- ERW pipe list prices drop by INR 1000/t for mid-Mar’26 sales

- HRC prices rise due to higher raw materials costs

A leading Indian ERW pipe producer, specialising in hot-rolled coil (HRC)-based products, has reduced list prices of its base-grade pipes (25-125 NB, 2.2-6 mm) by INR 1,000/t across various locations for mid-March 2026 sales compared with early-March 2026, market participants told BigMint.

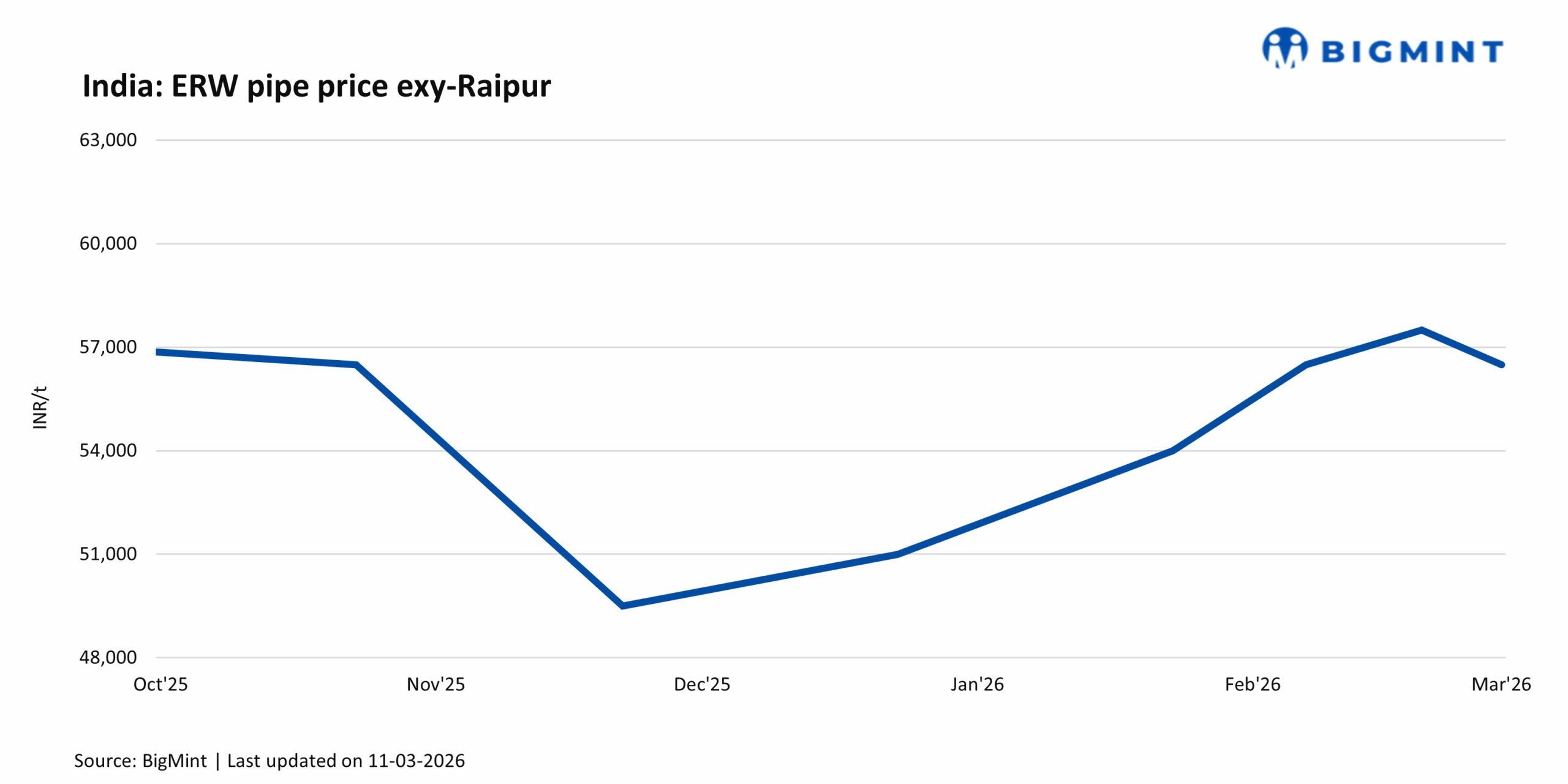

Post revision, list prices reached INR 56,500/t ($615/t) exy-Raipur, INR 58,500/t ($637/t) exy-Pune and INR 58,500/t ($637/t) exy-Delhi, excluding 18% GST. The revised prices are effective from 10 March 2026.

Market update

Distributor-level monthly average prices of ERW pipes in Raipur declined by INR 850/t ($9/t) m-o-m to INR 57,300/t ($624/t) in March compared with INR 58,150/t ($633/t) in February 2026.

During the first week of the month, market activity remained weak due to the Holi festival slowdown, leading to cautious buying behaviour and limited transactions among participants.

Furthermore, a market participant informed BigMint that, “Prices had remained relatively high over the past few months, resulting in inventory build-up across the market. In order to clear these inventories, prices are now being adjusted downward.”

Market participants also reported weak demand and slow sales, resulting in procurement activity largely remaining limited to immediate requirements, as traders refrained from building inventories amid subdued market conditions.

Trade-level HRC prices rise m-o-m

However, on a m-o-m basis, trade-level HRC prices for (IS2062, Gr E250, 2.5-8 mm/CTL) exy-Mumbai, increased by INR 1,250/t ($13/t) to INR 55,000/t ($598/t) in March 2026 compared with INR 53,750/t ($585/t) in February 2026, with demand remaining steady m-o-m.

The rise in trade-level HRC prices has largely been driven by higher raw material costs and a reduction in imports. Input costs have increased, with coking coal prices rising by around $10/t m-o-m to approximately $260/t in February 2026. At the same time, the 12% safeguard duty on steel imports has pushed up the landed cost of overseas material, resulting in lower import volumes. With fewer imports entering the market, domestic producers are finding greater room to raise prices.

However, the recent increase in HRC prices has not yet translated into higher ERW pipe prices as of 11 March 2026, as downstream trading activity remains subdued. Weak demand has restricted procurement activity largely to need-based purchases, keeping overall buying interest limited and preventing any meaningful upward movement in pipe prices.

Outlook

ERW pipe prices are likely to remain under mild pressure in the near term amid weak demand and elevated inventory levels. However, lower imports and higher HRC costs could gradually lend support to domestic ERW pipe prices in the near term if demand improves. Meanwhile, ongoing geopolitical tensions may continue to keep the market volatile.

Leave a Reply