- Price cuts by miner seen as participation catalyst

- Steel sector softness caps aggressive buying

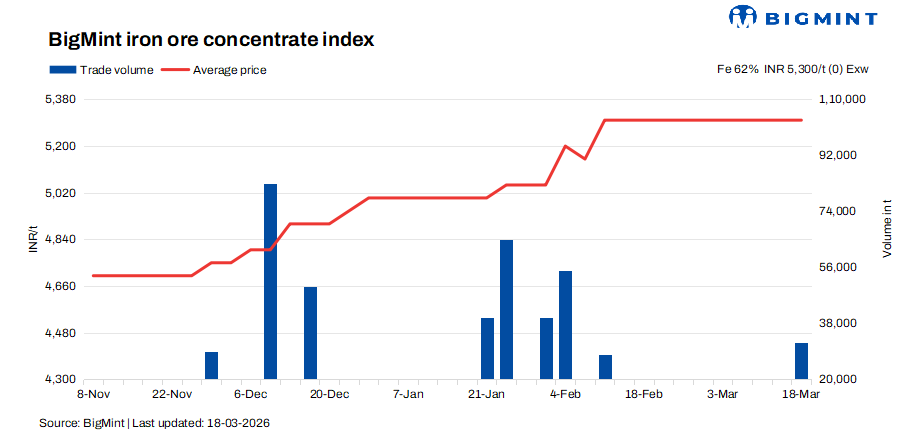

Iron ore concentrate prices in Jabalpur continued to exhibit notable resilience on 18 March 2026, holding firm amid a finely balanced demand-supply landscape and a clear absence of fresh selling pressure. As per BigMint’s latest bi-weekly assessment, Fe 62% concentrate prices remained unchanged at INR 5,300/t ($58/t) ex-works since 14 March, while higher-grade Fe 63% material was heard at around INR 5,600/t ($61/t) exw. This sustained firmness highlights the market’s ability to withstand broader uncertainty, supported by a strong underlying cost structure and controlled supply.

The stability in prices has been significantly reinforced by steady pellet rates in Raipur and largely stable iron ore prices in Odisha, both of which have established a solid cost floor for concentrate in the region. Despite cautious sentiment prevailing across the steel value chain, trading activity in Jabalpur remained selectively active, particularly for higher-grade material, where bulk deals indicated continued interest from quality-conscious buyers.

Supply-side constraints have further tightened the market. Many sellers are currently focused on fulfilling previously booked orders, resulting in limited availability of fresh material. This restricted supply has played a crucial role in sustaining price levels. A Jabalpur-based seller noted that “dispatches against earlier commitments are ongoing and may take another couple of weeks to complete, after which fresh offers will be introduced based on prevailing market conditions.”

Market attention is now firmly centered on the Odisha Mining Corporation (OMC) auction scheduled for 19 March 2026, where around 3.6 mnt of iron ore comprising 1.57 mnt of lumps and 2.04 mnt of fines will be offered. Although OMC has reduced base prices by INR 50-600/t for lumps and INR 250-300/t for fines on a m-o-m basis except a few lots, the move is expected to stimulate participation rather than a sign of weakening fundamentals. With ore availability tightening in Odisha’s merchant market due to fiscal year-end constraints and exhausted environmental clearances (EC’s), market participants widely expect aggressive bidding. Many believe that intensified competition could push realized prices higher, providing a clearer directional cue to the market post-auction.

However, the market is not without its concerns. A section of traders remains cautious, pointing to softening downstream steel prices and subdued end-user demand, which could eventually weigh on concentrate prices. This disconnect between stable raw material prices and weakening steel sector fundamentals introduces an element of uncertainty, suggesting that current price levels may face pressure if demand fails to revive.

Contrastingly, a more optimistic view persists among some sellers, who anticipate that increasing participation in the market will fuel competition and support prices in the near term. This divergence in market expectations underscores the current transitional phase, where both bullish and bearish factors are actively at play.

Rationale

- Two (2) trade was recorded in this publishing window, in which only one (1) is taken into consideration, receiving a 50% weightage.

- Eight (8) offers and indicative prices were heard, all are taken into consideration as T2 trades, receiving 50% weightage.

Factors supporting prices

- Pellet prices steady in Raipur: PELLEX, BigMint’s bi-weekly domestic pellet (Fe 63%) index for Raipur, held stable at INR 11,000/t ($119/t) DAP on 17 Mar against the last assessment on 13 Mar. Trading activity stayed limited as buyers remained cautious, while sellers maintained firm price resistance. The market continues to operate in a wait-and-watch mode, with no clear directional trend in the near term. Participants also highlighted that similar subdued conditions are prevailing in neighbouring markets, reflecting a broader cautious sentiment.

- Odisha iron ore prices remain largely stable: BigMint’s Odisha iron ore fines (Fe 62%) index declined by INR 50/t w-o-w to INR 5,750/t ($64/t) ex-mines on 14 March, despite moderate trading activity. Market sentiment remained slightly cautious, as steelmakers continued to show underlying demand but adopted a more measured buying approach, focusing on securing cost-effective raw materials amid prevailing uncertainty.

Outlook

Iron ore concentrate prices are expected to remain relatively firm in the near term, supported by expectations of strong bidding in the upcoming OMC auction and continued supply tightness.

Leave a Reply