- Sales volumes rise 11% y-o-y in 9M FY’26

- EBITDA and PAT post double-digit growth

India’s leading stainless steel producer, Jindal Stainless (JSL), reported a 23% y-o-y rise in profit after tax (PAT) to INR 2,350 crore in the nine months ended December 2025 (9M FY’26), supported by robust domestic demand and better cost management, even as export markets remained under pressure amid global trade uncertainty.

Sales, product mix

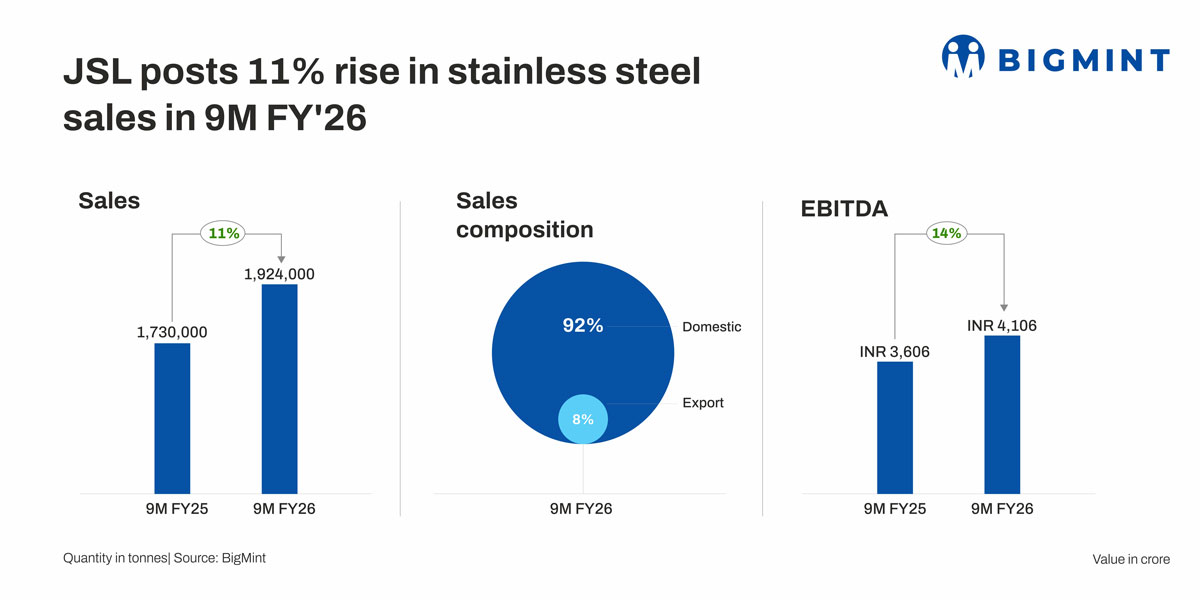

Sales volumes during 9M FY’26 stood at around 1.92 million tonnes, up nearly 11% year on year, driven by sustained demand from automotive, railways, metro projects, ornamental pipes and tubes, lifts and elevators, and white goods. Infrastructure-linked consumption continued to support offtake, while domestic sales accounted for about 92% of total volumes, with exports limited to around 8% due to policy uncertainty in the US and EU.

The grade mix remained was aligned with domestic demand trends, with the 300 series forming the largest share at 47%, followed by the 200 series at 36% and the 400 series at 17%. On a quarterly basis, sales volumes remained steady at 0.59 million tonnes in Q3 FY’26, broadly flat quarter on quarter and up 11% year on year, against 650,000 t in Q3FY’25.

EBITDA, cost performance

Consolidated EBITDA for 9M FY’26 stood at INR 4,106 crore, registering a 14% y-o-y increase, supported by operational efficiencies, higher value-added sales, and effective raw material cost pass-through despite volatility in nickel and ferrochrome prices.

Quarterly, EBITDA stood at INR 1,208 Cr in Q3FY’26, up 1% q-o-q as compared to INR 1,388 Cr and up by 27% y-o-y at INR 1,408 Cr in Q3FY’25.

Consolidated net debt declining to INR 3,451 crore as of December 2025. Net debt-to-equity and net debt-to-EBITDA ratios improved to 0.18 and 0.67, respectively.

Capacity utilisation, integration

Capacity utilisation improved steadily across facilities, supported by downstream ramp-up and better asset productivity. The cold-rolled (CR) share continued to increase, with CR accounting for about 70% of the combined HR-CR mix, aided by downstream investments and the Chromeni acquisition. All subsidiaries contributed positively to consolidated EBITDA, although a temporary shutdown at JUSL impacted volumes.

Subsidiaries & Integration

All subsidiaries delivered improved performance during the period and contributed positively to consolidated EBITDA. Volumes at JUSL were impacted by a temporary shutdown, although margin performance showed improvement.

Operations at Chromeni and the NPI venture continued to ramp up, with NPI operating at about 75% capacity utilisation, strengthening integration across the raw material value chain and reducing reliance on external sourcing.

Meanwhile, the Indonesian SMS project and downstream expansion projects in India are progressing as scheduled, with commissioning expected in FY’27.

Metro and infrastructure projects continued to support volumes, with Jindal Stainless receiving approval from Integrated Coach Factory (ICF) Chennai for the supply of stainless steel used in metro coach sidewalls for the Kolkata Metro project.

Market demand & exports

Domestic stainless steel demand remained firm during the period, supported by sustained activity across infrastructure, construction, metro and railway coach manufacturing, and elevators, alongside a gradual recovery in automotive consumption following GST adjustments. Process industries continued to provide a stable demand base, while railways and metros witnessed healthy offtake in Q3 FY’26, driven by higher coach additions and increasing adoption of austenitic stainless steel grades. Infrastructure consumption stayed resilient amid urbanisation and the rollout of BIS IS:17900, while demand from automobiles, pipes, and tubes remained supportive on festive sales and ongoing construction activity.

Exports continued to face headwinds due to CBAM-related uncertainties and protectionist measures, prompting the company to prioritise value-added domestic sales. Exports remained subdued due to geopolitical uncertainty, CBAM-related ambiguity, and protectionist policies in the US and EU; company consciously prioritised domestic sales to maximise EBITDA.

Outlook: Jindal Stainless expects domestic demand momentum to continue into Q4 FY’26, aided by infrastructure spending and stable consumption, while export volumes are likely to recover gradually once global policy clarity improves.

Leave a Reply