- Market participants stay inactive in festive season

- Production halted owing to adverse weather conditions

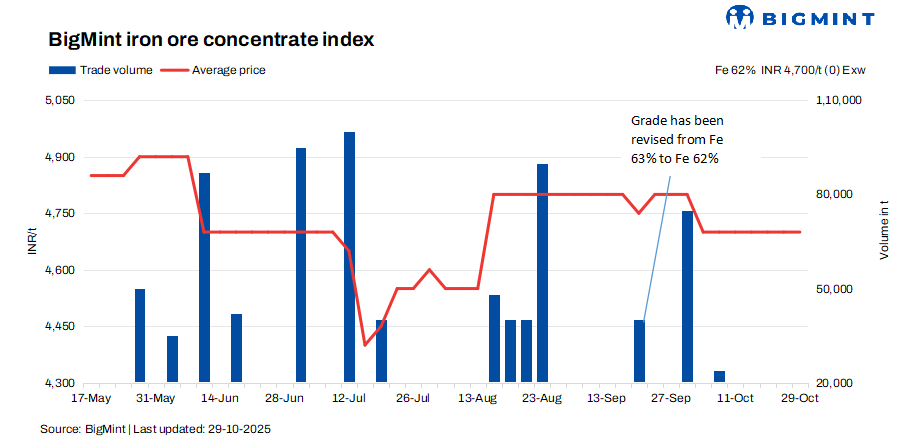

BigMint’s bi-weekly assessment for India’s iron ore concentrate (Fe 62%) stood firm at INR 4,700/tonne ($53/t) ex-works Jabalpur, unchanged from the previous evaluation on 25 October 2025. Despite this temporary stability, market participants anticipate a downward correction in the coming days as weak fundamentals continue to weigh on sentiment.

The overall market tone remains subdued, pressured by sluggish demand from the sponge iron and finished steel sectors. Additionally, NMDC’s iron ore price reduction for its November shipments has added to bearish expectations, likely exerting further pressure on concentrate prices across major producing regions.

A Jabalpur-based seller informed BigMint, “Production is yet to return to normal levels due to persistent weather-related disruptions and internal supply constraints. Operations are still running below capacity, and with weak demand, the market is likely to trend downward further.”

Echoing a similar sentiment, a local trader added, “Prices are currently holding steady, but a correction seems inevitable. Sellers are maintaining firm offers only because of pending orders, though overall sentiment remains bearish.”

Rationale

- No trade was recorded in this publishing window.

- Eight (8) offers and indicative prices were heard, and four (4) were taken into consideration as T2 trades, receiving 100% weightage.

Factors affecting iron ore concentrate prices

- Pellet prices fall by INR 100/t ($1/t) in Raipur: PELLEX, BigMint’s bi-weekly domestic pellet (Fe63%) index for Raipur, dipped by INR 100/t ($1/t) to 9,900/t ($112/t) DAP on 28 October 2025 compared to the previous assessment on 24 October. Pellet prices in Raipur have remained largely rangebound amid sluggish market activity, with buyers staying cautious due to weak demand and muted price movements in the sponge iron and semi-finished steel segments. Overall, market sentiment remains steady yet subdued, as participants await clearer demand signals from the downstream steel industry.

- Odisha iron ore prices stable w-o-w: BigMint’s Odisha iron ore fines (Fe 62%) index held firm at INR 5,300/tonne ($60/t) ex-mines on 25 October 2025, unchanged from the previous week. The stability follows the recent Odisha Mining Corporation (OMC) auction held on 17 October 2025, which saw active participation from major buyers. However, trading activity in the open market remained muted, as most steelmakers had already secured sufficient volumes during the OMC auction. As a result, fresh demand in the spot market stayed limited, with participants adopting a wait-and-watch approach amid steady price trends and cautious market sentiment.

Outlook

Iron ore concentrate prices are expected to soften further as weak demand from sponge iron and steel sectors, along with NMDC’s price cuts, weigh on market sentiment. Limited trade activity and cautious buying indicate a downward trend ahead. Overall, prices are likely to remain under pressure in the short term.

Leave a Reply