- Price rally encourages importers to restock material before further upside

- Rise in Berry Scrap imports suggests primary rod mills lifting scrap usage

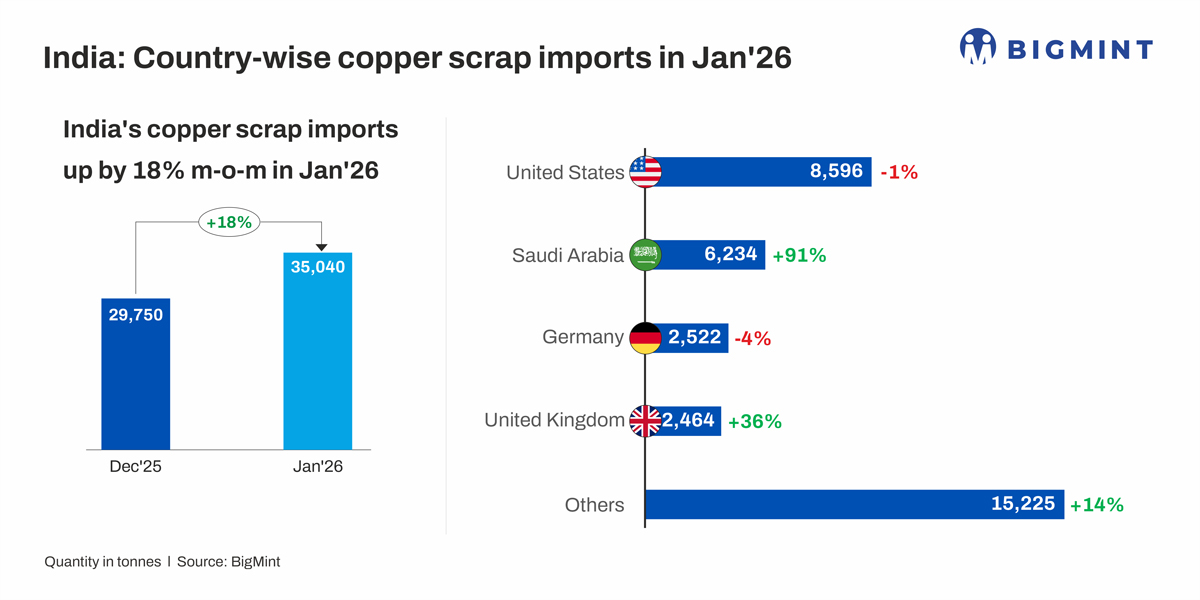

India’s copper scrap imports surged 15% m-o-m in January 2026 to 35,042 tonnes (t) from 29,750 t in December 2025, as per BigMint data. This was despite a sharp 11% m-o-m uptick in copper prices, from $11,800/t in December 2025 to $13,070/t in January 2026, driven by improved global demand after the year-end slowdown.

The fact that scrap imports rose even when LME prices crossed $13,000/t suggests buyers actively secured material due to feedstock necessity. The drop in cathode imports from 12,150 t to 8,550 t confirms that scrap was being used as a direct substitute in the melt mix, especially by rod makers and secondary refiners.

The price rally likely encouraged stock replenishment before further upside, particularly as market participants anticipated tighter non-US availability due to US-bound cargo diversion.

Country-wise imports

Middle East-origin material (primarily Saudi Arabian) contributed the most to the monthly expansion. Middle East-origin scrap typically carries competitive pricing and shorter transit times compared to Europe, making it attractive when Indian buyers are restocking aggressively.

US led scrap inflows but sourcing diversified. Volumes from the United States declined marginally by 1% to 8,596 t, indicating stable trade flow, while Germany fell 4% to 2,522 t, likely due to limited spot availability or shipment rescheduling. Imports from Saudi Arabia surged 91% m-o-m to 6,234 t from 3,270 t, likely due to large cargo arrivals and improved shipment scheduling from Middle East suppliers after year-end slowdowns. The United Kingdom also recorded a strong 36% rise to 2,464 t, possibly reflecting deferred December shipments clearing in January.

Grade-wise scenario

Berry scrap recorded the sharpest increase, surging 137% m-o-m to 7,314 t. This is particularly significant because Berry offers higher metallic recovery and is suitable for continuous casting rod units. The jump suggests that primary rod mills — not just secondary smelters — are actively absorbing scrap. This aligns with feedback that 5-6 new recycling-linked units in North India and 1-2 in South India are increasing melt capacity.

Birch imports rose 18%, supported by steady demand from secondary smelters due to its relatively high copper content and stable recovery rates.

Brass Honey increased 6%, reflecting consistent demand from India’s brass ingot manufacturers, particularly as India exports brass products to China and other Asian markets while importing brass scrap as raw material.

The steady rise in brass scrap imports also indicates that India’s brass export cycle remains intact despite higher LME prices, meaning downstream order books are firm enough to pass on higher input costs.

Other updates: Gravita enters copper recycling segment

Meanwhile, Gravita India — with its core business spanning lead battery recycling, aluminium alloy manufacturing, plastic recycling, and waste tyre recycling — has signed a binding agreement for the proposed acquisition of Rashtriya Metal Industries Ltd (RMIL), marking its formal entry into the copper segment. The acquisition provides access to a state-of-the-art facility in Gujarat with a production capacity of 31,200 t/year. The move aligns with Gravitas strategy to diversify beyond lead recycling and strengthen its non-ferrous portfolio.

This move suggests organised players are positioning for scale in copper recycling, indicating expectations of sustained scrap inflows rather than a temporary spike. Corporate capital entering the segment reinforces the view that India’s copper ecosystem is structurally shifting toward a higher secondary share in the overall metal balance.

India’s refined copper output rises

India’s refined copper production increased significantly by 36% m-o-m in December 2025 to 64,000 t from 47,000 t in November 2025. The increase was largely driven by higher output from Hindalco, which produced 36,000 t in December compared to 31,000 t in November, reflecting a 16% rise. Kutch Copper recorded the strongest growth, with production surging to 13,000 t from just 1,000 t in November, indicating a substantial ramp-up in operations. Meanwhile, Sesa Sterlite maintained stable output at 15,000 t in both months. The overall m-o-m improvement highlights stronger operating rates and capacity utilisation across key producers in December.

Outlook

India’s copper outlook remains firm in the near term. Scrap imports are expected to stay elevated as mills increasingly use secondary material to offset lower cathode imports and optimise costs. With LME prices sustaining above $13,000/t and Chinese demand stable, global sentiment remains supportive. New recycling capacities and higher domestic operating rates will keep scrap demand strong. Unless global prices correct sharply or downstream demand weakens, imports and domestic premiums are likely to remain supported.

Leave a Reply