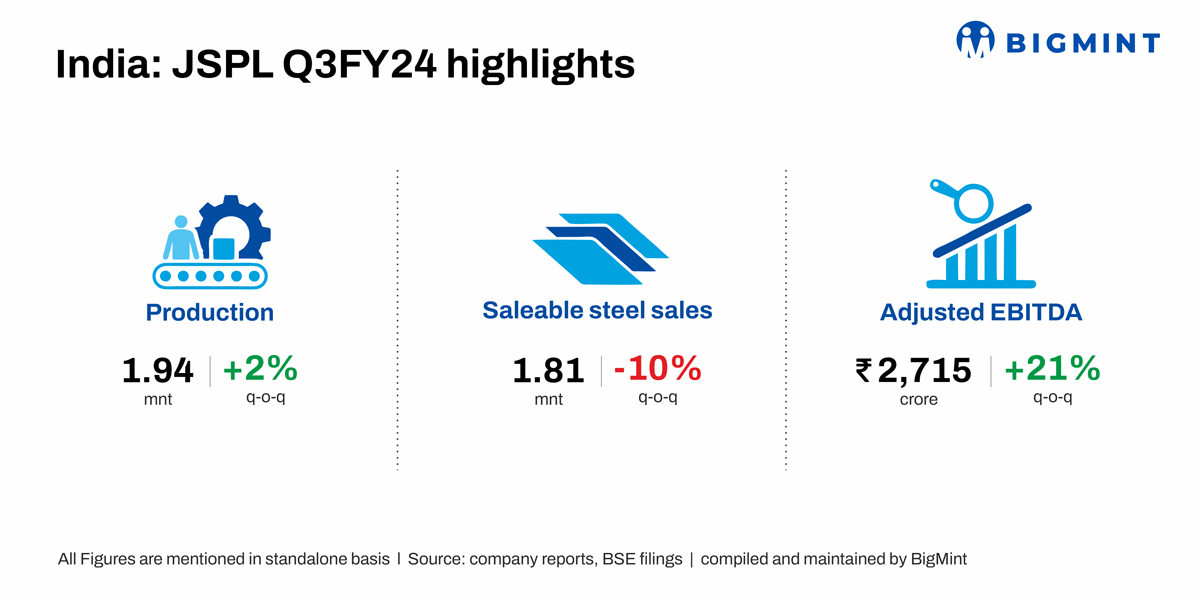

The production of Jindal Steel & Power Limited (JSPL) edged up by 2%, while sales decreased by 10% q-o-q in Q3FY24, BigMint learnt from the company’s investors call held on 31 January 2024.

Update on projects at Angul:

- The hot strip mill (HSM) and pellet plant-1 are commissioned.

- The slurry pipeline is expected to be commissioned in Q1FY25.

- The commissioning of BOF-II with a capacity of 3.3 million metric tonnes per annum (MTPA), along with other facilities such as the Air Separation Unit (ASU), Coke Oven, and Raw Material Handling System (RMHS), is scheduled for the second quarter of the fiscal year 2025. Additionally, Blast Furnace-II with a capacity of 4.6 MTPA, and Advanced Combined Power Plant (ACPP)-II generating 1050 megawatts, is also set to commence operations by Q2FY25.

Other highlights

Production edges up q-o-q: The company’s production edges up by 2% q-o-q to 1.94 million tonnes (mnt) in Q3FY24(Q3) as against 1.9 mnt in the previous quarter. However, the same was down by 6% y-o-y from 2.06 mnt in Q3FY23.

Steel sales fall q-o-q: Steel sales stood at 1.81 mnt in Q3, down by 10% q-o-q from 2.01 mnt in the preceding quarter. The same was down by 5% y-o-y from 1.9 mnt in Q3FY’23.

The value-added product/grade sales contributed to 65% of total sales in Q3FY24. The share of exports fell to 3% of total sales.

Major chunk of domestic sales came from infrastructure sector contributing to about 40% of domestic sales followed by trade/retail sales with 33%. Moreover, building and construction, engineering & packaging and automotive sectors contributed 13%, 11% & 4% in domestic sales, respectively.

EBITDA falls q-o-q: The company’s adjusted EBITDA rose by 21% in the quarter to INR 2,715 crore in Q3 as against INR 2,244 crore in the previous quarter. Also, the same increased by 26% y-o-y from INR 2,163 crore in Q3FY23.

Net sales realisations (NSR): The company witnessed a 4% enhancement in its net sales realisations (NSR) in the current quarter, attributable to the robustness observed in steel prices.

Operational costs: The cost of steel melting shop (SMS) increased by 2% on the quarter majorly due to increase in coking coal and iron ore prices. The coking coal prices were up by $32/t in the quarter. The price of coking coal is expected to increase by $10-20/t in Q4. The average cooking coal prices for the quarter were $281 as against $249 in the previous quarter.