- Western prices gain while east remains stable

- Higher feedstock costs add upward pressure

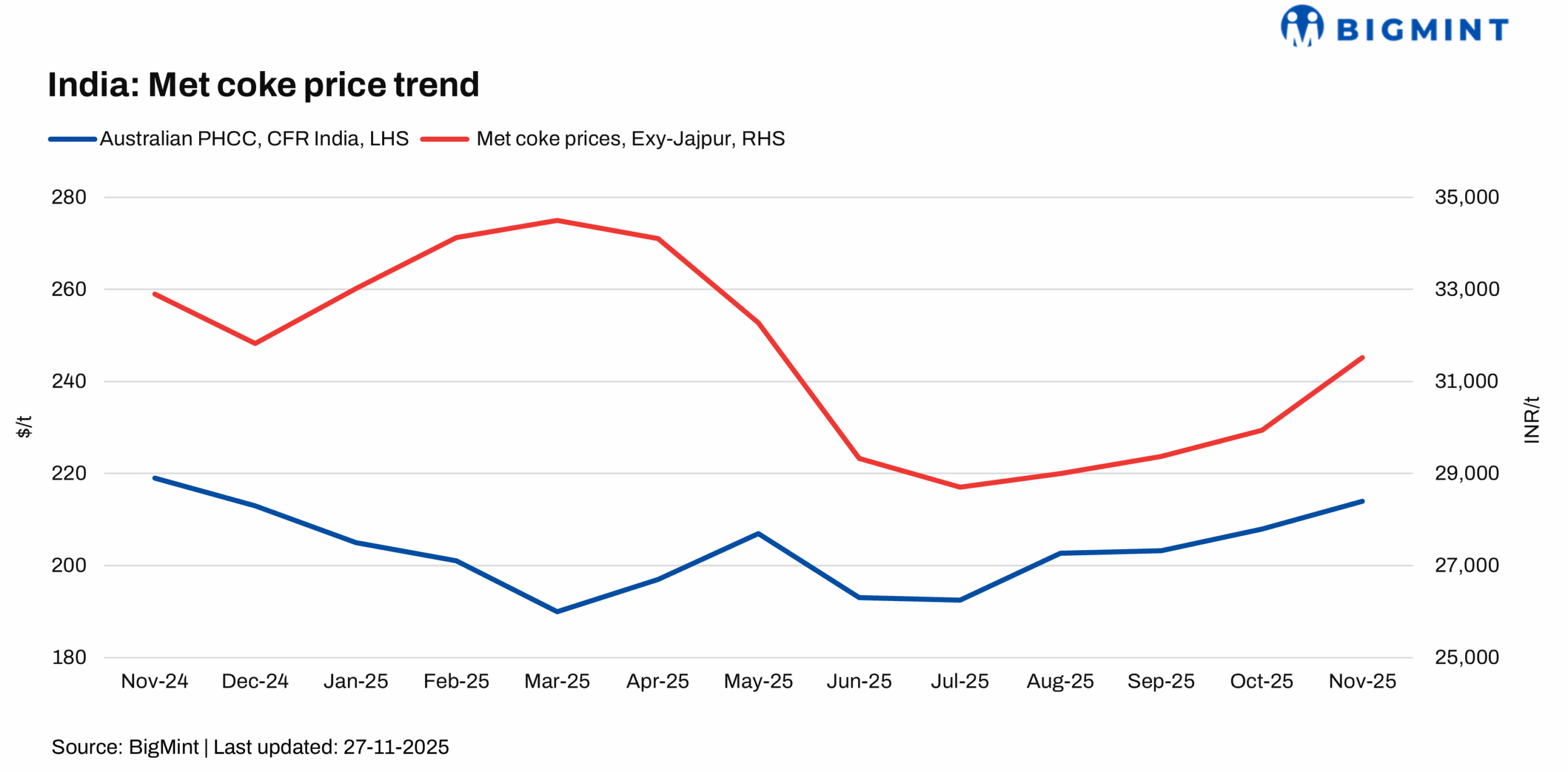

India’s metallurgical coke (met coke) market witnessed stable fundamentals with mild positive sentiment during the week ending 27 November 2025.

BF-grade (25-90 mm) met coke prices in eastern India were unchanged w-o-w at INR 31,800/t ex-Jajpur. In contrast, western India saw a slight lift, with the BF grade, ex-Gandhidham, assessed at INR 30,200/t, an INR 200/t rise w-o-w. Foundry-grade (+90 mm) met coke prices in Rajkot remained firm at INR 36,000/t, indicating stable domestic demand.

Market highlights

The market was broadly steady across regions. Eastern BF-grade prices remained stable after several weeks of continuous increases, while Western prices firmed up following a prolonged flat pattern.

Market participants largely adopted a wait-and-watch approach after the release of preliminary anti-dumping findings, with clarity on final duties still pending.

Higher feedstock costs added upward pressure: Australian premium HCC rose by $4/t w-o-w to $199/t FOB, reinforcing supply-led firmness.

China: Fragile stability amid soft sentiment

China’s met coke spot market remained stable but was clouded by weakening sentiment. Steady feedstock costs, firm on-site procurement, and calibrated production cuts helped maintain equilibrium. However, soft steel margins and uneven coke quality capped aggressive buying.

Inventories inched up even as producers continued to control output, as several steel mills reduced procurement ahead of winter demand transitions. Futures markets extended their decline amid subdued speculative participation, reflecting broader caution and reinforcing limited near-term momentum.

Pig iron prices register mild correction

The domestic pig iron market showed slight weakness. Steel-grade pig iron ex-Durgapur fell by around INR 150/t w-o-w to INR 32,400/t, driven by tepid trade activity.

Outlook

Domestic met coke prices are expected to stay range-bound in the near term. Western markets may retain a mild upward bias, while eastern prices could remain stable. Any confirmation of anti-dumping duties and volatility in seaborne coking coal will be pivotal in shaping upcoming market direction.

Leave a Reply