- Miner sells cargoes at around 18% discount

- Market expects better clarity post holidays

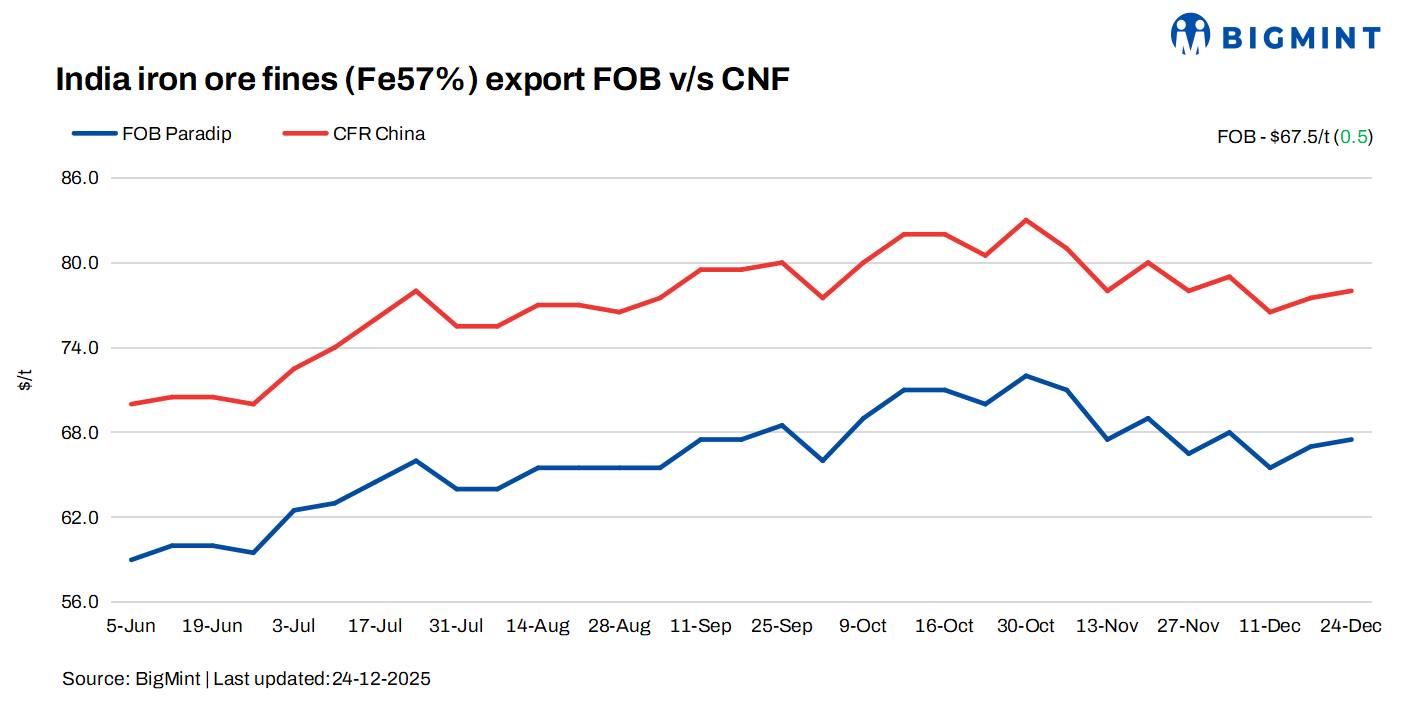

Indian iron ore fines export prices remained largely stable this week on 24 December; however, market activity stayed muted due to weak buying interest and relatively higher discounts for Indian-origin material. The ongoing Christmas holiday period significantly slowed trading activity, as many market participants were away from the seaborne market.

Prices, deals

BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export prices increased by $0.5/tonne (t) w-o-w to $67.5/t FOB east coast on Wednesday. Meanwhile, the index stood at $78/t CFR China.

As per sources, a miner sold multiple Fe 57% fines cargoes at 17.5-18% discount to the global benchmark fines index last weekend, which kept the market firm, but other traders failed to catch up with reasonable prices.

BigMint heard approximately 370,000 t of export deals during this assessment period, which were primarily concluded for below-Fe 55% fines at 25-26% discounts. Discounts now being offered are around 20-21% for Fe 57% fines cargo, while exporters are still targeting 19%, which is not attracting buyers toward fresh deals. While Fe56% cargoes were reported to fetch discounts in the range of 22-23%.

Market scenario

Exporters noted that buying interest was subdued throughout the week, with only limited inquiries received from overseas buyers. An exporter said, “We received a few buying inquiries, but counter bids were significantly lower than our expectations. We are currently holding back offers due to elevated sourcing costs, and plan to explore sales opportunities in the first week of January, once market participation improves.”

An international trader highlighted that demand for Indian iron ore cargoes in China continues to remain very weak. According to the trader, high port inventories in China, coupled with production restrictions at several Chinese steel mills, have dampened appetite for spot purchases. The trader added, “Chinese buyers are cautious, and preference for Indian cargoes is limited under the current market conditions.”

Another market participant stated that the market remained mostly silent during the week, with no aggressive bidding witnessed from buyers. Discounts for Indian iron ore fines were observed at higher levels, reflecting weak demand sentiment despite relatively stable headline prices. “Buyers are not willing to chase cargoes at current offer levels, especially amid ample port stocks in China,” a source told BigMint.

Market participants expect clearer price direction after the Christmas holiday period. Trading activity is likely to resume gradually after the New Year holidays, when buyers reassess their procurement strategies, and participants return to normal trading schedules.

Chinese spot prices firm w-o-w: The benchmark iron ore fines index rose $2/t w-o-w to $108/t CFR China on 17 December. Trading stayed muted on weak demand and ample non-mainstream Brazilian supply. The conclusion of some deals in Tangshan failed to lift sentiment, as lower pig iron output kept mill buying subdued. Although falling coke prices slightly boosted steel mills’ margins, iron ore prices remained range-bound.

DCE iron ore futures rise w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the Jan 2026 contract closed at RMB 777.5/t ($110/t) on 18 December, rising by RMB 10/t ($1/t) w-o-w.

Rationale

- Two (2) major deals for Fe 57% were recorded during this publishing window; not taken for price calculation. Therefore, T1 trade was given 0% weightage in the index calculation. A few deals were already factored into Monday’s assessment. For the detailed methodology, click here.

- BigMint received Twenty (20) indicative prices in the current publishing window, and eighteen (18) were considered for price calculation as T2 inputs and given 50% weightage.

Outlook

While prices have managed to stay firm, the near-term outlook remains cautious, with demand recovery dependent on post-holiday market participation and developments in Chinese steel production and inventory levels.

Leave a Reply