- Steel sector demand sees no improvement

- Chinese market stabilises after 4th price cut

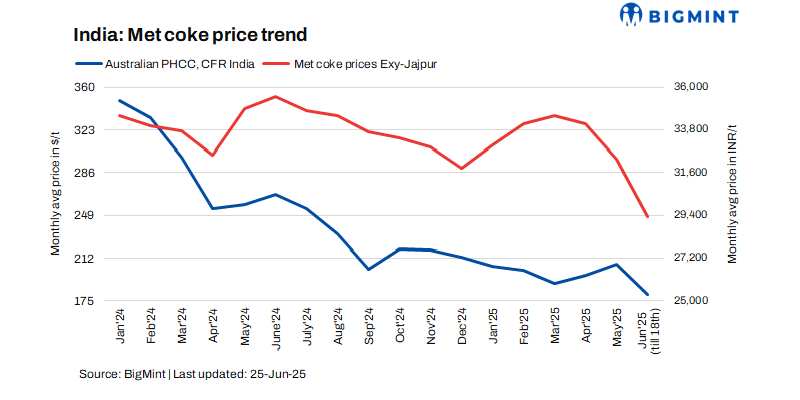

Indian metallurgical coke price tags continued to decline this week, remaining at over five-year lows, amid tepid steel sector demand and policy-related uncertainties. According to BigMint’s assessment on 25 June, the 25-90 mm blast furnace (BF) grade coke price dropped by INR 1,000/tonne (t) w-o-w to INR 28,000/t ex-Jajpur. In western India’s Gandhidham market, prices also slipped by INR 150/t w-o-w to INR 29,000/t ex-works.

Steel sector struggles weigh on demand

The price drop is largely attributed to sluggish demand from steelmakers. Uncertainty over the potential continuation of quantitative restrictions (QRs) on coke imports has also made buyers cautious, limiting procurement activity further.

Global market shows stabilisation but limited impact on India

While India struggles with oversupply, China’s coke market is showing early signs of stabilisation after four rounds of price cuts totalling RMB 220-240/t ($31-33/t) since mid-May. Steel mills in China resumed cautious restocking amid tight supply and rising coking coal costs. However, these developments have had minimal impact on Indian prices so far due to weak local fundamentals.

Coking coal prices ease slightly

Australian premium hard coking coal (PHCC) tags declined marginally by $1/t w-o-w to $174/t FOB last week, amid mixed market sentiment, though there are expectations of price improvements for premium low and mid vol. Although global coking coal prices recently stabilised, they have yet to offer meaningful support to Indian met coke prices.

Outlook: Further pressure likely

With demand still subdued and oversupply persisting, Indian met coke prices may face further downward pressure in the short term. Any stabilisation will likely depend on a recovery in steel demand or clearer policy direction regarding import controls.

Leave a Reply