- LME copper eases from recent highs; bid-offer gaps widen

- Selective procurement continues as price discovery challenges persist

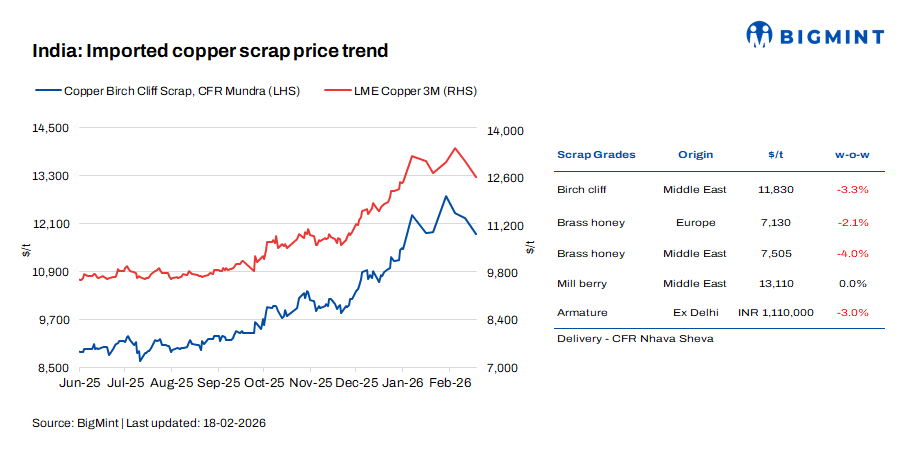

Imported copper scrap prices in India edged lower w-o-w in the week ended 17 February, mirroring a correction on the London Metal Exchange (LME). Domestic copper scrap prices also softened amid comfortable availability and subdued downstream demand.

According to BigMint’s assessment, Middle East-origin Birch Cliff scrap was assessed at $11,830/t CFR Mundra, falling by 3.3% w-o-w, while armature scrap prices fell 3% w-o-w to INR 1,110,000/t ex-Delhi. US motors mix prices also fell w-o-w to around $1,400/t CFR Mundra.

LME trend

LME copper prices corrected sharply during the week. The LME cash settlement fell from $13,172/t on 12 February to $12,561/t on 17 February, marking a decline of around 4.6% over the period. The three-month contract also dropped to $12,674/t from $13,239/t earlier in the week.

Meanwhile, LME copper stocks increased steadily to 221,625 t on 17 February, up from 196,650 t on 12 February, indicating rising exchange inventories and easing immediate tightness concerns.

Market insights

Domestic copper scrap prices witnessed a mild correction this week, tracking the downturn on the LME. Market participants indicated that comfortable availability of material in certain segments, coupled with subdued operational activity, has limited aggressive buying interest.

A trader source highlighted a growing preference for African-origin copper and brass scrap, citing better price viability compared to other supplying regions. Offers from alternative origins were heard to be uncompetitive for Indian buyers, restricting fresh deal closures from those regions.

In the US market, copper motor scrap was reportedly offered at around $1,450/t for large motors and $1,500-1,530/t for mixed motors. However, significant bid-offer disparities persist. While active buying interest from China and Pakistan has supported asking prices, Indian buyers are finding it difficult to secure material at workable levels, resulting in limited transactions.

Seller sources suggested that excess material availability in certain grades has kept prices on the softer side amid relatively muted demand. Despite ample supply in parts of the market, transaction activity remains selective rather than broad-based.

On the demand side, buyers pointed to challenges in price discovery, noting that offered prices have not aligned with their bid levels over the past week. This mismatch has reduced spot trading activity, as participants remain hesitant to commit without clearer pricing signals.

Another trader source indicated that “operational activity remains subdued, with average capacity utilisation hovering around 30-40%. Active procurement is largely confined to manufacturers facing immediate raw material requirements, while others continue to adopt a wait-and-watch approach.

Market participants are closely monitoring price movements on both the LME and the MCX of India for clearer directional cues before taking fresh positions.

Global scrap sentiment

In overseas markets, scrap sentiment remains weak but relatively stable. Rising LME inventories and softer futures have tempered bullish momentum, although sustained buying interest from select Asian markets has provided some support to exporters’ asking prices.

Overall, global scrap trade flows remain active but cautious, with sellers defending offers while buyers resist higher levels amid margin pressures.

Additional updates

BHP has outlined a global copper project pipeline that could lift its production capacity by 1.8-2 mnt over the next decade, with final investment decisions planned between 2026 and 2032 and start-ups from 2028 onward. Its major Copper South Australia Phase 1 and 2 projects are expected to add 790,000-910,000 t between 2029 and 2038. The company maintained FY’26 copper production guidance at 1.9-2 mnt and recently invested $555mn to expand South Australian operations. BHP estimates that an additional 10 mnt/yr of new capacity will be required globally by 2035 to address supply gaps, projecting demand growth from 34 mnt in 2026 to over 50 mnt by 2050. Similar deficit concerns have been flagged by South32, Cochilco, and Nornickel.

Outlook

Copper demand continues to offer underlying structural support. However, rising exchange inventories, subdued operating rates, and persistent bid-offer gaps are likely to keep prices rangebound in the near term. Short-term movements may remain sentiment-driven, with volatility closely tied to LME price fluctuations and speculative positioning rather than any immediate physical supply constraints.

Leave a Reply