- Buyers stick to workable price range

- OMC auction outcome to guide direction

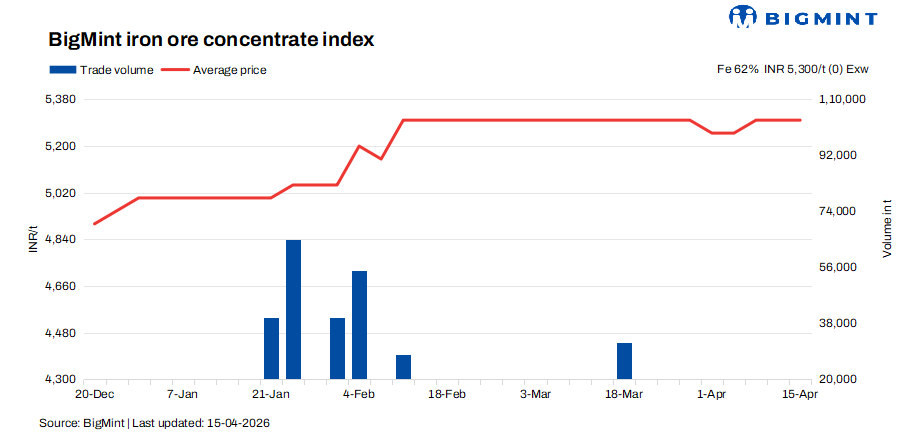

India’s iron ore concentrate market continued to exhibit a firm yet cautiously balanced tone this week, underpinned by steady seller offers and broadly stable market sentiment, even as underlying demand signals remained mixed.

As per BigMint’s latest bi-weekly assessment dated 15 April, Fe 62% concentrate prices held their ground at INR 5,300/t ($58/t) ex-works, unchanged from 11 April. Similarly, higher-grade Fe 63% material remained steady in the range of INR 5,600-5,700/t ($60-61/t) ex-works, reflecting persistent tightness in premium-grade availability. The shortage of high-grade material continues to act as a strong price anchor, with around 30,000 t of Fe 63% trades concluded within the same range, highlighting sustained buying interest despite broader caution.

Instead of aggressive price discovery, the market is currently being shaped by availability discipline and transactional selectivity. Sellers are not actively revising offers, largely because current levels are ensuring deal visibility, while buyers are confining their interest strictly within this workable band. The recent dip in pellet prices has not translated into any immediate correction in concentrates, suggesting a decoupled trend between the two segments.

A key feature this week has been the slow pace of deal finalization, driven less by disagreement and more by timing mismatches. Buyers continue to explore marginally lower levels, whereas sellers quoting above the market are finding limited engagement. This has resulted in elongated negotiations rather than outright deal rejections.

Operationally, the market is also navigating a heavy execution pipeline, with multiple previously concluded deals still pending dispatch. This backlog has temporarily reduced fresh spot exposure, as suppliers remain occupied with fulfilling earlier commitments.

Participants are also closely monitoring the outcome of OMC’s upcoming auction, which is expected to provide a clearer benchmark for near-term positioning. Until then, activity is likely to remain range-bound with limited triggers.

A Jabalpur-based seller highlighted the situation: A significant volume of old orders is still pending, reflecting a clear demand-supply gap. With over 30 rakes from the last financial year yet to be dispatched, our current focus is on clearing these commitments. Fresh offers will only be considered once these volumes are moved.”

Echoing a similar stance, another market participant noted: “Following an extended shutdown, we are currently focused on clearing old orders. Fresh offers will likely resume next month. While some sellers quoted higher prices, buyers have shown clear resistance, and enquiries continue to align with prevailing levels.”

Rationale

- Zero (0) trade was recorded in this publishing window receiving a 0% weightage.

- Ten (10) offers and indicative prices were heard, in which eight (8) are taken into consideration as T2 trades, receiving 100% weightage.

Factors might put pressure on concentrate prices

- Pellet prices fall by INR 300/t ($3/t): PELLEX, BigMint’s bi-weekly domestic pellet (Fe 63%) index for Raipur, declined by INR 300/t ($3/t) to INR 10,600/t ($114/t) DAP on Tuesday, compared to 10 April, indicating a cooling market trend. The drop comes after last week’s uptick, when producers had raised offers following higher iron ore prices announced by NMDC and Lloyds Metals for April supplies. However, the market was unable to sustain those levels, as buying interest remained weak, leading to a price correction.

- Odisha iron ore prices dip by INR 50/t ($0.5/t) w-o-w: BigMint’s Odisha iron ore fines (Fe 62%) index declined by INR 50/t ($0.5/t) w-o-w to INR 5,750/t ($62/t) ex-mines on Saturday (11 April), despite active trading in the market. The dip was largely driven by fresh offer announcements from Odisha-based miners, which exerted downward pressure on sentiment. Increased spot availability further encouraged miners to adjust prices and finalize bulk deals for April deliveries, leading to the overall correction.

Outlook

Iron ore concentrate prices are likely to remain muted in the near term, with limited upside momentum. Downward pressure may persist due to softening pellet prices and easing iron ore fines trends. However, restricted fresh supply and ongoing dispatch backlogs could prevent any sharp correction. Market direction will largely depend on OMC auction outcomes and improvement in buying activity.

Leave a Reply