- Export deals slow down, seaborne prices drop

- Exporters facing fines shortage during monsoon

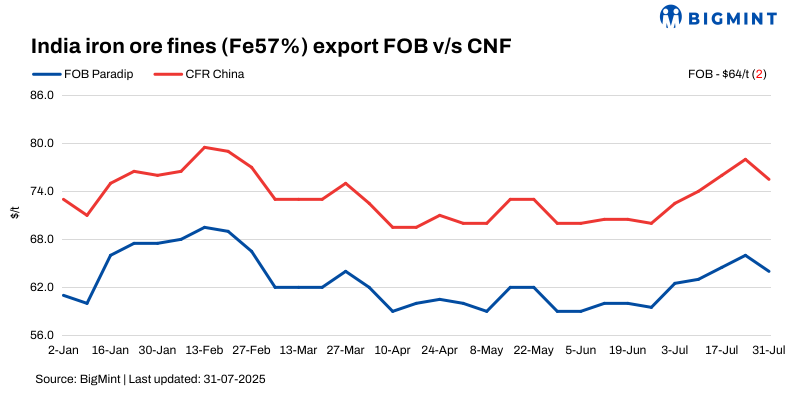

Iron ore prices in the export market witnessed a decline this week, mirroring the fall in Chinese iron ore prices. The drop in China is largely attributed to news of production curbs in North China, which has dampened buying sentiments across global markets.

Prices, deals

BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index fell by $2/t w-o-w to $64/t FOB east coast on 31 July. Around 165,000 t of Fe 55-57% fines were sold at $72-76/t CFR China in this publishing window.

Trade activity remained subdued over the past few days as market participants grappled with negative price fluctuations in the seaborne market. Exporters reported that the price correction of around $4-5/t has led to a cautious approach, with many buyers adopting a wait-and-watch stance.

Fe 57% fines were offered at a 17-19% discount, with many waiting for the August discount revision from Australian miners.

Iron ore and steel futures declined this week in China as new data showed that the country’s manufacturing sector slowed again in July, diminishing hopes for significant policy changes.

Market scenario

A market participant informed, “Despite the sluggish demand, few exporters were able to secure deals at the end of last week and the start of the current one. Several tenders are currently in the negotiation phase, but market sentiment remains uncertain.”

Exporters highlighted that while export inquiries exist, the domestic market is facing a material shortage. Heavy rainfall in India’s eastern mining regions has disrupted iron ore production and dispatches, creating challenges in replenishing export cargoes.

An exporter commented, “Miners in Odisha are struggling to meet dispatch schedules due to continuous rainfall. This has delayed restocking efforts for upcoming export commitments.”

As per reports, China’s manufacturing output has contracted for the fourth consecutive month, with fading export boosts and weak domestic demand. Steelmakers expected strong stimulus from the latest Politburo meeting, but officials only offered a slightly looser monetary policy and a more proactive fiscal approach, which disappointed markets. This led to declines in key commodities, with steel products like rebar and coil falling significantly.

Chinese spot prices fall w-o-w: Benchmark iron ore fines prices in China decreased by $3/t w-o-w at $101/t CFR on 30 July. Port prices dipped as interest weakened, although traders held firm on high-grade fines amid strong demand and wider Fe 65/62% spread. Production curbs and policy support kept mill margins stable, sustaining demand for pellets and lumps.

DCE iron ore futures down w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the September 2025 contract dropped by RMB 32/t ($5/t) w-o-w to RMB 779/t ($107/t) on 31 July.

Rationale

- One (1) deal for Fe 57% was recorded during this publishing window, and was taken for price calculation. Therefore, T1 trade was given 50% weightage in the index calculation. For the detailed methodology, click here.

- BigMint received twenty-five (25) indicative prices in the current publishing window, and nineteen (19) were considered for price calculation as T2 inputs and given 50% weightage.

Iron ore inventory at Chinese ports fell by 0.75 mnt w-o-w to 130.3 mnt on 31 July, as per SteelHome data.

Outlook

As per BigMint’s analysis, Indian export prices are expected to remain rangebound in the near term, with moderate deal activity anticipated unless there’s a significant shift in weather or policy developments.

Leave a Reply