- Buyers go slow on fresh procurements amid inventories

- OMC auction witnesses strong booking response

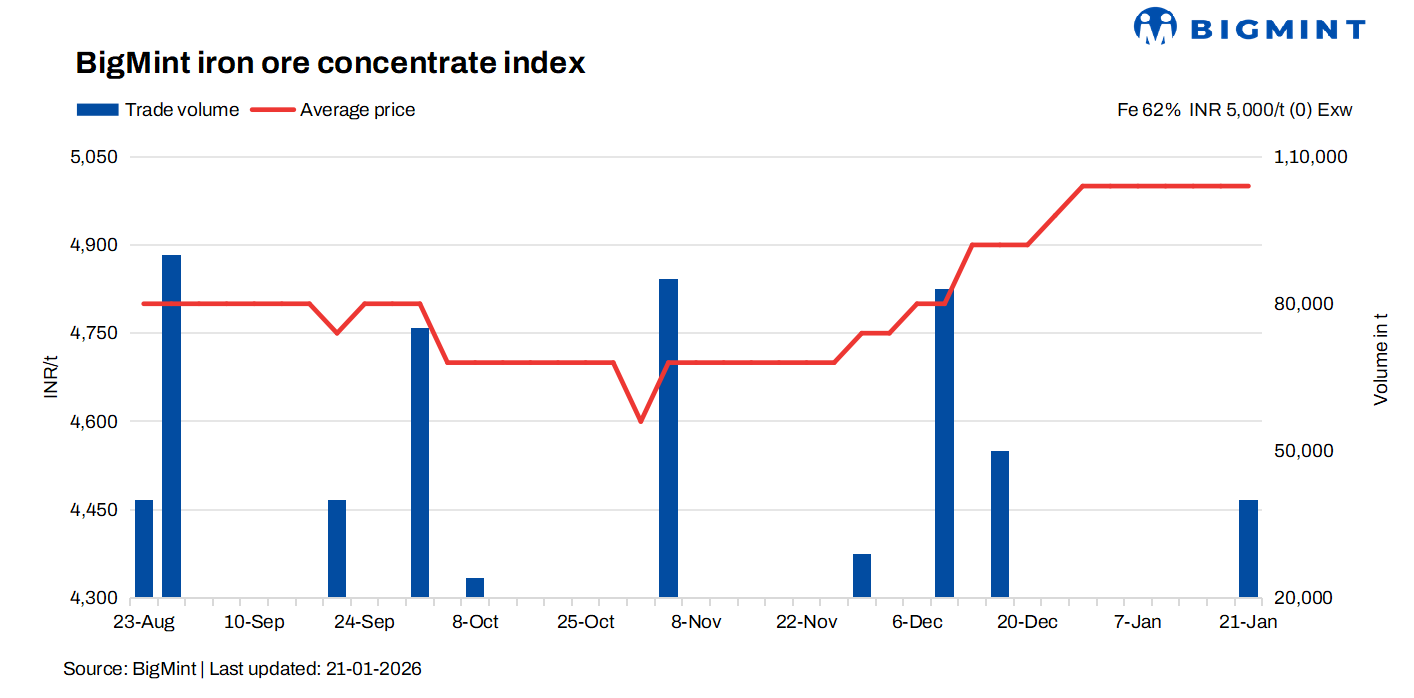

Domestic Fe 62% iron ore concentrate prices in Jabalpur were assessed unchanged at INR 5,000/t ($56/t) ex-works on 21 January, compared with 17 January, according to BigMint’s latest assessment. Similarly, Fe 63% concentrate prices remained steady at INR 5,300/t ($59/t) ex-works.

Prices continued to draw firm support from a persistent shortage of high-grade material, which kept market sentiment on the stronger side despite moderate buying activity. Transactions were concluded at prevailing price levels, reflecting continued demand for higher-grade material in the region.

An uptrend in finished steel prices offered indirect support to raw material prices; also the higher bids in OMC’s auction supported concentrate prices in the region. Market participants largely focused on executing previously committed orders, with dispatches and arrivals progressing as scheduled.

Sellers maintained their offers unchanged, citing broad market acceptance at current levels. A Jabalpur-based seller told BigMint that “the market is positioned at the higher end and price appreciation appears likely in the near term, though offers are being held steady as trades continue to clear smoothly at existing rates”.

Another seller noted that “the market remains driven by earlier order fulfilments, and any upward tilt in pellet prices could act as a trigger for a fresh rise in concentrate prices.”

On the demand side, a Jabalpur-based buyer said, “Procurement activity has slowed due to comfortable inventory levels, though expectations of a potential price increase persist.”

In OMC’s iron ore fines auction for 2.24 mnt (Fe 51-62%) on 19 Jan’26, around 2.03 mnt (91%) were booked at INR 2,450-6,200/t. The lots received premiums of INR 550-1,150/t over base prices, with INR 750/t being the average premium. Bids (weighted average) rose by INR 425/t m-o-m. Positive steel market sentiment, amid expectations of a pick-up in demand in Q4FY26, led to the robust auction response.

Rationale

- One (1) trade was recorded in this publishing window and, thus, this category was not taken into consideration, receiving a 50% weightage.

- Nine (9) offers and indicative prices were heard, and eight (8) were taken into consideration as T2 trades, receiving 50% weightage.

Factors supporting prices

- Odisha iron ore prices rise by INR 100/t wo-w: BigMint’s Odisha iron ore fines (Fe 62%) index rose by INR 100/t ($1/t) w-o-w to INR 5,900/t ($64/t) ex-mines on Saturday. Iron ore prices in Odisha recorded an increase of INR 100–200/t during the week ended 17 January, underpinned by a revision in base prices by the Odisha Mining Corporation (OMC). Market participants attributed the upward movement to improving sentiment in the downstream steel market, which strengthened over the past three to four days and encouraged buyers to re-enter the market, lending firm support to iron ore prices.

- Pellet prices remain stable in Raipur: PELLEX, BigMint’s bi-weekly domestic pellet (Fe 63%) index for Raipur, remained unchanged at INR 9,800/t ($108/t) DAP on Tuesday, in line with the previous assessment on 16 January. Pellet prices in Raipur held steady during the week, as assessed on 20 January 2026, with trading activity staying subdued amid weak buying interest from steelmakers. Market participants indicated that overall sentiment remains cautious, with buyers largely limiting procurement to need-based transactions rather than engaging in bulk purchases. The absence of aggressive demand continued to cap any upward movement in pellet prices, despite stability in other segments of the iron ore value chain.

Outlook

Iron ore concentrate prices are expected to remain supportive in the near term, driven by limited availability of high-grade material and improving demand from the finished steel segment, which is strengthening overall market fundamentals.

Leave a Reply