- Fe 57% fines discount widened to 22-23%

- Higher Chinese port stocks limit sea trades

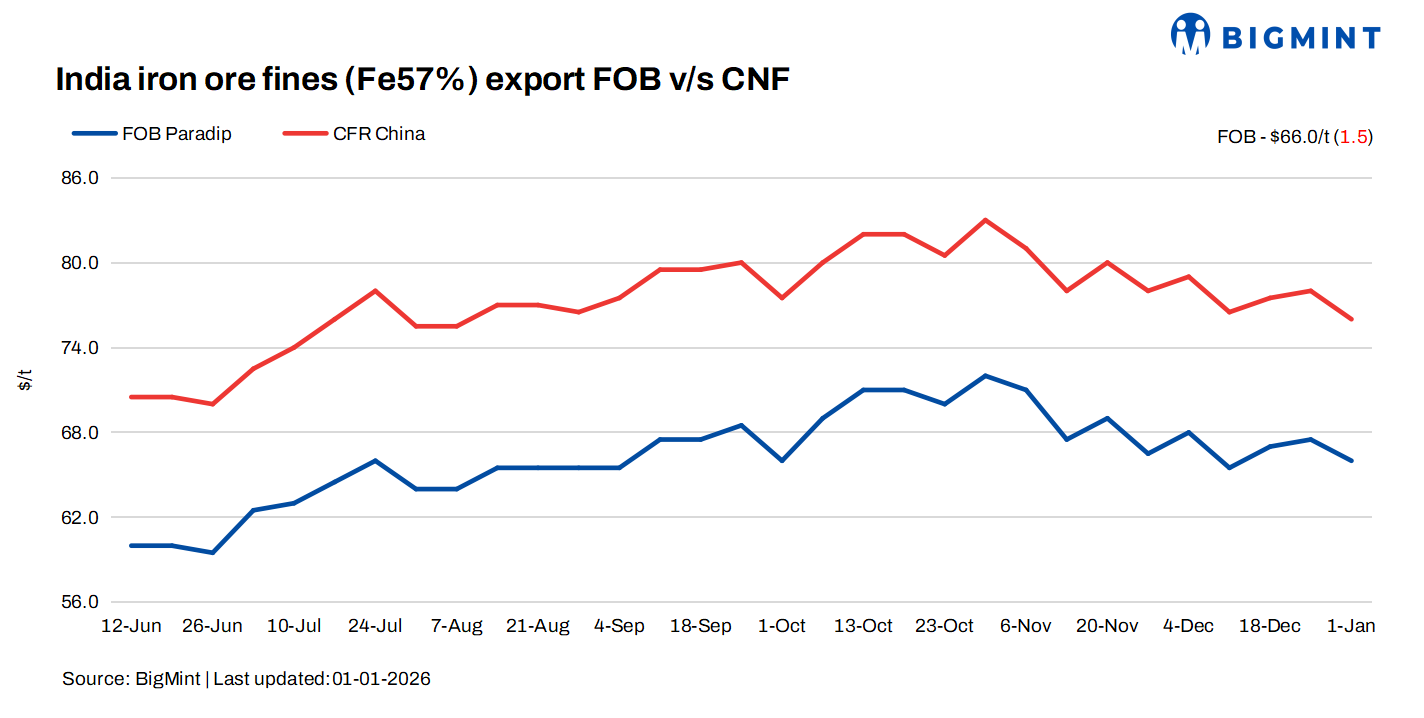

Indian iron ore export prices witnessed a decline of around $2/t this week on 1 January 2026, largely due to a widening discount in the seaborne market and muted buying interest from key consuming regions. Market sources said export activity remained subdued as buyers stayed on the sidelines amid the ongoing New Year holidays, with the Chinese market closed until 4 January.

Prices, deals

BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export prices decreased by $1.5/tonne (t) w-o-w to $66/t FOB east coast on Thursday. Meanwhile, the index stood at $76/t CFR China.

No export deals recorded this week amid the holidays and weakened market sentiments.

Market scenario

Market participants noted that Chinese mills had aggressively booked iron ore cargoes over the past month, leading to a sharp rise in port inventories across major Chinese ports.

An international trader said, “Chinese mills are well covered for the near term, and rising port stocks have reduced the buying interest for Indian fines. The current buying interest for Indian-origin material remains limited.”

The pressure on prices was further reflected in the widening discounts for low-grade material. According to market sources, the export discount for Fe 57% fines widened to around 22-23%, while Fe 54-55% material saw discounts increase to nearly 30% against the global fines index.

An exporter said, “Low-grade fines are facing intense competition in the seaborne market, especially with higher inventories and alternative supplies available.”

Meanwhile, exporters are facing a contrasting situation in the domestic market. Domestic prices for low-grade iron ore have been trending higher, prompting many exporters to hold back material in anticipation of improved export realizations. A market participant informed, “With domestic prices improving, exporters are not in a hurry to sell at lower export margins.”

Adding to the pressure, Australia-based miners increased the special lower-grade fines discount to 7.35% for January deliveries, narrowing from 8.5% in December, further weighing on seaborne low-grade prices. However, it is yet to be confirmed from official sources.

Recent reports indicate that inventories at Portside remain high, while the demand for finished steel products is moderate. Most Chinese mills are not operating at full capacity due to the ample stock at the ports and a lack of significant seasonal demand. However, there is an expectation of increased trading activity as the Chinese New Year approaches.

Market participants said they remain in a wait-and-watch mode, as several Indian cargoes are reportedly unsold at Chinese ports.

Chinese spot prices firm w-o-w: The benchmark iron ore fines index rose $1/t w-o-w to $109/t CFR China on 31 December. Market activity remained subdued amid thin liquidity and limited trades. Seaborne prices were rangebound during the year-end holidays. A sharp decline in buying interest was evident, as most mills had already completed procurement ahead of the holidays, leaving little scope for price movement later on.

DCE iron ore futures rise w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the May 2026 contract closed at RMB 789.5/t ($113/t) on 1 January 2026, rising by RMB 20/t ($3/t) w-o-w.

Pellet inventories at major Chinese ports stood at 150.55 mnt on 31 December, increasing by 1.75 mnt w-o-w, as per data published by SteelHome. With this, port inventories reached an over one-year high, last seen in mid-November 2024.

Rationale

- No major deals for Fe 57% were recorded during this publishing window; not taken for price calculation. Therefore, T1 trade was given 0% weightage in the index calculation. A few deals were already factored into Monday’s assessment. For the detailed methodology, click here.

- BigMint received fourteen (14) indicative prices in the current publishing window, and twelve (12) were considered for price calculation as T2 inputs and given 100% weightage.

Outlook

Iron ore export prices are expected to remain volatile and under pressure in the near term, amid widened global discounts and subdued demand from China.

Leave a Reply