- Market awaits upcoming auction results

- Supply crunch in both high, low grade ore

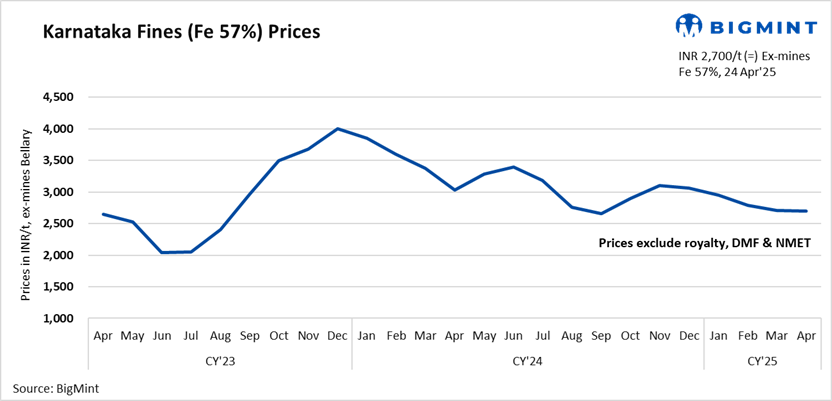

Domestic low-grade iron ore fines (Fe 57%) prices remained flat this week in Karnataka’s Bellary region. BigMint’s weekly index for the same (Fe 57%) stood unchanged w-o-w at INR 2,700/tonne (t) ($32/t) ex-mines Bellary (excluding taxes).

Similarly, the Fe62% fines index was assessed at INR 4,800/t ($56/t) ex-mines Bellary, including taxes. Additionally, some offers were noted at higher levels, that is INR 5,150/t ($60/t), due to a demand-supply mismatch in the region. However, no deals were concluded at these offers, as buyers were not yet ready to accept the increased prices.

Notably, the National Mineral Development Corporation (NMDC) has rolled over iron ore prices, which, along with material shortages, helped sustain domestic prices. However, domestic trades remained weak ahead of incoming imported iron ore cargoes, with no significant sales through either e-auctions or direct channels.

NMDC Karnataka’s list prices of iron ore fines (-10 mm, Fe 58%) and lumps (10-40 mm, Fe 58%) stood at INR 3,537/t ($41/t) and INR 4,224/t ($49/t), respectively, for the Donimalai auction on 23 April 2025. List prices remained unchanged from the previous revision on 24 March 2025. However, BigMint is still awaiting auction results from the Donimalai and Kumaraswamy mines.

A source told BigMint that the merchant market remains short on both low and high-grade iron ore, as some miners have resumed production but are still not actively offering material. Commenting on the lack of current offers in the merchant market, a major regional miner stated, “We are still awaiting environmental clearance (EC) to begin fresh production.”

Another miner from Bellary said, “Our focus is currently on dispatching previous bulk orders, given the large volume involved.”

Rationale

- Zero (0) trades were recorded for Fe 57% in this publishing window, so T1 trade received 0% weightage.

- Fourteen (14) offers and indicative prices were reported, out of which twelve (12) were considered as T2 trades. Hence, this category was accorded 100% weightage.

Outlook

Domestic low-grade iron ore prices are likely to stay under pressure amid ongoing uncertainty around the proposed mineral rights tax (MRT) Bill. Meanwhile, sponge iron manufacturers are increasingly turning to alternative sources like South Africa and Brazil for cost efficiency and supply stability, a trend that may further impact domestic trade in the near term.

Leave a Reply