- Crude steel output up 15% y-o-y but falls q-o-q

- Share of value-added products increases in sales mix

JSW Steel reported solid operational performance in Q1FY’26 with both crude steel production and sales volumes registering strong growth. The company maintained its full-year volume guidance despite planned maintenance shutdowns and continued to ramp up operations at its Vijayanagar facility.

Consolidated capex spending for Q1 stood at INR 3,400 crore, bringing the total cumulative spend to approximately INR 12,000 crore so far in FY’26.

Update on key projects

JVML (Vijayanagar): Produced 0.75 mnt in Q1. The second converter is expected to be commissioned in Q2. A blast furnace upgrade (BF3) is planned for September to enhance capacity by 1.5 mnt.

Dolvi Phase 3 expansion (from 10 to 15 mnt) is on track for completion by September 2027.

Cold rolling projects: New 0.6 mnt facility at Khopoli and a 0.4 mnt galvanising line at Vijayanagar to support appliance and automotive segments.

Electrical steel: A new 0.55 mnt CRNGO facility at Vijayanagar has been approved to meet rising demand from motors and transformers.

Iron ore mines: JSW Steel plans to commence mining operations at the Cudnem iron ore mine in Q3, while the Surla-Sonshi mine is expected to start production in the second half of FY’27. Together, these Goa-based mines are projected to yield approximately 3.7 mnt of iron ore annually.

Coal mines: The company continues to advance development of its three captive coking coal mines in eastern India, along with washeries at Parbatpur and Dukda. In addition, JSW Steel has secured a 5 mnt coal linkage from Coal India. Combined, these domestic sources are expected to supply around 3.2 to 3.5 mnt of usable coking coal annually over the next two to three years.

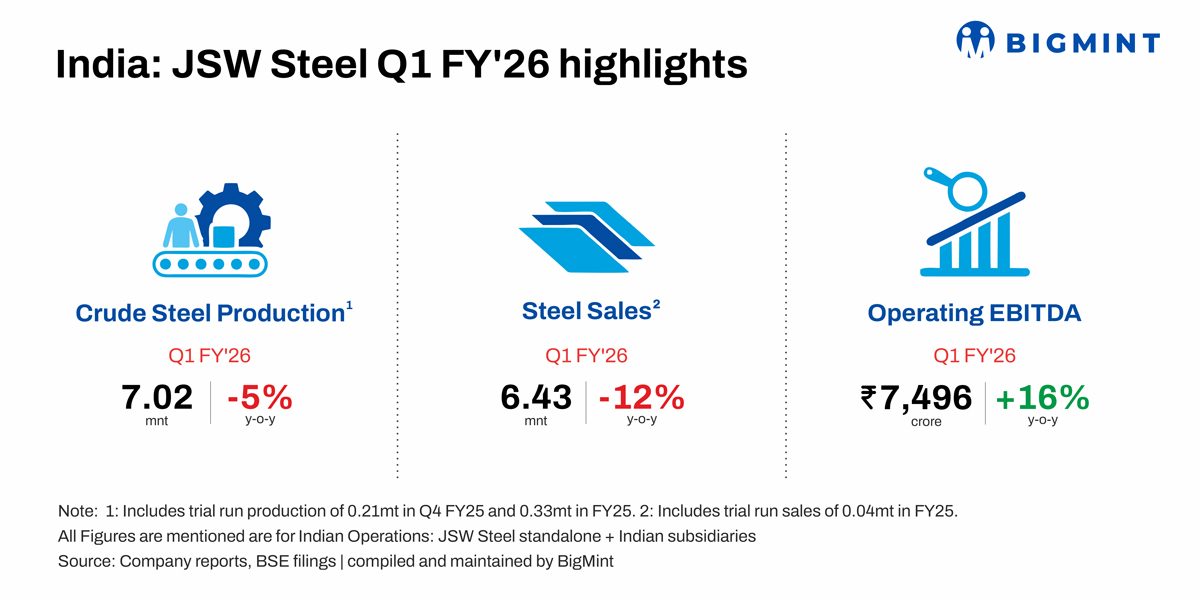

Crude steel production up y-o-y: JSW Steel’s Indian operations produced 7.02 mnt, up 15% y-o-y. However, on a q-o-q basis, production declined 5% due to planned maintenance shutdowns that led to lower capacity utilisation at 87%.

Steel sales show robust y-o-y growth: Steel sales volumes reached 6.43 mnt, up 9% y-o-y. However, on a q-o-q basis, sales declined 12% from 7.27 mnt in previous quarter. Share of export stood at 7%, marginally lower than the previous quarter. Sales of value-added and special products (VASP) contributed 64% to the total, marking the highest-ever quarterly share.

JSW Steel has demonstrated robust growth driven by its value-added and special products (VASP) portfolio. The company achieved its highest-ever VASP sales, reaching 3.91mnt, which represents a 2.6% y-o-y increase. This growth was particularly notable across several key segments:

- Automotive: Sales to the automotive sector surged 20% y-o-y, marking a new peak for the company in this category.

- Alloy long products: Sales of alloy long products saw a significant 19% increase.

- Appliances: The appliances segment also showed strong performance with a 27% rise in sales.

These impressive gains are attributed to improved market demand and JSW Steel’s expanded market penetration, facilitated by its extensive retail network of over 2,400 branded outlets.

Operating EBITDA rises q-o-q: Consolidated operating EBITDA for Indian operations contributed INR 7,496 crore to EBITDA at a healthy 18.5% margin. Improved product mix and a partial benefit from lower coking coal prices supported profitability, although forex losses of INR 343 crore due to euro appreciation impacted earnings.

Iron ore & coking coal costs: Coking coal costs declined by $14/t q-o-q, aiding EBITDA. The company expects a further $5/t reduction in Q2. While iron ore costs remained stable, increased captive sourcing (39% in Q1) helped offset imported price pressures. Ramp-up of three captive coking coal mines and washeries in eastern India is expected to supply 3–3.5 mnt annually over the next two-three years.

Net sales realisations (NSR): NSR improved by approximately INR 3,300/t q-o-q in Q1 due to price hikes in April and May. However, steel prices softened in June-July due to seasonal slowdown and import pressures. JSW expects realisations to decline in Q2 but aims to offset part of the impact through cost efficiencies and higher volumes.

Leave a Reply