- High-grade ore prices rise amid supply constraints

- Quality concerns and dispatch delays keep buyers selective

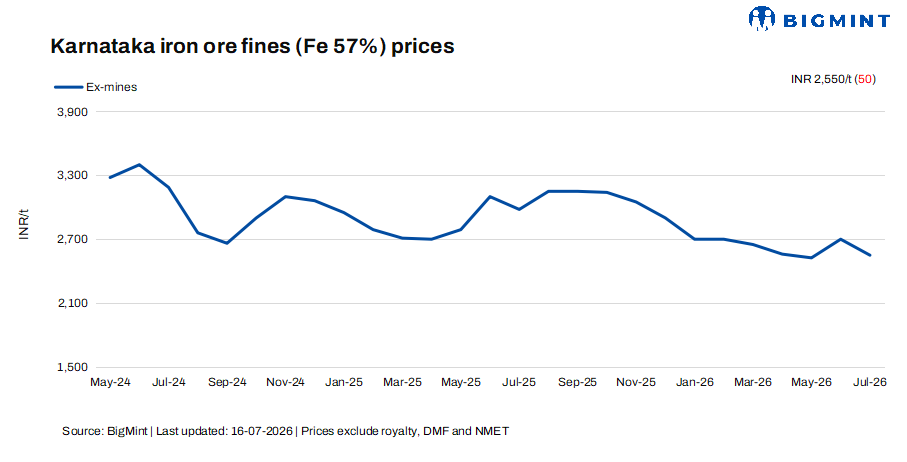

Iron ore prices in Karnataka remained largely unchanged during the week, with divergent price trends across grades reflecting contrasting supply-demand fundamentals. Weak demand from sponge iron producers and downstream steelmakers continued to weigh on procurement of lower-grade ore, while limited availability of high-grade material supported premium-grade prices.

According to BigMint’s latest assessment, Fe 57% iron ore fines declined by INR 50/t ($0.5/t) w-o-w to INR 2,550/t ($26/t) ex-mines. Demand for lower-grade material remained weak as sponge iron producers increasingly preferred higher-grade ore to improve productivity, reduce fuel consumption and optimise production costs. With ample availability of Fe 57% fines and limited buying interest, suppliers were compelled to lower prices to attract buyers.

In contrast, benchmark Fe 62% iron ore fines increased by INR 100/t ($1/t) w-o-w to INR 5,000/t ($52/t) ex-mines. The increase was driven by strong preference for high-grade ore coupled with limited availability in the region. Sponge iron producers continued to favour low-alumina, higher-grade material to improve metallic yield and furnace efficiency, while only a few miners were able to consistently supply such grades. Although overall market demand remained subdued, the scarcity of quality material prevented prices from softening. However, market participants noted that even premium-grade auction lots attracted only limited bidding as weak downstream steel demand continued to discourage aggressive procurement.

Auction activity remained muted during the assessment period, with only a few auctions conducted and buyer participation remaining below expectations. Consumers continued to favour direct purchases and discounted spot offers over bidding at fixed reserve prices. Reflecting the subdued market sentiment, NMDC reduced the price of Doni lumps (10-40 mm, Fe 53%) by INR 81/t ($1/t) to INR 2,096/t ($22/t) from INR 2,177/t ($23/t) in its auction held on 15 July. Despite the price reduction, the entire quantity offered remained unsold, highlighting the cautious procurement strategy adopted by buyers.

Supply-side constraints, however, continued to persist despite weak demand. Market participants reported increasing dispatch delays, with material purchased in earlier auctions yet to be delivered. The slower movement of ore has reduced spot availability and created a temporary shortage in the merchant market despite subdued consumption. Sources attributed the delays to lower mining activity, while several operational mines have either suspended production or diverted output towards captive consumption. As a result, buyers requiring immediate deliveries continued to face supply constraints, particularly for higher-grade material.

A Bellary-based miner told BigMint, “Demand remains weak as sponge iron producers are not receiving adequate support from downstream steel sectors. Buyers have also become increasingly selective because ore quality varies significantly across mines.”

A regional buyer said, “Low-grade iron ore is primarily purchased for blending purposes. However, with limited availability of high-grade material, buyers are unable to optimise blending ratios, which has reduced procurement of lower-grade ore as well.”

Rationale

- Zero (0) trade via e-auction was recorded for Fe 57% in this publishing window and was not taken into consideration. Hence, the T1 trade category was accorded 0% weightage.

- fifteen (15) offers and indicative prices were reported, out of which twelve (12) were considered as T2 trades. These were accorded 100% weightage.

C-DRI prices rise by INR 150/t ($1.5/t) w-o-w in Bellary: Meanwhile, Bellary’s coal-based sponge iron (C-DRI) prices increased by INR 150/t ($1.5/t) w-o-w to INR 26,150/t ($274/t), supported by tighter spot availability and expectations of higher non-coking coal prices. Market participants said anticipated increases in coal costs, driven by ongoing geopolitical tensions, encouraged some buyers to secure sponge iron before production costs rise further.

Consequently, iron ore buying continued to be driven by immediate production requirements rather than inventory building. Buyers also maintained a preference for pellets and higher-grade ore over lower-grade fines to improve furnace efficiency and offset rising fuel costs.

Karnataka iron ore sales scenario (10- 16 July 2026)

Outlook

Karnataka’s iron ore market is expected to remain largely stable in the coming weeks, with lower-grade material may remain under pressure due to weak demand, while high-grade ore is expected to stay supported by limited supply. Although rising non-coking coal prices may continue to support sponge iron prices by increasing production costs, higher input costs alone are unlikely to stimulate iron ore demand. Instead, pressure on sponge iron producers’ margins and sluggish finished steel demand are expected to keep procurement largely need-based. Market participants will closely monitor coal price movements, sponge iron operating rates and downstream steel demand, which will remain the key factors influencing iron ore prices in Karnataka.

Leave a Reply