- India’s copper scrap market turns cautious ahead of festival

- Global refined copper production rises in H1CY’25

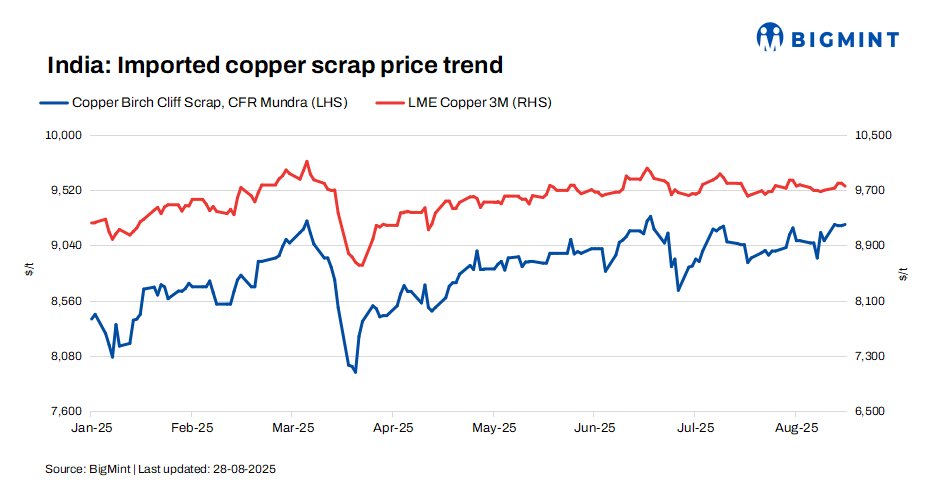

Imported copper scrap prices in India remained largely stable w-o-w, following a largely stable w-o-w LME copper futures at $9,755/tonne w-o-w.

According to BigMint’s assessment, copper Birch cliff scrap was assessed at $9,220/t, while US motors mix stood at $1,170/t (both CFR Mundra), both largely stable w-o-w.

LME futures slightly increased by $80/t to $9,755/t compared with last week’s $9,675/t. Meanwhile, copper stocks at LME-registered warehouses stood at 156,100t, slightly down by 250 t compared to 156,350 t the previous week.

Meanwhile, copper prices touched a two-week high as political tensions in the US boosted expectations of near-term rate cuts and weakened the dollar, making metals more attractive for non-US buyers.

A buying surge in New York offset earlier selling pressure from China. Supply risks also lent support, with Chile’s regulator tightening safety requirements at Codelco’s El Teniente mine after a deadly collapse, prompting the producer to cut its annual output forecast.

Market updates

India’s copper scrap market is witnessing a slowdown as the festive season approaches, with trading activity turning cautious. At the same time, global cues remain uncertain, as US government policies continue to play a significant role in influencing market sentiment and pricing trends.

In India’s non-ferrous metals markets, BigMint assessed domestic copper armature scrap at INR 794,000/t ex-Delhi, up by INR 6,000/t d-o-d.

Secondary continuously cast rods (CCRs) (99.90%) were assessed at INR 858,000/t ex-Delhi, up by INR 6,000/t w-o-w. Meanwhile, primary CCR prices stood at INR 900,000/t, up by INR 4,000/t w-o-w.

Demand from infrastructure, power, and manufacturing sectors continues to support prices, driven by ongoing projects and electrification initiatives. Supply tightness and minor logistical delays have kept bids firm, maintaining a positive market sentiment.

Price Levels (CIF China)

- Mill Berry (US/EU origin): 98.5% LME

- Candy Berry (EU origin): 97.3% LME

- Birch/Cliff (EU origin): 94.5% LME

In India, Mill Berry is commanding a premium, driven by robust domestic demand and limited supply.

However, near-term buying momentum has eased as participants adopt a cautious, wait-and-watch stance, influenced by both domestic dynamics and global price trends. In the imported scrap segment, trading volumes remained stable, though buyers stayed highly selective amid moderate swings in global copper prices and persistent currency volatility.

Overall, while underlying fundamentals remain supportive, the domestic market is showing signs of cooling, with participants closely tracking macro and currency developments before committing to fresh bookings.

Other market updates

India’s copper scrap imports surge while cathode inflows shrink

India’s copper scrap imports jumped 36% y-o-y to 229,548 t in 7MCY’25, supported by strong demand, zero duty, and easier norms, pushing the country’s share to 15% of Asia’s scrap trade. In contrast, copper cathode imports slumped 24% y-o-y to 131,486 t, hit by the BIS Quality Control Order, which curbed inflows and forced many wire and cable makers to shift towards scrap-based feedstock.

Copper market supported by Chinese demand, supply tightness

Copper prices held above $9,800/t as optimism grew from China’s RMB 200 billion ($27 bn) infrastructure package and an 8% y-o-y rise in July refined copper imports to 503,000 t. Supply constraints deepened with Asian spot TC/RCs falling below $50/t amid lower Chilean and Peruvian output, while supportive macro signals from the US and EU further underpinned sentiment. Analysts see prices stable in the $9,700–9,900/t range, with potential upside if inventories continue to decline.

Global refined copper output rises 3.6% in H1CY’25

Global refined copper production grew 3.6% y-o-y in H1CY’25, led by a 6% rise in China and 6.5% in the DRC, while Chile’s output fell 8.4% on smelter issues, ICSG data showed. Mine output increased 2.7% y-o-y, supported by Peru, DRC, Mongolia, and Chile, though Indonesia slumped 36% on Grasberg maintenance. Apparent refined usage rose 4.8% globally, with China’s demand up 7.5% and accounting for nearly 58% of world consumption.

Leave a Reply