- Liquidity weakens, and muted demand from China

- Discount for Fe 57% fines widened to 18-20%

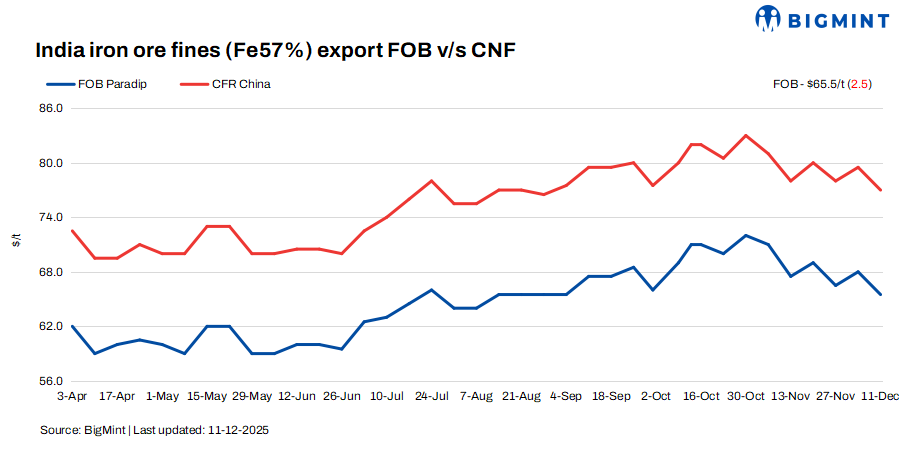

India’s iron ore export market witnessed a notable price correction in the week ended 11 December, with offers slipping by $ 3-4/t amid weak buying interest from Chinese mills and subdued liquidity in the seaborne market. Market participants indicated that a significant number of previously booked cargoes remain unsold in China, creating pressure on traders and adding to the bearish sentiment.

Prices, deals

BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export prices decreased by $2.5/tonne (t) w-o-w to $65.5/t FOB east coast on Thursday. Meanwhile, the index stood at $77/t CFR China.

BigMint heard approximately 575,000 t of export deals during this publishing period, were primarily concluded over the last weekend.

The discount is now floating in the market at around 18-20% for the Fe 57% fines cargo, while exporters are still targeting 17-18%, which is not attracting buyers for fresh deals.

Market scenario

“The market is flooded with unsold cargoes, and traders are struggling to clear out their cargo into China. Port inventory in China sharply hiked in the last two weeks, while mills are cutting production due to pollution control regulation. This overhang has weighed on fresh offers, with exporters facing poor responses and wider discounts compared to last week” an international trader told BigMint.

Even single-mine cargoes, which usually attract steady demand, failed to draw bids due to tight liquidity among buyers. “Liquidity has dried up, and buyers are negotiating aggressively. Even quality cargoes are not getting workable bids,” an exporter said.

Bids for mixed cargoes were largely heard around a 19% discount, while Fe 56-57% fines failed to receive bids above $ 75-76/t CFR China, keeping spot activity muted. However, market sources reported that a miner managed to sell Fe 57% fines at USD 79-79.5/t CFR China in today’s trading session – one of the few concluded deals in an otherwise dull market.

Last week, some exporters were able to conclude deals at a 20.5-21% discount for 56% Fe fines, but discounts have further widened this week as demand softens. Another source mentioned, “The gap between expectations and bids is increasing. Exporters are holding back cargo because domestic sourcing costs remain high.”

Chinese spot prices down w-o-w: The benchmark iron ore fines index fell $2/t w-o-w to $108/t CFR China on 10 December. The Asian seaborne iron ore market firmed up on improved macro sentiment, with a rebound driven by expectations of US Fed rate cuts and support from the upcoming year-end Politburo meeting. The domestic Chinese market saw the first coke price cuts, with trades focused on mid-grade fines.

DCE iron ore futures fall w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the Jan 2026 contract closed at RMB 757/t ($108/t) on 11 December, falling by RMB 37.5/t ($5/t) w-o-w.

Rationale

- Five (5) major deals for Fe 57% were recorded during this publishing window; two (2) were taken for price calculation. Therefore, T1 trade was given 50% weightage in the index calculation. A few deals were already factored into Monday’s assessment. For the detailed methodology, click here.

- BigMint received Twenty (20) indicative prices in the current publishing window, and seventeen (17) were considered for price calculation as T2 inputs and given 50% weightage.

Iron ore inventories at major Chinese ports were recorded at 142.8 mnt on 11 December, surging by 1.4 mnt w-o-w, as per data published by SteelHome.

Outlook

According to BigMint’s analysis, sentiment is turning increasingly bearish. Market participants expect export prices to remain under pressure, while the volume of reported deals is likely to stay limited in the coming week.

Leave a Reply