- Global sentiment remains firm on higher coke, coking coal prices

- Domestic sentiment cautious amid adequate supply, weak demand

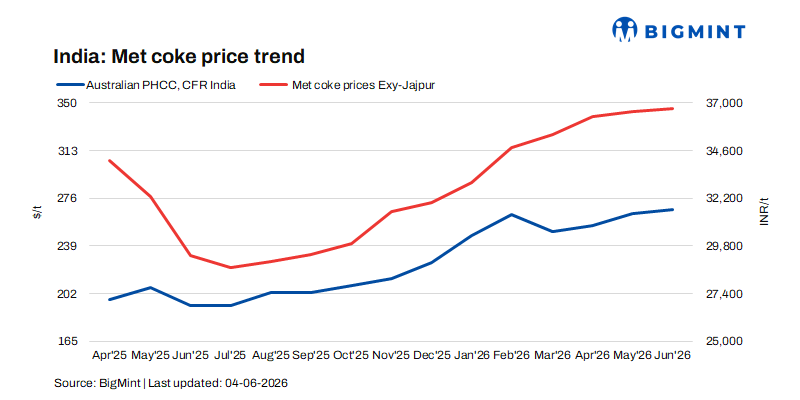

The metallurgical coke market witnessed an improvement in sentiment during the week ended 04 June 2026, primarily supported by strengthening international coke prices and firm upstream raw material costs. BigMint’s assessment of Indonesian-origin BF-grade coke (65/63 CSR) increased by $4/t w-o-w to around $313/t CFR India.

The upward movement was largely driven by firmer FOB offers from Indonesian suppliers, rising freight costs, and improving sentiment across the global coking coal and coke value chain. Additionally, sustained strength in China’s coke and coking coal markets contributed to higher replacement costs for international coke suppliers, lending further support to export quotations.

“Suppliers are currently holding back cargoes. Until last week, 65 CSR coke was being offered at around $288-290/t FOB. However, coke producers are attempting to push prices higher amid a sharp rise in coking coal prices, coupled with supply concerns following the recent accident in China and delays in Australian coal shipments. As a result, FOB coke prices could potentially rise to around $300/t by next week,” stated a trader.

India’s domestic coke market remains stable despite global price gains

In contrast to the international market, India’s domestic BF-grade metallurgical coke market remained largely stable during the week. Adequate material availability, balanced supply-demand dynamics, and comfortable inventory levels across key steel-producing regions prevented any significant upward movement in domestic prices despite higher import parity costs.

In the eastern region, BF-grade coke prices remained unchanged at INR 36,700/t ex-Jajpur. Meanwhile, prices in western India increased marginally by INR 500/t to INR 34,000/t ex-Gandhidham, supported by localised demand and replacement cost considerations. Foundry-grade (+90 mm) coke prices also remained stable at INR 36,400/t ex-Rajkot, reflecting steady demand from the foundry sector and sufficient market availability.

Anti-dumping duty remains a key market focus

Market participants continue to closely monitor the anti-dumping duty (ADD) on imported metallurgical coke, which is scheduled to expire at the end of June 2026. Industry stakeholders widely expect an extension of the duty, citing concerns that unrestricted imports could adversely impact domestic coke producers.

According to market participants, the continuation of the duty is considered critical for protecting domestic manufacturing capacity, preserving employment within the coke industry, and preventing a sharp increase in import dependence. An extension would also align with the government’s broader objective of supporting domestic industries and managing external trade balances.

Coking coal market continues to provide cost support

The global coking coal market remained firm during the week, providing sustained cost support to coke producers. Australian premium hard coking coal (PHCC) prices increased by $1/t w-o-w to $242/t FOB Australia as of 04 June 2026.

In China, the coke market maintained its upward momentum, with the fifth round of coke price increases, amounting to RMB 50-55/t ($7-8/t), fully implemented. Tight coking coal availability, slow supply recovery in Shanxi, and robust demand from steelmakers continued to support prices. Simultaneously, coking coal prices increased by RMB 20-80/t ($3-12/t), driven by active procurement from downstream consumers. Expectations of a potential sixth round of coke price hikes further strengthened overall market sentiment and reinforced cost support across the global coke supply chain.

Pig iron market signals cautious downstream demand

Despite stable steel production, downstream purchasing activity in the pig iron market showed signs of caution. Steel-grade pig iron prices in Durgapur declined marginally by INR 100/t w-o-w to INR 38,000/t ex-works, indicating moderate buying interest from steelmakers.

Recent auction results from NMDC Steel’s Nagarnar plant further reflected the cautious market environment. On 2 June 2026, the company successfully sold the entire offered volume of 12,000 t of steel-grade pig iron at a base price of INR 36,000/t ex-works. However, the auction clearing price was INR 500/t lower than the previous auction held on 29 May 2026. The lower bids suggest that consumers leveraged the price correction to replenish inventories while remaining cautious about near-term steel demand prospects.

Outlook

The Indian metallurgical coke market is expected to remain stable-to-firm in the near term. Continued strength in international coke and coking coal prices, along with elevated replacement costs, is likely to provide underlying support to domestic coke prices. Furthermore, expectations surrounding the extension of the anti-dumping duty could help sustain domestic producer confidence and limit import pressure.

However, the pace of domestic price increases may remain constrained by comfortable inventories, adequate supply availability, and cautious downstream buying sentiment in the pig iron and steel sectors. Market direction over the coming weeks will largely depend on developments in China’s coke market, coking coal price trends, domestic steel demand, and the government’s decision regarding the anti-dumping duty extension.

Overall, the market outlook remains cautiously bullish, supported by firm raw material costs and positive international sentiment, although weak downstream purchasing activity may limit aggressive price gains in the short term.

Leave a Reply