- Muted buying interest keeps Karnataka iron ore market subdued

- Rising inventories continue to pressure sponge iron prices

The Karnataka raw material market continued to witness a bearish trend during the week, primarily driven by subdued demand across the steel value chain. Persistent weakness in sponge iron and finished steel segments weighed heavily on overall market sentiment, resulting in cautious buying activity and lower participation in both spot and auction-based transactions.

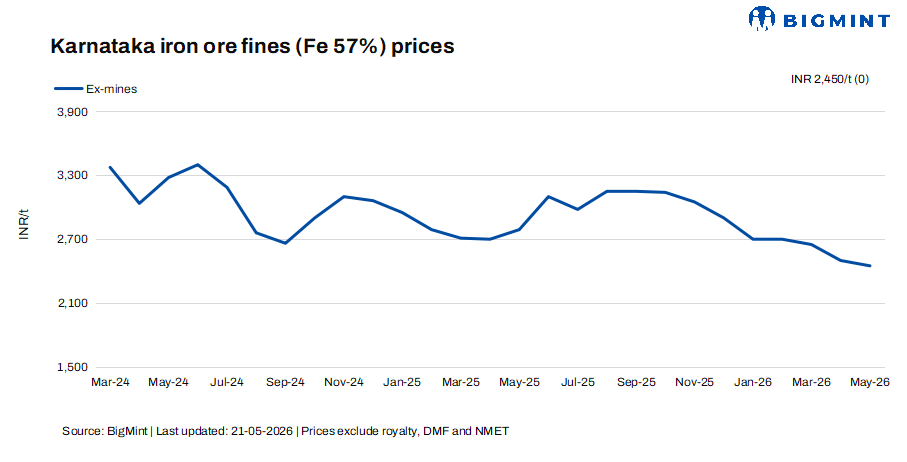

Prices of Fe 57% iron ore fines remained stable w-o-w at INR 2,450/t ($25/t) ex-mines. The lack of any upward movement was mainly attributed to muted buying interest and limited fresh enquiries in the market. Market participants indicated that low-grade material continues to face significant resistance, with consumption yet to show any meaningful improvement.

Meanwhile, prices of Fe 62% fines declined sharply by INR 200/t ($2/t) w-o-w to INR 4,750/t ($49/t) ex-mines. The correction was largely driven by the absence of fresh deals in both direct and auction markets, even at lower price levels, reflecting the cautious sentiment prevailing among buyers.

Despite the overall weak market environment, demand for high-grade material remained comparatively better supported. Availability of high-grade fines continues to be limited, with only a handful of miners actively offering such material in the market. Although demand fundamentals for premium-grade ore remain relatively stable, prices have also come under pressure owing to the broader market downturn.

Industry sources indicated that only select miners have been able to secure premium prices for high-grade fines through auctions and direct sales, while several other suppliers are struggling to maintain realizations amid weak market conditions.

Meanwhile, some smaller miners are facing challenges in accumulating sufficient inventory for upcoming auctions. Buyers are also becoming increasingly selective in procurement, with greater emphasis being placed on material quality and consistency before concluding purchases.

Market participants are now closely monitoring NMDC’s upcoming auction, expected to be conducted today. However, the base prices are yet to be announced. This will be the first auction from the Kumaraswamy mines in the new fiscal year and is expected to attract significant attention from traders, miners, and end-users alike due to its potential impact on regional pricing trends and market direction.

Commenting on current auction activity, a Bellary-based miner informed BigMint “Our previously auctioned material is yet to be fully sold due to logistical disruptions in our mining area. Even after the auction, dispatches generally take around 10-15 days to materialize.”

Sharing the demand-side perspective, a Bellary-based buyer stated “Coking coal prices have not increased significantly, and primary steel producers continue to maintain healthy margins, allowing them to procure material as required. However, sponge iron manufacturers are under severe pressure because RB2 and RB3 coal prices remain elevated.”

Rationale

- Zero (0) trade via e-auction was recorded for Fe 57% in this publishing window and was not taken into consideration. Hence, the T1 trade category was accorded 0% weightage.

- Fourteen (14) offers and indicative prices were reported, out of which nine (9) were considered as T2 trades. These were accorded 100% weightage.

C-DRI prices dip by INR 100/t ($1/t) w-o-w in Bellary: Prices of sponge iron (CDRI) in Bellary edged down by INR 100/t ($/t) w-o-w to INR 26,600/t ($276/t) primarily due to weak demand for finished steel products, particularly rebar, from end-user segments. Slow movement in the construction and infrastructure sectors has impacted steel offtake, creating pressure across the value chain and resulting in softer sentiments in the raw material market as well.

Additionally, conversion margins for steel and sponge iron manufacturers have remained under significant pressure. Rising operating costs coupled with weak finished steel realizations have reduced profitability levels, with several industries struggling to even achieve their break-even margins in the current market conditions.

Karnataka iron ore sales scenario (15-21 May)

Outlook

The Karnataka raw material market is expected to remain under pressure in the near term due to weak sponge iron and finished steel demand, elevated coal costs for secondary steel producers, and cautious procurement strategies adopted by buyers. Market participants are likely to closely monitor the outcome of NMDC’s Kumaraswamy auction for pricing cues and demand visibility.

Leave a Reply