- Buyers hold sufficient inventories, limiting fresh bookings

- Pellet market weakness and Odisha price correction weigh on sentiment

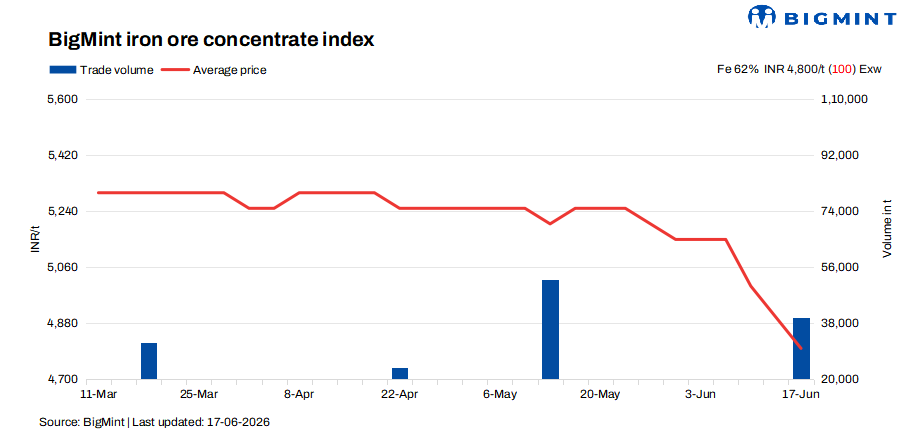

Iron ore concentrate prices continued to soften this week also, pressured by lower bids from buyers, limited trade activity, and weak sentiment across the broader iron ore and pellet markets. The ongoing correction in Odisha iron ore prices, coupled with subdued demand in the pellet segment, further weighed on concentrate prices, prompting a cautious approach from both buyers and sellers.

According to BigMint’s latest bi-weekly assessment, Fe 62% iron ore concentrate prices were assessed at INR 4,800/t ($51/t) ex-works, down by INR 100/t ($1/t) from the previous assessment on 13 June. Meanwhile, Fe 63% concentrate was heard at around INR 5,000-5,200/t ($53-55/t) ex-works. 40,000 t of high-grade concentrate transactions were concluded during the assessment period, indicating selective buying interest for premium-grade material.

The market remained largely inactive as a significant bid-offer gap continued to restrict trade. While buyers aggressively sought discounts amid weakening downstream demand, sellers largely resisted major price reductions, resulting in prolonged negotiations and delayed transactions. Several suppliers refrained from revising their offers, citing pending order commitments and production constraints, while others temporarily withdrew from the market. A few sellers, however, were compelled to lower their offer levels in line with deteriorating market fundamentals.

Market sentiment was further dampened by expectations surrounding the upcoming Odisha Mining Corporation (OMC) iron ore auction scheduled for 19 June. Industry participants are closely monitoring the base prices to be announced, with many anticipating either stable or lower levels considering the current weakness in raw material and finished steel markets. The lack of support from finished steel prices has significantly reduced confidence across the raw material value chain, limiting buyers’ willingness to replenish inventories.

Trading activity remained muted as both sides maintained a firm stance. Buyers were unwilling to procure material at prevailing offer levels, citing sufficient inventory positions and uncertain market prospects. Sellers, on the other hand, remained reluctant to accept significantly lower prices, unwilling to compromise margins amid rising operational pressures.

Adding to the pressure, concentrate producers are facing growing inventory concerns ahead of the monsoon season. The need to liquidate stock before rains disrupt logistics and production activities has increased selling pressure across several regions. However, this urgency has not translated into stronger buying interest, as consumers continue to adopt a wait-and-watch approach.

A Jabalpur-based concentrate supplier told BigMint that “We are finding it difficult to conclude deals as buyers are seeking steeper discounts. The current market imbalance has been exacerbated by OMC’s pricing strategy. Independent suppliers like us are struggling to compete as buyers continuously compare material prices across different sources. While NMDC is moving prices upward, OMC’s lower pricing is dragging market sentiment down, making it increasingly challenging to justify our offers. Buyers are naturally choosing whichever source offers the greatest advantage, creating significant pressure on standalone suppliers.”

Meanwhile, a major buyer stated “We are currently not making fresh purchases as we have sufficient inventory to meet our near-term requirements.”

Rationale

- Two (2) trade was recorded in this publishing window, in which one (1) deal is taken into consideration, receiving a 50% weightage.

- Eight (8) offers and indicative prices were heard, and five (5) were taken into consideration as T2 trades, receiving 50% weightage.

Factors affecting prices

- PELLEX declines by INR 300/t ($3/t) w-o-w: PELLEX, BigMint’s bi-weekly domestic pellet (Fe 63%) index for Raipur, declined by INR 300/t to INR 9,300/t ($98/t) DAP on 16 June from 12 June, while Raipur-based producers simultaneously lowered offers for Fe 62.5/63% pellets by INR 300/t ($3/t) to INR 9,100-9,200/t ($96-97/t) ex-works on 13 June, the correction was driven by weak buying interest, constrained liquidity, and elevated inventories at pellet plants, with steelmakers adopting cautious procurement strategies and restricting purchases to immediate operational needs, leaving bulk booking activity largely absent and forcing sellers to reduce prices to stimulate demand.

- Odisha iron ore prices fall by INR 150/t($1.5/t) w-o-w: BigMint’s Odisha iron ore fines (Fe 62%) index declined by INR 150/t w-o-w to INR 4,950/t ($52/t) ex-mines on 13 June 2026. Iron ore prices across Odisha fell by INR 100-200/t over the past week, as weak demand from steelmakers and continued softness in finished steel prices weighed on market sentiment. The correction highlights mounting pressure on raw material consumption, with buyers maintaining a cautious stance amid subdued steel sector fundamentals and limited procurement activity.

Outlook

Iron ore concentrate prices in central India are expected to remain under pressure in the near term amid subdued demand from pellet makers and steel producers, elevated inventories, and cautious market sentiment. Market participants are closely monitoring the outcome of OMC’s auction on 19 June, as the bidding response is likely to provide further direction to the market. However, sellers may look to liquidate inventories ahead of the monsoon season over the coming weeks.

Leave a Reply