- Demand-supply gap widens for superior grades

- Coal cost surge and scrap shortage lift DRI prices

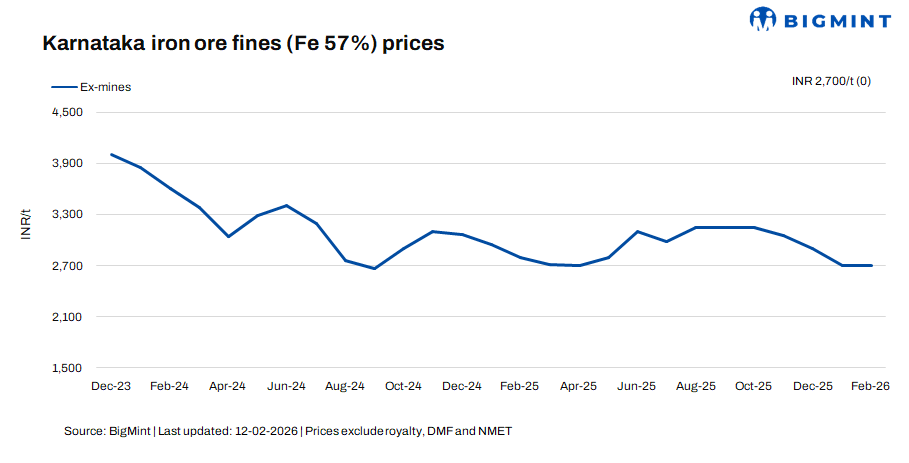

Domestic iron ore prices in Karnataka’s Bellary region continued to hold firm w-o-w as of 12 February, underpinned by steady procurement, active market participation, and constrained availability. Low-grade fines (Fe 57%) remained unchanged, with BigMint’s weekly index assessed at INR 2,700/t ($30/t) ex-mines, excluding taxes. Similarly, Fe 62% fines stayed stable at INR 5,100/t ($56/t) ex-mines, reflecting the market’s strong resistance to any downward correction despite evolving downstream dynamics.

However, beneath this overall stability, a clear divergence in grade-wise demand is emerging. The region is currently witnessing a shortage of high-grade material, while demand for superior-grade ore remains robust. Market participants noted that whenever high-grade lots are offered through auctions, they attract aggressive bidding and receive an overwhelming response from buyers. Limited availability from high-grade suppliers has further widened the demand-supply gap, intensifying competition for premium material.

In contrast, buying interest for lower-grade ores, particularly below 55% Fe, remains notably weak. Buyers are increasingly cautious and reluctant to procure inferior-quality material, especially cargoes with elevated silica and phosphorus content. Such grades are facing subdued enquiries and slower liquidation, highlighting a widening preference gap between premium and sub-par material.

Despite rising sponge iron and finished steel prices, raw material rates in Karnataka have maintained remarkable stability. Market participants believe that ore prices are already positioned at relatively elevated levels, leaving limited room for further upside. As one buyer remarked, “Raw material prices are already on the higher side, so we are not expecting any major correction at this stage.”

On the sponge iron front, prices have climbed, largely driven by higher coal costs and tightening scrap availability. However, trading momentum has slowed recently. A Bellary-based buyer commented, “Sponge prices are increasing due to rising coal prices and scrap shortage, but trading activity has eased since most buyers had already booked their requirements last week.”

Adding to the mixed sentiment, a Bellary-based miner highlighted the current auction challenges, stating, “Even after reducing the base price, our auction remained unsold, despite offering higher-grade material.” This reflects the selective buying approach adopted by participants, where price sensitivity and immediate consumption needs are dictating procurement decisions.

Overall, the Bellary iron ore market is demonstrating resilience in benchmark prices, but the underlying narrative reveals tightening high-grade availability, cautious buying behaviour for lower grades, and a carefully balanced demand-supply equation shaping near-term market direction.

NMDC has revised the base prices for its iron ore auction from the Donimalai mines in Karnataka on 10 Feb’26. Post-revision, fines (-10 mm, Fe 56%) stood at INR 2,177/t ($24/t), marginally up by INR 61/t ($1/t), while lumps (10-40 mm, Fe 55%) were at INR 1,995/t ($22/t), marginally up by INR 45/t ($0.5/t). Prices exclude royalty, DMF, and NMET

Rationale

- One (1) trade via e-auction was recorded for Fe 57% in this publishing window and was not taken into consideration. Hence, the T1 trade category was accorded 0% weightage.

- Sixteen (16) offers and indicative prices were reported, out of which eleven (11) were considered as T2 trades. These were accorded 100% weightage.

C-DRI prices edge up by INR 150/t ($2/t) w-o-w in Bellary: Prices of sponge iron (CDRI) in Bellary inched up by INR 150/t ($2/t) w-o-w to INR 26,850/t ($296/t), supported by firm pellet-based DRI prices and higher raw material costs. However, local demand slowed due to shortage of melting scrap, restricting fresh buying activity. Despite this, a few deals were concluded in down south and neighboring states, keeping overall market sentiment stable to slightly firm.

Karnataka iron ore sales scenario (6-12 February 2026)

Outlook

Low-grade iron ore prices in Karnataka are expected to remain largely unchanged in the near term, with limited upside potential. Weak buying interest, especially for material with higher silica and phosphorus content, may continue to cap price gains. However, firm sponge iron prices and stable raw material sentiment could provide some support, preventing any sharp correction. The movement in upcoming auctions and actual deal conversions will be key in determining whether prices hold steady or witness marginal fluctuations.

Leave a Reply