- Angul expansion nears completion

- Coking coal costs decline q-o-q

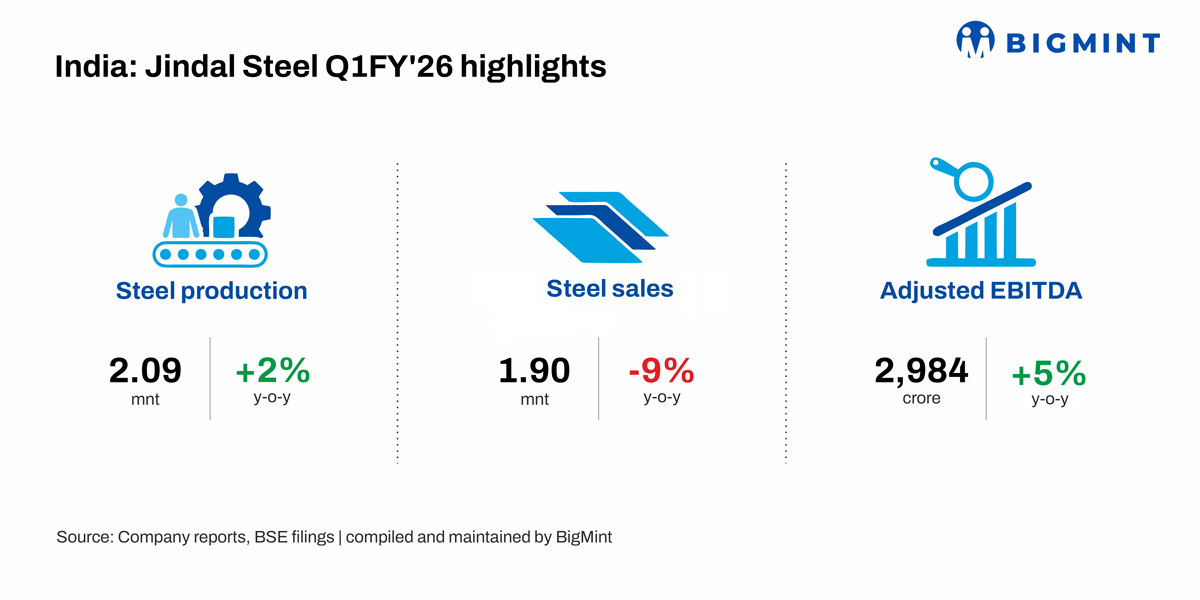

Jindal Steel Ltd’s steel production edged up 2% y-o-y to 2.09 mnt, while steel sales witnessed a drop of 9% y-o-y to 1.90 mnt in Q1FY26. The total capex for Q1FY26 was INR 2,226 crore, largely allocated to expansion of the Angul facility.

Update on key projects

Angul expansion

- Final stage commissioning of India’s 2nd-largest 5,499 m³ blast furnace at Angul. First hot metal tapping is expected in Q2FY26.

- BOF-2 is undergoing pre-commissioning tests

- 0.20 mnt/year continuous galvanising line (CGL-1) commissioned to boost value-added product capacity.

Mines update

The company secured the Roida-I Iron Ore and Manganese Block in Odisha, with an environmental clearance capacity of 3 mnt and estimated reserves of 126.05 mnt. Iron ore extraction has already commenced from this mine.

Other highlights

Steel production edges up y-o-y: The company’s steel production edged up by 2% y-o-y to 2.09 mnt in Q1FY26 as against 2.05 mnt in the same period last year. Meanwhile on q-o-q basis, the same edged down by 1% from 2.11 mnt in Q4FY25.

Steel sales decline y-o-y: Jindal Steel’s steel sales declined 9% on the year to 1.90 mnt during the quarter from 2.09 mnt in Q1FY25. The same witnessed drop of 11% q-o-q from 2.13 mnt in Q4FY25. Sales volumes declined due to inventory replenishment following significant drawdowns in Q4FY25, which is typically a seasonally strong quarter.

EBITDA rises y-o-y: The company’s EBITDA increased 5% y-o-y to INR 2,984 crores in Q1FY26 from INR 2,831 crores in Q1 of FY25. Likewise, on q-o-q basis, EBITDA rose 20% from INR 2,482 crores.

The company’s EBITDA per tonnes increased 16% on the year to INR 15,680 in Q1FY26 as against INR 13,527 seen in the same period of previous year. On quarterly basis, the same rose 35% from INR 11,651.

Steel price movements in Q1FY26: During the quarter, domestic steel prices showed mixed trends. HRC prices rose initially on safeguard measures but eased later amid weak demand. Rebar prices opened firm but declined due to early monsoon onset and ample inventories.

The blended average selling price (ASP) rose q-o-q, driven by higher steel prices and a 2% increase in the share of flats in the sales mix.

Raw material & operating costs: Total operating costs fell 15% q-o-q, driven by a 10% decline in sales volumes, lower coking coal prices, and reduced conversion costs from decreased repairs, maintenance, and stores/spares expenses.

Coking coal costs declined by $11/t, in line with guidance. For Q2FY26, the company expects a further $5/t reduction, while iron ore costs remain largely stable q-o-q.

Leave a Reply