- Global offers stable, Indian buying muted

- Domestic copper scrap firms up as demand improves

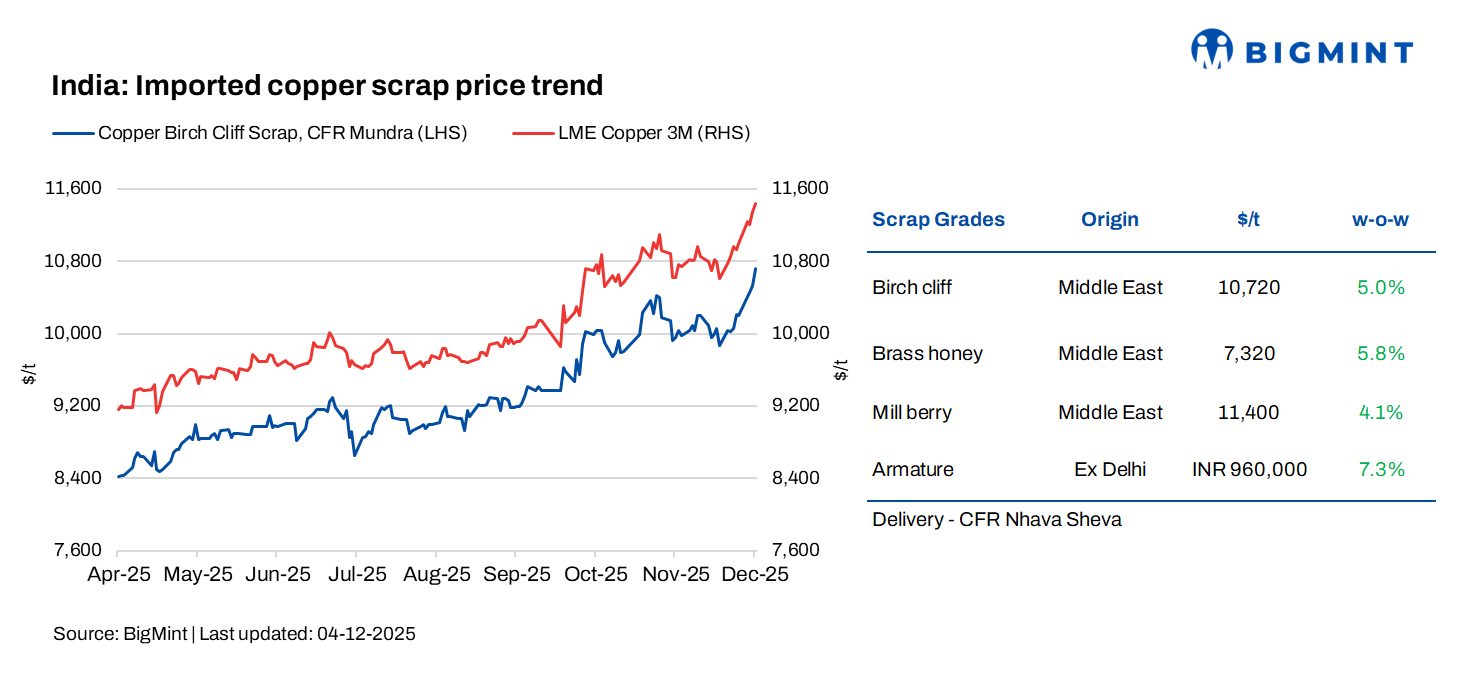

Imported copper scrap prices in India moved higher w-o-w on 4 December, supported by positive momentum in LME futures. Domestic scrap prices also firmed as market sentiment stabilised, and activity recovered from the post-festive slowdown. Buying remained cautious, however, with LME’s brief move toward the $11,500/t mark tempering aggressive restocking.

According to BigMint’s assessment, Birch/Cliff was assessed at $10,720/t, up 5% w-o-w, while US motors mix stood at $1,265/t (both CFR Mundra), up 1.2% w-o-w.

LME copper prices strengthen

LME copper prices climbed to $11,425/t on 4 December, up 4.3% from $10,950/t in the previous week, reflecting continued strength in the broader base metals complex. Copper inventories in LME-registered warehouses also increased, rising by 5,650 t to 162,150 t compared with 156,500 t a week earlier, signalling a moderate build in visible stocks despite firm pricing.

Copper surged past $11,500/t on the LME to a new record as tariff fears, heavy US-bound stockpiling and sharp warehouse withdrawals tightened global supply. A spike in LME Asian depot withdrawals triggered panic buying, while proposed US tariffs for 2027 created an unprecedented arbitrage that is pulling metal out of global pools and driving up EU and Asian premiums. With fund-driven momentum, collapsing visible inventories, structural mine outages and a widening US-LME price gap, the market has shifted into a two-world structure — surplus inside the US but deficit everywhere else.

Chinese and Russian-origin copper in LME stocks cannot enter the US, further tightening supply in Asia and Europe. Overall, copper prices continue to move deeper into uncharted territory as structural tightness, regional imbalances and strong financial flows shape the market.

Market insight

Imported copper scrap prices have remained largely unmoved despite LME copper briefly surpassing $11,500/t, as overseas suppliers opted to keep offers stable in view of muted Indian buying interest. Market participants noted that the recent rally appears more speculative than fundamentally driven, limiting the pass-through to imported scrap.

The surge in LME copper has been attributed to fund-driven buying, expectations of tighter mine supply, improving macro sentiment, and Chinese restocking ahead of Q1. Speculative flows and algorithmic trading intensified the move, pushing futures sharply higher even as physical demand remains mixed — explaining why imported scrap prices have not reacted to the exchange-led rally.

Price levels (CIF China)

- Brass Honey (EU, 6-7% impurity): 58% of LME

- Birch/Cliff (EU): 93% of LME

- UAE Birch/Cliff: 93.5-94% of LME

Imported copper scrap offers remained steady across major origins, with LME cash levels guiding most price benchmarks. Australian origin material saw Brass Honey (2% impurity) at 63% of LME, Birch/Cliff at 94%, Candy/Berry at 97%, while Millberry continued to trade flat to LME.

UAE origin offers included Brass Honey (4% ME grade) at 64%, Millberry flat to LME (US/EU parity), and high-grade Druid around 91% of LME. US origin Copper Motors Mix was reported at $1,260, while US/EU origin Copper Barley was assessed at 98% of LME (CIF Mundra). Copper Cloves of US/EU origin were quoted near 95% of LME.

In contrast, domestic scrap markets have firmed. Indian yard owners have raised offers, supported by strong CCR rod demand, with most plants operating at 75-80% capacity. This has tightened local scrap availability and shifted pricing power toward domestic suppliers, as buyers increasingly prefer quicker local deliveries over volatile and uncertain import markets. Sources also indicated that a few new plants are expected to come up in the Uttar Pradesh region, which may further influence regional scrap dynamics.

Copper prices strengthened across the Delhi market, with armature scrap rising to INR 960,000/t, up 7.26%, secondary CCR wire rods increasing to INR 1,020,000/t, up 7.14%, and primary CCR wire rods edging higher to INR 1,080,000/t, up 2.95%.

Outlook

Imported copper scrap prices are likely to stay steady to slightly firm in the near term, supported by strong LME cues but limited by cautious Indian buying. Domestic scrap is expected to hold firm as CCR rod demand remains strong and yard availability stays tight. Unless LME prices maintain their rally or Chinese buying picks up, imported scrap may see only marginal upside.

Leave a Reply