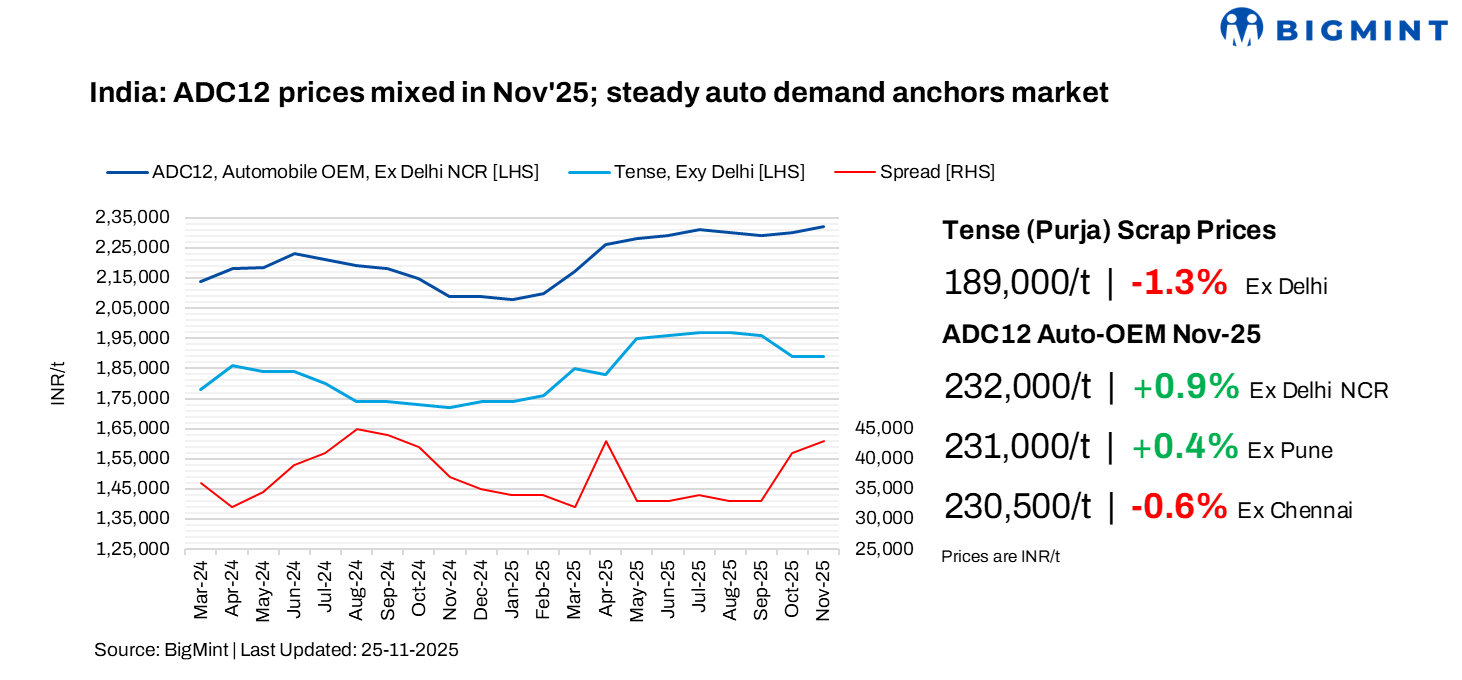

India’s aluminium ADC12 market showed mixed movement in November 2025 after rising in October. Even with regional variations, demand from the auto sector remained strong, helping keep prices steady and preventing any major decline.

International scrap prices increased due to higher LME levels, but domestic scrap prices fell as availability improved creating a wider gap between scrap and semi-finished products. Import conditions also became more favourable as restrictions on ADC12 were relaxed, and stable automotive demand continued to support consumption and pricing across the north, west, and south.

BigMint data shows that average OEM ADC12 prices for November increased month on month in Delhi and Pune, reaching INR 232,000/t and INR 231,000/t, which is an increase of INR 2,000/t and INR 1,000/t respectively. Chennai recorded an average price of INR 230,500/t, which is a decrease of INR 1,500/t. The gap between scrap and semi-finished products widened to INR 43,000-45,000/t, indicating that ADC12 prices stayed firm while domestic scrap prices continued to fall.

Additionally, a leading Indian automaker has increased its ADC12 settlement price by INR 800/t m-o-m to INR 232,600/t for December 2025. The price hike was primarily driven by firm demand in the automobile segment following the recent GST reduction. Meanwhile, the scrap-to-ADC12 spread widened to INR 43,000-44,000/t as of November 2025 average.

Market dynamics in early Dec’25

Market feedback from the northern and western regions shows that supplier offers for ADC12 in late November and early December were generally between INR 233,000-234,000/t. However, OEMs were negotiating slightly lower settlement levels for November, in the range of INR 230,000-232,000/t on the usual 30-day payment terms.

In the southern region, suppliers were reportedly offering ADC12 at INR 230,000-231,000/t, while buyers were bidding slightly lower at around INR 228,000-229,000/t. BigMint’s bi-monthly ADC12 assessments indicate that prices in Chennai were higher during the first week of November but started to decline as domestic scrap availability improved and scrap prices fell. In contrast, prices in the North and West remained steady, largely tracking the settlement levels of major automaker.

Raw material trends

In October, imported aluminium scrap prices rose, driven by rise in average LME aluminium prices to $2,845/t in November due to supply concerns and optimism over the December US Fed rate cuts, marking a 2.2% m-o-m gain. In contrast, domestic aluminium scrap prices, particularly casting-grade scrap used for ADC12 production, declined as availability improved with higher import levels. Notably, tense scrap prices in Chennai fell below Delhi levels in mid-October, reflecting better domestic supply in the south and strict GST compliance.

Market participants in Chennai noted that securing casting scrap on a daily basis has become much easier than before when availability was a major challenge. They also reported that higher scrap imports have improved material supply in domestic markets across both the northern and southern regions of India.

Among key imported grades, US-origin Tense rose by $5/t m-o-m to $2,005/t, while UK-origin Wheels increased by $35/t to $2,645/t. On the domestic front, Tense scrap prices fell by INR 2,500/t in Delhi and INR 6,500/t in Chennai, with BigMint’s November averages at INR 189,000/t in Delhi and INR 185,000/t in Chennai.

Meanwhile, Chinese silicon 553 prices remained stable at $1,360/t CFR Mundra amid steady demand.

India’s scrap, ingot imports in 10MCY’25

India’s aluminium scrap imports rose year on year during January-October 2025, reaching 1.65 mnt, an increase of 14% compared with 1.4 mnt in the same period last year.

The United States remained the largest supplier, shipping 0.34 mnt to India, although this was 2% lower than 10MCY’24 due to strong domestic scrap demand in the US and uncertainty around tariffs.

ADC12 imports

In contrast, India’s ADC12 alloy imports saw a steep decline. During the first ten months of 2025, inbound ADC12 volumes fell by 51% y-o-y, totalling only 10,250 t compared with 20,996 t in the same period of 2024.

Auto sector performance

Passenger vehicle retail sales in October hit an all-time high, growing 86% m-o-m to 0.56 million units. This surge was driven by the rollout of GST 2.0, strong festive sentiment during Dussehra and Diwali, and robust rural demand. Dealers also reported improved conversions and healthier inventory levels, which eased by 5 to 7 days, reflecting better supply alignment.

On the other hand, the overall automobile retail sales stood at 22.6 million units in 10MCY’25, reflecting an 8% increase y-o-y from 20.9 million units in the previous year.

Outlook

ADC12 prices in December are expected to stay stable to slightly firm across regions. Strong automotive demand, supported by GST 2.0 benefits and steady PV production, will continue to provide a price floor. Improved domestic scrap availability may limit sharp increases but earlier OEM price hikes and healthy year-end retail momentum should prevent any decline. Overall, a steady market with a mild upward bias is anticipated, with no major correction likely.

Leave a Reply