- Logistical disruptions keep supply tight

- Sellers focus on clearing pending orders

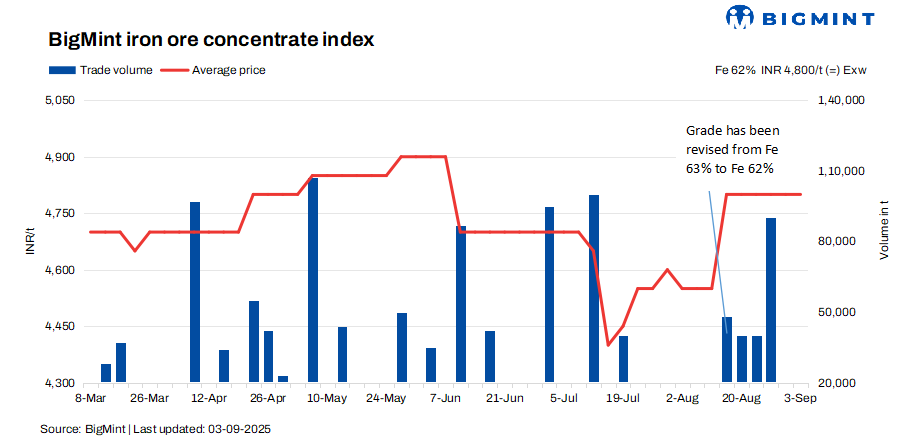

BigMint’s bi-weekly India iron ore concentrate index stood firm at INR 4,800/tonne (t) ($55/t) exw-Jabalpur, unchanged from the previous assessment on 30 August 2025. Fe 63% iron ore concentrate prices hovered at around INR 5,100/t ($58/t) exw, with some deals closed at these levels. However, most sellers prioritised clearing pending orders, limiting scope for fresh bookings and maintaining overall market stability.

Trading activity in Jabalpur, central India, remained subdued this week, as buyers held back from fresh purchases due to a backlog of pending orders. The combination of unfulfilled previous bookings and steady Odisha iron ore fines prices provided support to concentrate offers, keeping the market stable.

Railway movement restrictions remained a key concern, while poor road connectivity in major mining areas further disrupted the supply chain. Although demand was steady, these logistical challenges and supply-side constraints tightened material availability, leading to cautious buying in the market.

A Jabalpur-based seller highlighted, “Logistical restrictions have slowed down dispatches, while payment-related issues are also weighing on trading activity. Adding to the pressure, nearly 50% of previously booked orders are still pending due to weak supply flows. On the other hand, demand for material remains firm, creating a mismatch between supply and consumption needs.”

Rationale

- No trade was recorded in this publishing window.

- Ten (10) offers and indicative prices were heard, of which eight (8) were taken into consideration as T2 trades, receiving 100% weightage.

Factors affecting iron ore concentrate prices

- Odisha iron ore fines prices remain firm w-o-w: BigMint’s Odisha iron ore fines (Fe 62%) index remained stable w-o-w at INR 5,500/t ($62.5/t) ex-mines on 30 August 2025. The raw material market maintained its strength; however, the downstream steel sector witnessed sharp price corrections. In recent weeks, sponge iron and semi-finished steel prices have fallen significantly, prompting buyers to turn cautious about procuring iron ore at elevated levels. Still, selective need-based buying persisted, as steelmakers continued to secure material to meet immediate production requirements.

- Pellet prices inch down by INR 200/t ($2/t) in Raipur: Raipur-based pellet producers reduced their offers for Fe 63/63.5% (+/-0.5%) material by INR 200/t ($2/t) to INR 10,000-10,300/t ($113-117/t) exw recently. Continuous declines in sponge iron and semi-finished steel prices, along with weakened market dynamics, led to a reduction in pellet offers. Sponge iron (PDRI) prices fell by INR 1,200/t in the last two weeks to INR 23,200/t exw-Raipur.

Outlook

Iron ore concentrate prices are expected to remain stable in the near term, supported by pending orders and steady Odisha fines prices. Logistical constraints and subdued downstream steel demand may continue to restrict fresh buying, while the ongoing demand-supply imbalance is likely to provide additional support to prices.

Leave a Reply