- Demand from steelmakers, foundries remains steady

- Pig iron prices dip but met coke prices not impacted

Indian blast furnace (BF)-grade metallurgical coke prices remained stable w-o-w on 18 February 2026, supported by balanced domestic fundamentals and firm import parity despite softer raw material costs.

Domestic price trend

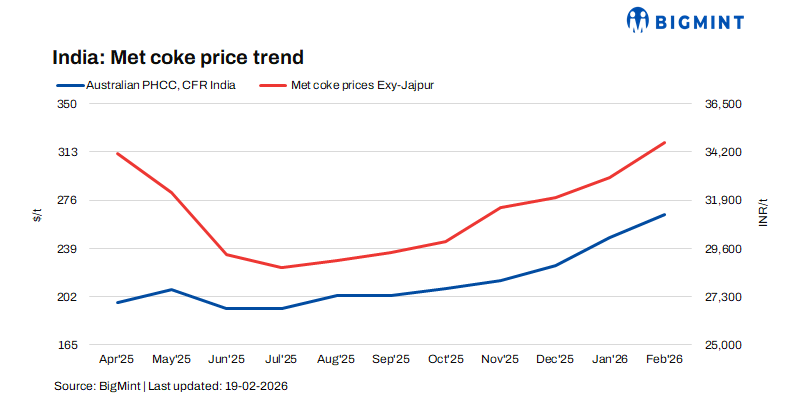

In eastern India, BF-grade coke (25-90 mm) prices were steady at INR 34,800/tonne (t) ex-Jajpur, while in western India, prices held at INR 30,400/t ex-Gandhidham. The stability reflects measured procurement by steelmakers and disciplined supply from domestic coke producers.

Similarly, foundry-grade metallurgical coke (+90 mm) prices remained unchanged at INR 36,100/t ex-Rajkot, indicating steady demand conditions in the casting and foundry segment, with no significant pressure from either supply or consumption.

Import parity and external influences

Firm import price indications also contributed to the market stability. Indonesian-origin BF coke (65/63) offers were heard at $270-275/t CFR India, with landed costs equivalent to around INR 34,000-34,500/t. The stronger import indications enabled domestic suppliers to maintain elevated offer levels despite marginal softening in coking coal costs.

On the raw material front, Australian premium hard coking coal prices declined by $6/t w-o-w to $ 243/t FOB amid subdued buying interest and cautious procurement by major importing markets. However, the decline was not steep enough to significantly alter domestic coke pricing structures.

In China, the domestic coking coal market remained stable, with prices unchanged across key production hubs such as Tangshan, Changzhi, and Lüliang. While holiday-related mine closures temporarily tightened supply, weak trading activity and the completion of winter restocking by steel mills limited demand. Reduced procurement by mills and traders, along with easing raw coal prices, is expected to keep the Chinese market stable to slightly weak in the near term.

Downstream market indicators

BigMint assessed steel-grade pig iron in Durgapur at INR 38,300/t ex-works, declining by INR 400/t w-o-w. Prices were marginally lower, reflecting cautious buying sentiment in the steel value chain. However, these did not trigger immediate pressure on met coke demand.

Outlook

Indian BF-grade metallurgical coke prices will stay at around current levels next week, with a slight drop possible due to softer coking coal costs. However, firm Indonesian import offers and steady domestic steel output should limit sharp corrections. Some market participants highlighted that Indonesian met coke offers are likely to increase in the near term, given that active bookings were done in the past month and coke supply may decrease before the April-May laycans.

Leave a Reply