- Coal prices rise amid supply disruptions

- Rising power plant stocks may restrict further price gains

Portside prices of Indonesian thermal coal in India strengthened w-o-w in the week ending 14 November 2025 buoyed by firmer global benchmarks and a revival in Chinese procurement.

Traders reported a steady pickup in domestic buying interest as international indices gained momentum and Chinese import demand improved ahead of the winter heating season.

BigMint’s assessments show a broad-based upward movement across key grades. 5000 GAR grade increased by INR 50/t reaching INR 7,200/t at Kandla and INR 7,100/t at Vizag, while 4200 GAR rose by INR 50/t to INR 5,850/t at Kandla and INR 5,750/t at Vizag. 3400 GAR coal prices saw the strongest uptick, rising INR 100/t to INR 4,550/t at Navlakhi. The firming up of prices owed to higher seaborne values and selective restocking by traders positioning for stronger Q4 demand.

Chinese buying resurgence boosts sentiment

Sentiment across Asian markets improved as Chinese spot buying strengthened following a partial relaxation of import controls and reduced domestic output. Coastal utilities actively sought winter cargoes, reinforcing a broader shift towards firmer demand expectations. Indian portside markets closely tracked this resurgence, with buyers showing renewed willingness to procure after several weeks of resistance.

Freight market ticks up

Supramax freight rates on the Indonesia (East Kalimantan)-India (Navlakhi) route continued their upward momentum. Rates increased by approximately $1/dmt w-o-w to $14.72/dmt. This sustained rise was primarily attributed to improved activity in the Pacific basin, where an uptick in fixtures tightened vessel availability and strengthened market sentiment, thereby supporting higher freight levels on the route.

Portside inventories dip on lower arrivals

India’s portside thermal coal inventories eased 3.2% w-o-w to 12.57 mnt in week 45, reflecting reduced vessel arrivals and conservative procurement by buyers, particularly along the west coast. Although select eastern ports recovered following recent cyclone-related disruptions, overall inventory levels suggest cautious stocking behaviour despite improving market sentiment.

Power plant stocks improve, variations persist

Coal stocks at Indian power plants increased to 51.56 mnt as of 13 November, up from 49.03 mnt a week earlier, offering around 17 days of consumption cover. This indicates a comfortable national supply position heading into winter.

Despite the overall improvement, 15 power plants remain under critical stock conditions – seven dependent on domestic coal, six on imported coal, and two using washery rejects. Localised shortages persist due to logistical constraints, uneven mine dispatches, and regional distribution gaps. Strengthening supply chain efficiency will be essential as seasonal demand rises.

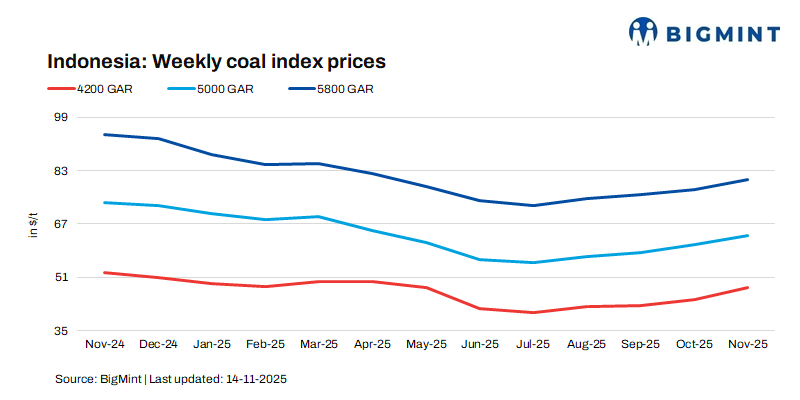

Seaborne prices edge up

Indonesian seaborne coal prices registered modest gains during the week, supported by firmer Chinese tender activity and emerging supply constraints stemming from rainfall in Kalimantan. 5800 GAR prices increased by $0.60/t to $80.45/t, while the 4200 GAR grade rose by $1.63/t to $48.40/t. The 3400 GAR grade also edged higher by $0.41/t to $32.63/t.

Weather-related disruptions have begun affecting mine output and loading operations, leading to expectations of tighter export availability through November. Sustained buying interest from South Asian markets further contributed to the upward momentum in prices.

Outlook

Indonesian coal prices are expected to remain firm on stronger Chinese demand and weather-related supply tightness. Indian portside prices may see limited gains, while freight rates are likely to stay elevated. The short-term market outlook remains positive.

Leave a Reply