- Imported pellet supply tightens amid route disruptions

- Kandla’s steelmakers import lumps from South Africa

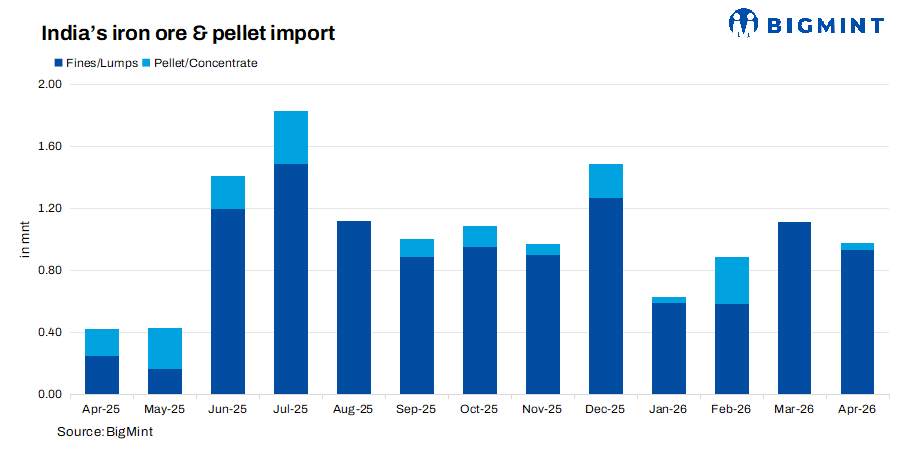

India’s iron ore (including pellets) imports stood at around 0.98 million tonnes (mnt) in April 2026, declining 11% from 1.11 mnt in March, but significantly higher compared to 0.38 mnt in April 2025, as per BigMint data. The total included 0.93 mnt of iron ore fines and lumps and 0.05 mnt of pellets, indicating that the bulk of the inflows continued to be ore, while pellet imports remained minimal. In comparison, iron ore fines and lumps comprised the entirety of the 1.11 mnt imported during March, while pellet imports were nil.

The resumption of pellet imports (sourced primarily from Oman) in April after a one-month gap suggests a partial stabilisation in shipping routes from the Middle East. However, overall import availability has tightened sharply, with pellet imports declining to just 0.05 mnt in March-April 2026 from 0.35 mnt in January-February.

Brazil, Malaysia dominate supply mix

Malaysia and Brazil emerged as the leading exporters during the month, contributing 0.34 mnt and 0.33 mnt, respectively. South Africa followed, with 0.15 mnt. The supply trend reflects continued diversification in sourcing, with steady inflows from both Southeast Asia and Atlantic basin suppliers. Most supplies were shipped to west coast-based plants.

JSW group leads import activity

Among buyers, JSW Steel dominated imports with 0.79 mnt, accounting for a major share of total volumes. This was followed by JSW Minerals at 0.15 mnt, while the remaining volumes were imported by other players. The concentration highlights strong procurement by integrated steelmakers.

Port-wise imports

On the logistics front, Jaigad Port handled the highest import volumes during April at around 0.51 mnt. The dominance of west coast ports reflects their proximity to key steelmaking hubs and ease of cargo handling for bulk imports.

Market scenario

- Domestic availability improves after EC renewals: Most domestic miners, along with several integrated steelmakers, received renewed environmental clearances (ECs) during April, improving ore availability in the domestic market. Regular auction flows and better local supply reduced dependence on imported cargoes, with many buyers limiting overseas procurement mainly to specific grade requirements. Indian miners’ total available EC capacity increased from 520 mnt in FY’26 to around 558 mnt in FY’27, following multiple EC renewals and capacity additions.

- South African lumps cargoes replace pellets: Pellet imports remained limited during April as disruptions around the Hormuz Strait impacted cargo movement through the Oman route. Amid reduced pellet inflows, South African high-grade lumps cargoes gained traction, particularly among Kandla-based buyers seeking stable raw material availability.

A few shipments that were booked in April are expected to arrive in May. Meanwhile, some inland plants continue to source from domestic raw material suppliers due to competitive prices. Additionally, a few bulk pellet domestic tenders from South India filled the void of imported pellets in the west coast market.

Outlook

India’s iron ore imports are expected to remain moderate in the near term, with buying likely to be driven by large steelmakers amid limited domestic availability of high-grade material. Import volumes will continue to depend on global prices, freight trends, and grade requirements from steel and DRI producers.

Leave a Reply