- NMDC emerges as leading miner in H1CY’25

- Pre-monsoon restocking in May-Jun’25 kept sales supported

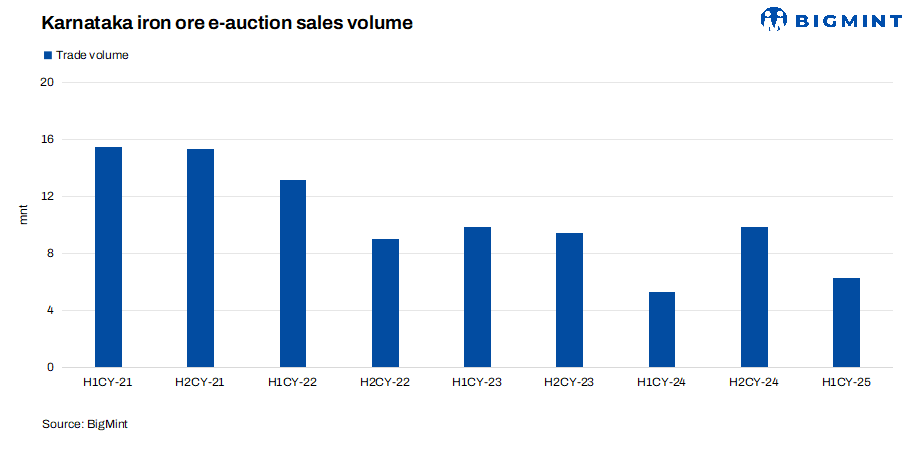

Karnataka’s iron ore e-auction sales witnessed an increase in the first half (January-June, 2025) of the calender year 2025 (H1CY’25). Sales volumes stood at 6.26 million tonnes (mnt), up by 19% y-o-y from 5.31 mnt in H1CY’24, as per BigMint’s data. H1CY’25 volume comprised 3.3 mnt of fines and 2.96 mnt of lumps.

Furthermore, June saw 1.25 mnt of iron ore sold through e-auctions, significantly increasing by 44% compared to around 0.87 mnt in the previous month. June’s volume comprised 689,000 tonnes (t) of fines and 545,000 t of lumps.

Factors which supported iron ore e-auction sales:

- Improved buyer participation post-Dec’24 slowdown: Buyer interest picked up in early 2025, following dull procurement activity in December 2024. Low procurement in the last month of CY’24 created pent-up demand that spilled over into the new year. Buyers, having deferred purchases earlier, entered the market with renewed appetite, driving up sales volumes.

- Karnataka iron ore production up sharply y-o-y: Karnataka’s iron ore production rose sharply by 19% y-o-y to 24.5 mnt in H1CY’25. NMDC remained the leading producer in H1CY’25 with its output rising 6% y-o-y, with the miner setting a guidance of around 55.4 mnt for FY’26.

- Favourable demand-supply dynamics: The regional demand-supply balance improved in H1CY’25. On the one hand, some supply was constrained due to temporary factors like delayed ECs and logistical issues; on the other, demand from sponge iron and pellet plants remained steady. This mismatch supported steady bidding in auctions, especially for higher-grade material. The favourable balance helped push up volumes even when offered material was relatively modest.

- Recovery after MRT-driven uncertainty, protests: The MRT Bill announcement in December 2024 had caused confusion in the mining industry, impacting auction activity in early 2025. However, with the Bill still pending, the market is abiding by the existing set-up.

Miners’ iron ore sales via auction outcomes:

- NMDC led the market with sales of 4.44 mnt in H1CY’25, up 24% y-o-y from 3.57 mnt in H1CY’24. In June alone, it sold 944,000 t (comprising 588,000 t of fines and 356,000 t of lumps), up 24% m-o-m.

- KSMCL recorded sales of 0.63 mnt, reflecting a 7% y-o-y decline from 0.68 mnt in H1CY’24. In June, it sold 48,000 t of fines and 24,000 t of lumps.

- SMIORE posted sales of 0.88 mnt in H1CY’25 so far, a 29% y-o-y increase compared to 0.68 mnt in H1CY’24. During June month, it sold 48,000 t of fines and 149,000 t of lumps.

- Vedanta sold 0.19 mnt in H1CY’25, down 27% y-o-y from 0.26 mnt in H1CY’24. However, only one auction was conducted in Jun’25, which remained unsold.

Company-wise volumes in H1CY’25 vs H1CY’24

Iron ore prices decrease y-o-y: The yearly weighted average prices of iron ore lumps and fines dropped y-o-y. Weighted average prices of Fe 60% fines stood at INR 3,467/t in H1CY’25, a drop of around INR 575/t y-o-y against INR 4,042/t in H1CY’24. Meanwhile, weighted average prices of Fe 63% lump prices were at INR 4,692/t, a decrease of INR 200/t y-o-y against INR 4,892/t in H1CY’24. Prices are exclusive of taxes.

Outlook

Karnataka’s iron ore e-auction sales volumes are expected to remain volatile in the coming months due to seasonal and market-driven factors. With the onset of the monsoon, logistical challenges and mining disruptions are likely to impact supply and dispatches, leading to reduced auction activity. Moreover, most buyers have already completed pre-monsoon restocking, which may result in subdued demand in the coming months.

Leave a Reply