- Australian PHCC, Chinese iron ore tags rise in early-Nov

- Manufacturing PMI climbs in Oct’25 on robust auto sector

Leading Indian steelmakers have increased hot-rolled coil (HRC) and cold-rolled coil (CRC) prices by INR 1,250/tonne (t) for November 2025 sales compared with late-October list levels. However, one major producer has opted to keep prices unchanged for the same period.

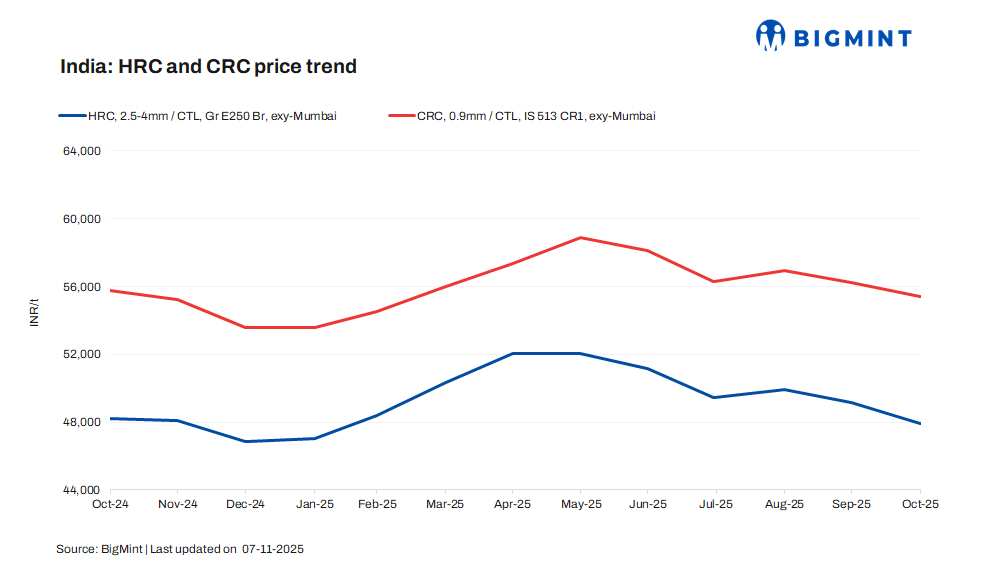

List prices of HRCs (2.5-8 mm, IS2062, Gr E250 Br) ranged within INR 47,700-50,500/t ($538-570/t) ex-Mumbai. CRCs (0.9 mm, IS513 CR1) were listed at INR 53,200-57,250/t ($600-646/t).

BigMint’s benchmark assessment (bi-weekly) for HRCs (IS2062, Gr E250, 2.5-8 mm/CTL) inched up by INR 200/t ($2/t) w-o-w to INR 47,600/t ($544/t) on 4 November 2025 against INR 47,400 ($546/t) on 28 October 2025. Moreover, CRC (IS513, Gr O, 0.9 mm/CTL) prices rose by INR 500/t ($5/t) w-o-w to INR 55,500/t ($628/t) on Tuesday against INR 55,000/t ($630/t) a week ago. These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

On an m-o-m basis, trade-level prices of HRCs fell by INR 1,200/t ($9/t) to INR 47,900/t ($553/t) in October 2025 against INR 49,100/t ($562/t) a month ago. Similarly, CRC prices fell by INR 850/t ($6/t) to INR 55,400/t ($635/t) in October 2025 against INR 56,250/t ($641/t) in September 2025.

What propelled mills to raise list prices for Nov’25?

1. Raw material prices rise: Prices of steel-making raw materials such as iron ore and coking coal have risen lately. The benchmark iron ore fines spot prices showed a slight rise of around $1/t, averaging $107/dmt CFR China in early November 2025 against a monthly average of $105/dmt in October 2025.

Similarly, Australian imported premium hard coking coal (HCC) prices increased during this period. The average price of Australian-origin premium HCC stood at around $197/t in early November 2025 against a monthly average of $191/t in October 2025, as per BigMint records. This marks an increase of $6/t m-o-m.

2. Manufacturing PMI increases: India’s Manufacturing PMI climbed up to 59.2 points in October 2025, reflecting strong factory activity. Moreover, robust new orders, especially from the automobile sector, boosted output and purchasing, as demand strengthened, driven by GST reforms, aiding price hike momentum.

Outlook

The Indian HRC market is expected to stay in wait-and-watch mode as participants assess mills’ revised pricing. Additionally, the announcement of safeguard duties is likely to further curb imports, influencing the domestic landscape, while ongoing BF/HSM maintenance will keep supply tight.

Leave a Reply