- Lower grades struggle to generate interest, auctions fetch poor response

- NMDC’s volumes decline 22% due to dispatch-related constraints

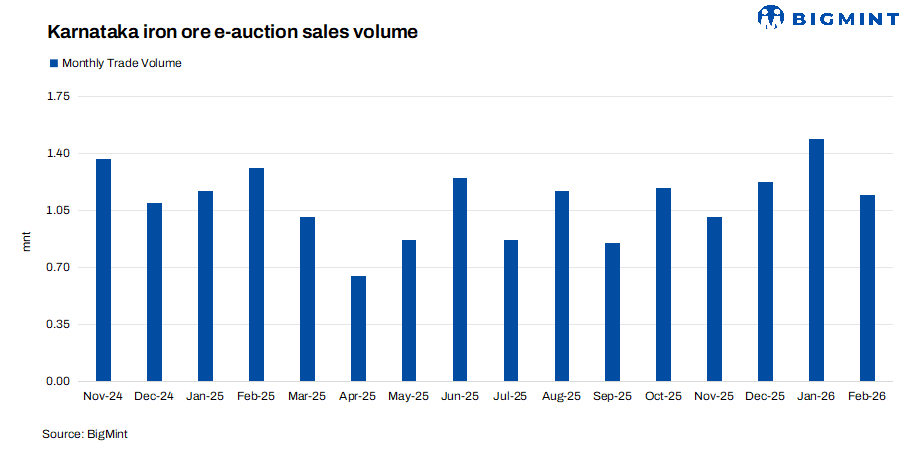

Iron ore e-auction sales in Karnataka declined by 23% m-o-m in February 2026 to 1.15 million tonnes (mnt), compared to 1.49 mnt in January, according to BigMint data. Out of the total quantity sold, iron ore fines accounted for approximately 660,000 tonnes (t), while lumps stood at 487,250 t.

The relatively weaker performance of lumps (with sales down 26% m-o-m from 658,850 t in January) highlights subdued demand for this segment, as buyers continued to show a clear preference for fines amid evolving consumption patterns.

Although the sponge iron segment showed signs of recovery during the month, it did not lead to aggressive raw material procurement. Sponge CDRI prices rose by INR 300/t ($3/t) m-o-m to INR 26,656/t ($284/t) in February 2026 from INR 26,358/t ($280/t) in January 2026.

Buyers largely remained cautious, backed by sufficient inventory levels accumulated earlier. This inventory overhang restricted fresh buying interest, ultimately resulting in muted auction response despite improving downstream activity.

A key trend observed during February was the continued preference for high-grade iron ore. Auctions offering superior-grade material witnessed healthy participation and better price realisation.

In contrast, low-grade material struggled to generate interest, with several auctions receiving poor or no bids. Even price reductions by smaller miners failed to stimulate demand, underscoring buyers’ increasing focus on quality and operational efficiency.

NMDC retains market leadership despite volume dip

NMDC Ltd. maintained its leadership position in Karnataka’s e-auction market, recording sales of 0.87 mnt in February. However, this marked a 22% m-o-m decline from 1.12 mnt in January. The total sales included 628,000 t of fines and 242,000 t of lumps.

The dip in NMDC’s volumes was partly attributed to dispatch-related constraints during the month, which offset the marginal improvement seen in sponge iron demand. It has been observed that NMDC Ltd. has predominantly offered low-grade material from its Kumaraswamy mines in most auctions.

Other miners show diverging trends

Sandur Manganese and Iron Ore Limited (SMIORE) emerged as the second-largest seller, recording a sharp rise in sales to 182,000 t in February, compared to just 63,000 t in January. This growth was driven by improved pricing strategies and stronger buyer participation.

Vedanta Limited ranked third, selling 48,000 t of lumps, including siliceous and haematite grades (till 18 February). However, the results for 57,000 t of lumps are pending.

Sri Kumaraswamy Minerals Private Limited (SKMEPL) reported modest growth, selling around 20,000 t of lumps versus 16,000 t in January.

Similarly, R Praveen Chandra recorded a significant jump, with volumes rising to 19,250 t from just 3,850 t in the previous month.

Karnataka State Minerals Corporation Limited (KSMCL) witnessed a steep 96% decline in sales, with only 8,000 t of low-grade lumps booked in February, compared to 224,996 t in January.

Auctions conducted by U Krishna Prasad once again failed to attract meaningful bids, despite further reductions in base prices. This trend clearly reflects a structural shift in buyer behaviour where quality, consistency, and usability outweigh mere price advantages.

Iron ore price trends in February presented a mixed picture

Weighted average prices of Fe 60% fines increased by INR 300/t m-o-m to INR 3,400/t. Fe 63% lumps remained stable at INR 4,400/t. The rise in fines prices was driven by the tight availability of high-grade material and sustained demand. Meanwhile, lumps demand remained subdued, as several buyers shifted towards sponge iron/PDRI routes due to better cost efficiency, limiting upward price movement.

Outlook

Karnataka’s iron ore e-auction market is expected to witness a gradual recovery in the coming months, supported by year-end inventory liquidation by miners and a seasonal uptick in demand during the summer period. Improved momentum in infrastructure and construction activities is likely to strengthen downstream steel demand, which in turn will drive higher raw material procurement. While buying may remain selective with a continued focus on high-grade material, overall auction participation and volumes are anticipated to improve steadily.

Leave a Reply