- ADC12 imports plunge 57% y-o-y in 9MCY’25

- PV retail sales rise 5% y-o-y in 9MCY’25

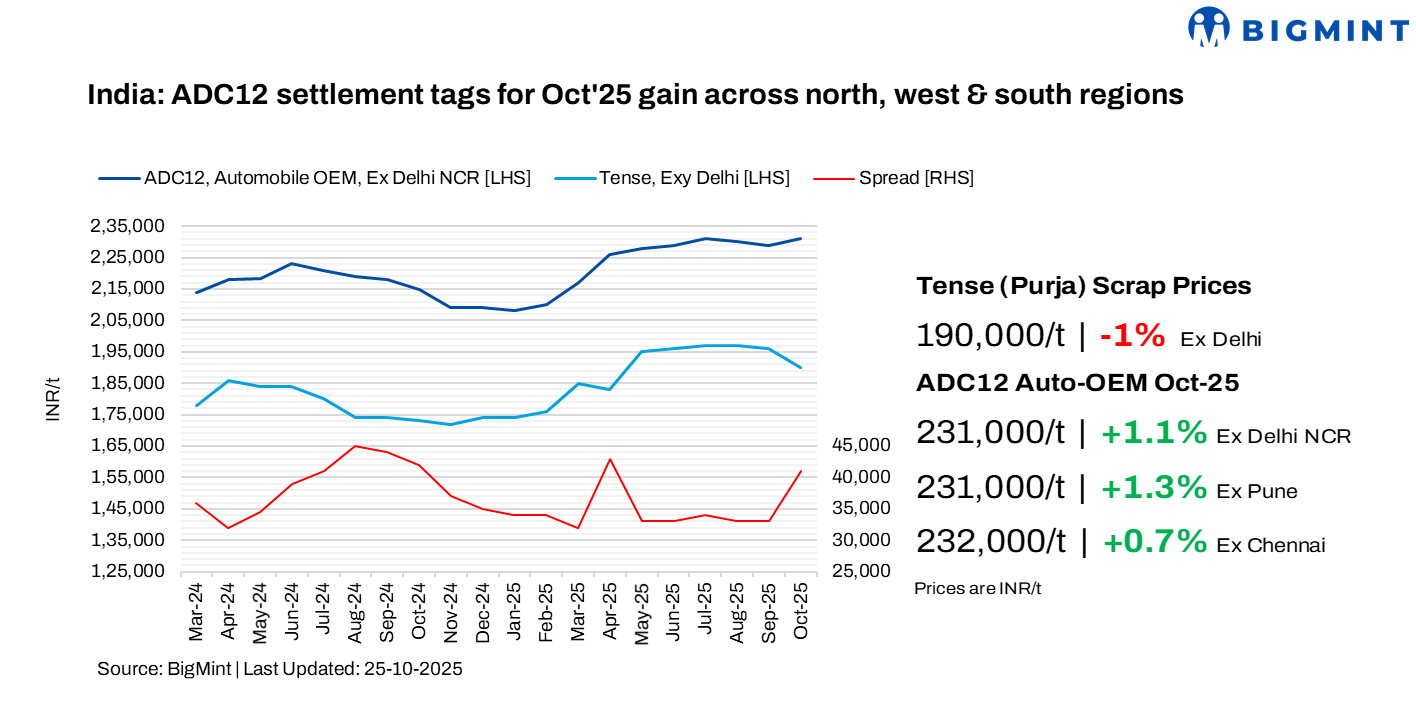

India’s aluminium ADC12 market rebounded in October 2025 after a modest decline in September, with prices supported by rising automotive sector demand following GST cuts. While global scrap prices surged on higher LME levels, domestic tags corrected due to improved availability.

According to BigMint, average OEM ADC12 prices for October increased m-o-m, reaching INR 231,000/t in Delhi and Pune, up by INR 2,500/t and INR 3,000/t respectively, and INR 232,000/t in Chennai, up by INR 1,500/t. The scrap-to-semi-finished spread widened to INR 39,000-43,000/t, reflecting higher ADC12 costs amid declining domestic scrap prices.

Additionally, a leading Indian automaker has increased its ADC12 settlement price by INR 2,900/t m-o-m to INR 231,800/t for November 2025. The price hike was primarily driven by a surge in auto demand following the recent GST reduction, which has pushed vehicle sales to record highs. Meanwhile, the scrap-to-ADC12 spread widened to INR 39,000-40,000/t in late October 2025.

Market dynamics in early Nov’25

As per the market participants across the northern, western, and southern regions indicates that supplier offer prices for ADC12 in late October and early November ranged between INR 233,000-234,000/t, while OEMs are negotiating slightly lower for November settlements, around INR 230,000-232,000/t on standard 30-day payment terms.

According to BigMint’s bi-monthly ADC12 assessments, regional prices were initially lower during the first week of October but began rising following the release of September automobile sales figures and growing optimism for the coming months.

Raw material trends

In October, imported aluminium scrap prices rose, driven by LME aluminium hitting a 3-year high of $2,800/t in late October due to supply concerns, marking a 5% m-o-m gain. In contrast, domestic aluminium scrap prices, particularly of the casting grade used for ADC12 production, declined as availability improved with higher import levels.

Notably, tense scrap prices in Chennai fell below Delhi levels in mid-October, reflecting better domestic supply in the south and strict GST compliance. Scrap demand also softened during October due to Diwali festivities, with auto companies clearing existing inventories before booking fresh raw material. However, market participants expect scrap demand to rebound alongside rising ADC12 consumption.

Among key imported grades, US-origin Tense rose by $15/t m-o-m to $2,000/t, while UK-origin Wheels increased by $32/t to $2,610/t. On the domestic front, Tense scrap prices fell by INR 3,500/t in Delhi and INR 8,000/t in Chennai, with BigMint’s October averages at INR 191,500/t in Delhi and INR 189,000/t in Chennai.

Meanwhile, Chinese silicon 553 prices remained stable at $1,370/t CFR Mundra amid steady demand.

Tracking India’s scrap, ingot import flow in 9MCY’25

India’s aluminium scrap imports have witnessed an incremental shift in terms of grade-wise sourcing. In January-September 2025 (9MCY’25), for the first time in the past three years, Taint Tabor scrap imports surpassed Zorba arrivals to become the most-imported grade into India. Imports of Taint Tabor stood at 0.32 mnt in 9MCY’25, an 15% increase from 0.28 mnt in 9MCY’24.

The US continued as the leading supplier, exporting 289,066 t to India reflecting an 9% decrease from 9MCY’24 primarily due to the strong domestic demand for scrap and tariff related uncertainty in the US.

ADC12 imports

India’s ADC12 alloy market witnessed a dramatic contraction in imports during nine months of 2025 (9MCY’25), with inbound volumes plunging by 57% y-o-y. Total ADC12 imports stood at just 8,457 t, down sharply from 19,584 t in 9MCY’24.

Auto sector performance

Passenger vehicle (PV) sales in India dipped 10.4% m-o-m to 0.29 million units in September 2025, down from 0.32 million units in August. However, PV retail sales for 9MCY’25 rose 5% y-o-y to 3.02 million units from 2.87 million units in 9MCY’24.

Overall automobile sales for 9MCY’25 reached 18.57 million units, up 2% from 18.12 million units in 9MCY’24, according to FADA retail data.

The first three weeks of September were subdued as buyers awaited the new GST regime. Sentiment turned sharply in the final week, as Navratri festivities coincided with GST cuts, triggering a strong consumer response across segments.

“September 2025 was a unique month for India’s automobile retail industry. While the initial weeks were muted, festive cheer and GST 2.0 reforms boosted demand, resulting in a 5.22% y-o-y growth,” said FADA Vice President Sai Giridhar.

Outlook

ADC12 prices for November in northern, western, and southern India are expected to remain firm, supported by strong automobile demand post GST cuts and the upcoming wedding season. A price correction appears unlikely. Additionally, November price hikes by a major automaker are likely to provide further support to ADC12 prices.

Leave a Reply