- Secondary smelter utilisation improves sharply

- Diversified sourcing supports steady inflows

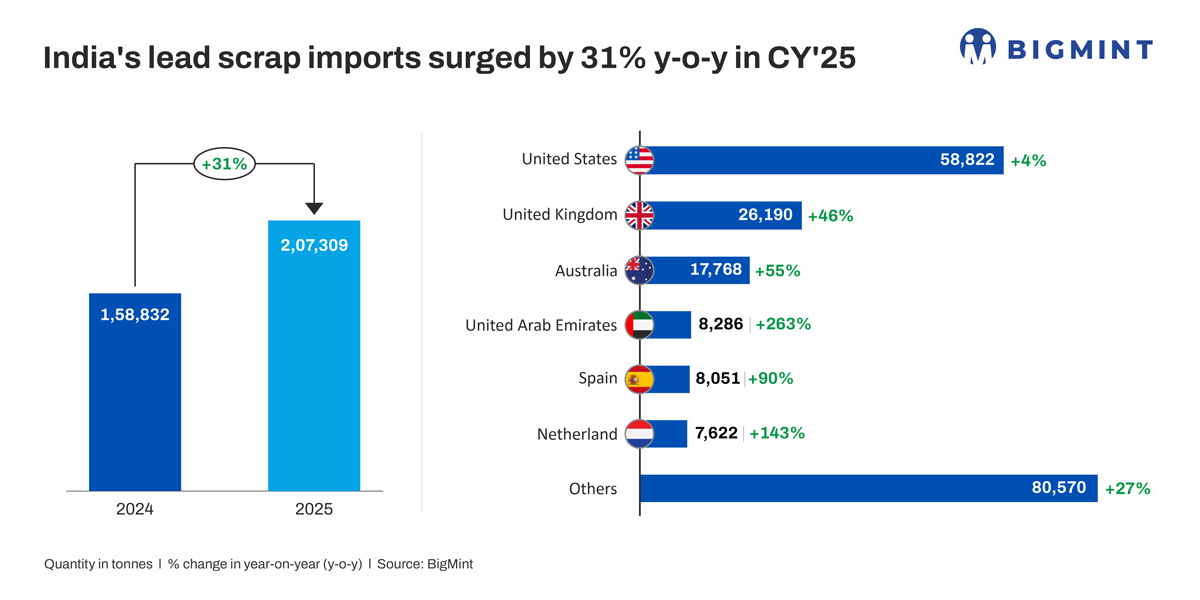

India’s lead scrap imports increased by 31% y-o-y in CY’25 to 207,310 tonnes (t), compared with 158,832 t in CY’24, reflecting a clear strengthening of secondary lead consumption. Buying interest remained consistently firm through the year, with monthly arrivals largely above 14,000 t, unlike the sharp fluctuations seen in CY’24. Imports peaked during July-August 2025, crossing 20,000 t per month, as recyclers stepped up procurement amid improved overseas scrap availability and restocking activity.

Supply diversification gathers pace

The United States remained India’s largest supplier, shipping 58,822 t, marginally higher by 4% y-o-y. However, growth was more pronounced from alternative origins, underscoring diversification in sourcing. Imports from the United Kingdom rose 46% y-o-y to 26,190 t, while Australia recorded a 55% increase to 17,768 t. Shipments from the UAE surged 263% y-o-y to 8,286 t, and Spain and the Netherlands also posted sharp double-digit growth. The widening supplier base reflects India’s growing reliance on multiple regions to secure adequate scrap feedstock for secondary smelters.

Grade mix tilts towards battery scrap

Grade-wise data highlights a clear preference for higher-yield, battery-related material. Radio scrap dominated imports, rising sharply to 133,070 t in CY’25 from 82,509 t in CY’24. Relay scrap imports increased to 33,012 t, while rink scrap declined to 22,424 t, indicating reduced appetite for lower-yield grades. Other minor grades such as ropes, racks, and rails remained marginal. The shift in the grade mix mirrors steady demand from the automotive and inverter battery replacement segments.

South India anchors consumption

On the consumption side, southern India remained the largest hub, accounting for 146,896 t of lead scrap intake in CY’25. This was followed by the west at 42,437 t, the north at 14,230 t, and the east at 3,738 t. Higher utilisation rates and capacity additions at secondary smelters in the south and west supported the elevated intake, reinforcing these regions’ dominance in India’s secondary lead ecosystem.

Key factors boosting imports

- Stronger secondary smelter utilisation: Secondary lead smelter utilisation improved to an estimated 75-80% in CY’25 from 65-70% in CY’24, driven by capacity additions and better operating efficiencies, particularly in southern and western India. Higher operating rates lifted feedstock requirements, while domestic scrap availability grew at a slower pace, directly translating into increased dependence on imported lead scrap

- Steady battery replacement demand: Lead demand remained structurally supported by automotive SLI and inverter batteries, which together account for 75–80% of total lead consumption. Stable replacement cycles of 3–4 years for automotive batteries and 2.5–3 years for inverter batteries ensured consistent offtake for recycled lead, encouraging recyclers to secure long-term scrap supplies through imports.

- Favourable international pricing: Average LME lead prices declined 5% y-o-y in CY’25, lowering CIF procurement costs for imported scrap. At the same time, domestic recycled lead prices stayed relatively firm due to steady battery demand, preserving recycler margins and widening the import arbitrage window.

- Rising LME inventories: LME lead stocks increased 19% y-o-y in CY’25, indicating improved global availability and easier circulation of lead-bearing material. Higher visible inventories reduced supply-side tightness and sourcing risks, supporting higher scrap flows into import-dependent markets.

- Preference for high-yield scrap grades: Imports increasingly shifted toward radio scrap and battery scrap, which typically deliver 65–75% lead recovery, significantly higher than mixed or low-grade scrap. The sharp rise in radio scrap imports reflects recyclers’ focus on maximising recovery rates, improving furnace efficiency, and lowering per-ton processing costs amid tighter compliance norms.

- Broader sourcing base: CY’25 saw rapid growth in shipments from the UK, Australia, UAE, and parts of Europe, reducing dependence on any single origin. A more diversified sourcing base improved supply security, enhanced price discovery, and enabled smoother procurement throughout the year.

Pricing and LME influence

Lead prices on the London Metal Exchange (LME) softened on a y-o-y basis in CY’25 amid ample global availability and a steady build-up in exchange inventories. The LME 3-month lead price averaged around $1,994/t, down nearly 5% y-o-y from $2,105/t in CY’24, with prices largely trading below the $2,000/t mark for most of the year. This contrasted with CY’24, when prices frequently stayed above $2,100/t. The weaker price trend coincided with a 19% y-o-y rise in LME lead stocks, which averaged close to 247,000 t in CY’25 and capped upside momentum.

What lies ahead in CY’26?

Looking forward, India’s lead scrap imports are expected to remain firm, supported by ongoing expansion in the secondary lead sector and steady battery replacement demand. Continued preference for battery-linked scrap grades is likely to shape procurement patterns. However, volatility in LME prices and tightening environmental and compliance norms could influence sourcing strategies and buying momentum.

Leave a Reply