- Pre-monsoon restocking supports stable prices

- NMDC price cut to not affect offers, feel sellers

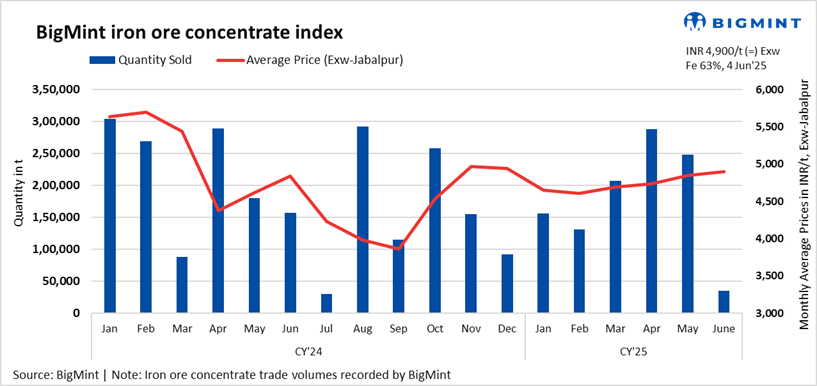

Iron ore concentrate (Fe 63%) prices in Jabalpur, India, remained stable in recently concluded deals compared to the previous assessment on 31 May 2025, with BigMint’s bi-weekly index for the same assessed at INR 4,900/tonne (t) ($57/t) exw Jabalpur.

Active restocking ahead of the monsoon, combined with stable pellet and Odisha iron ore price tags, provided some support to overall concentrate offers. However, weakening sponge iron and semi-finished steel tags, along with the recent announcement from the National Mineral Development Corporation (NMDC) of an iron ore price cut in June 2025, signal subdued market sentiment and are likely to exert downward pressure on concentrate offers.

Contrary to expectations, sellers remained hesitant towards a reduction in offers. A Jabalpur-based seller noted, “With pre-monsoon restocking likely to support prices, the recent NMDC price cut is not expected to have a significant impact on our offers.”

Echoing a similar view, another source remarked, “Although the NMDC price cut may affect overall market sentiment, the seasonal demand ahead of the monsoon is a key factor that will help counterbalance any potential downward pressure.”

Rationale

- Two (2) trades for 35,000 t were recorded in the publishing window. These were accorded 50% weightage.

- Eight (8) offers and indicative prices were reported, out of which seven (7) were taken into consideration as T2 trades, receiving the balance 50% weightage.

Factors supporting concentrate prices

- Pellet prices remain stable in recent trades: The pellet market in Raipur remained largely range-bound this week, marked by moderate trading activity and cautious buying sentiment. While a few plants managed to sell pellets in bulk to both local and outstation buyers at prevailing prices, the overall market remained subdued. This was primarily due to a sharp decline in sponge iron and billet prices, which exerted downward pressure on pellet demand. PELLEX, BigMint’s bi-weekly domestic pellet (Fe 63%) index for Raipur, remained stable at INR 9,250/t ($108/t) DAP Raipur on 3 June 2025 compared to the previous assessment on 30 May.

- Odisha iron ore market faces pressure, though prices stay firm: The iron ore market in Odisha continued to face downward pressure this week, as soft demand from the downstream steel sector weighed heavily on sentiment. With sponge iron and finished steel prices declining over the past two weeks, traders adopted a cautious approach. BigMint’s Odisha iron ore fines (Fe 62%) index remained stable w-o-w at INR 5,100/t ($60/t) ex-mines on 31 May.

Factors to watch out for

- NMDC cuts iron ore prices in Jun’25: India’s largest merchant iron ore mining company, NMDC, reduced its list prices of iron ore calibrated lump ore (CLO) and fines on 4 June 2025, BigMint learnt from sources. The miner fixed prices of DR-CLO (10-40 mm, Fe 67%) at INR 7,050/t ($82/t) and of iron ore fines (-10 mm, Fe 64%) at INR 5,350/t ($62/t), a decrease of INR 150-160/t ($2/t). Prices are on FOR basis from its Bacheli complex and include royalty, DMF, and NMET. Prices were reduced, as India’s steel prices hit a two-month low, domestic pellet tags dropped sharply, the Odisha Mining Corporation (OMC) iron ore fines auction fetched a weak response, and NMDC’s Chhattisgarh auction witnessed flat bids.

- Sponge PDRI prices drop INR 400/t w-o-w: Sponge PDRI prices in Raipur declined by INR 400/t ($5/t) w-o-w, driven by subdued market sentiment. Buyers remained cautious amid an uncertain market environment, leading to a drop in prices and limited transactions. Adequate bookings from the previous day prompted buyers to hold back on fresh commitments.

- Billet index drops w-o-w amid limited buying: Persistent weak market sentiment and cautious buying continued to pressure semi-finished steel prices. Despite lower offers, demand remained subdued, as most buyers chose to wait, leading to limited spot transactions and an ongoing downtrend. BigMint’s billet index dropped w-o-w by INR 400/t ($5/t) exw-Raipur on 4 June 2025.

Outlook

Market participants remain watchful for clearer pricing signals or signs of recovery in steel, iron ore, and pellet markets. While pre-monsoon restocking may continue to provide some support in the short term, persistently weak downstream sentiment poses a challenge to any meaningful price rebound.

Leave a Reply