- Australian miner widens discount for May delivery

- Limited availability of Indian Fe57% cargo in market

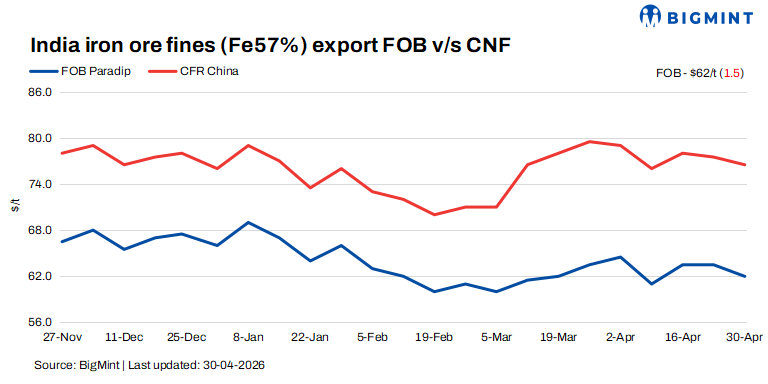

BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index inched down by $1.5/t w-o-w to $62/t FOB east coast on Thursday, 30 April 2026. Meanwhile, CFR China prices for Indian-origin iron ore softened w-o-w to $76.5/t, with vessel freight rates remaining largely stable.

Iron ore export prices declined this week in the seaborne market, primarily due to higher discount rates on lower-grade materials and subdued demand ahead of the upcoming Labour Day holidays in China.

Prices, deals

Deal activity remained healthy, with transactions for around 400,000 tonnes (t) recorded from east coast-based and west coast based exporters during the assessment window. Most deals were concluded for Fe 55-57% fines, while demand for lower-grade Fe 54-55% cargoes remained weak, with offers receiving limited acceptance.

Australian miners increased discounts on their special lower-grade fines, with May delivery cargoes offered at around 13%, compared to 10.75% for April shipments. This widening discount reflects a weaker appetite for lower-grade materials amid soft downstream steel demand.

Meanwhile, discounts for Indian lower-grade fines remained uncertain due to a lack of concluded trades. However, market participants indicated that discounts could hover around 22-23% for Fe 57% cargoes and approximately 26% for Fe 55% fines.

Market scenario

Market sentiment remained cautious as most steel mills had already completed their restocking activities, limiting fresh buying interest during the week.

An international trader noted that the market was largely cautious this week, as mills had already secured sufficient inventories and were preparing for the Labor holidays. He added. “There is limited spot buying interest at the moment, and most mills are staying on the sidelines.”

Another trader added that demand was not particularly strong, while the supply of Fe 57% cargoes remained tight, with only a few miners offering such material in the market.

On the other hand, traders reported that most of the available cargoes in the spot market were in the Fe 54-55% range, which attracted limited interest from buyers due to concerns about quality. An exporter noted, “Lower-grade cargoes are facing significant resistance, and buyers are not willing to take positions at current discount levels.”

Chinese mills have largely refrained from purchasing spot cargoes in recent days, further dampening market activity. Additionally, sources indicated that the removal of restrictions on Australian cargoes at Chinese ports by CMRG has improved the availability of seaborne supply. This development has exerted further pressure on Indian fines, making it challenging for exporters to secure deals.

Market participants expect limited activity in the coming days, with the market likely to remain closed until 5 May due to holidays.

Domestic prices exceeded export realizations by around INR 300/t ($3/t), with the gap widening by INR 50/t ($0.5/t) w-o-w. Iron ore fines (Fe 57%) prices in Odisha were recorded at INR 3,750/t ($40/t) ex-mines, and remained stable w-o-w on 23 April. Meanwhile, the ex-mines realization in exports from the Barbil region was recorded at INR 3,450/t ($36/t).

Chinese iron ore fines prices stable w-o-w: The benchmark iron ore fines Fe 61% index remained stable w-o-w at $108/dmt CFR China on 29 April. Prices were supported by limited trading, mainly in the medium-grade segment. Improved sentiment in steel exports is likely to support pig iron output and iron ore demand. However, the current shift toward fines demand may be temporary, with lump demand and prices expected to recover soon.

DCE iron ore futures rise: Iron ore futures on the Dalian Commodity Exchange (DCE) for the September 2026 contract closed higher at RMB 793.5/t ($115/t) against RMB 775.5/t ($113/t) on 30 April, increasing by RMB 18.5/t ($2/t) w-o-w.

Rationale

- One deal for Fe 57% were recorded, which was not taken during this publishing window. Therefore, T1 trade was given 0% weightage in the index calculation. For the detailed methodology, click here.

- BigMint received nineteen (19) indicative prices in the current publishing window, and sixteen (16) were considered for price calculation as T2 inputs and given the rest 50% weightage.

Outlook

Price direction is expected to become clearer once trading resumes next week, depending on post-holiday demand recovery and inventory positions at Chinese mills.

Leave a Reply