- Domestic scrap prices firm across major grades

- Year-end slowdown weakens scrap buying activity

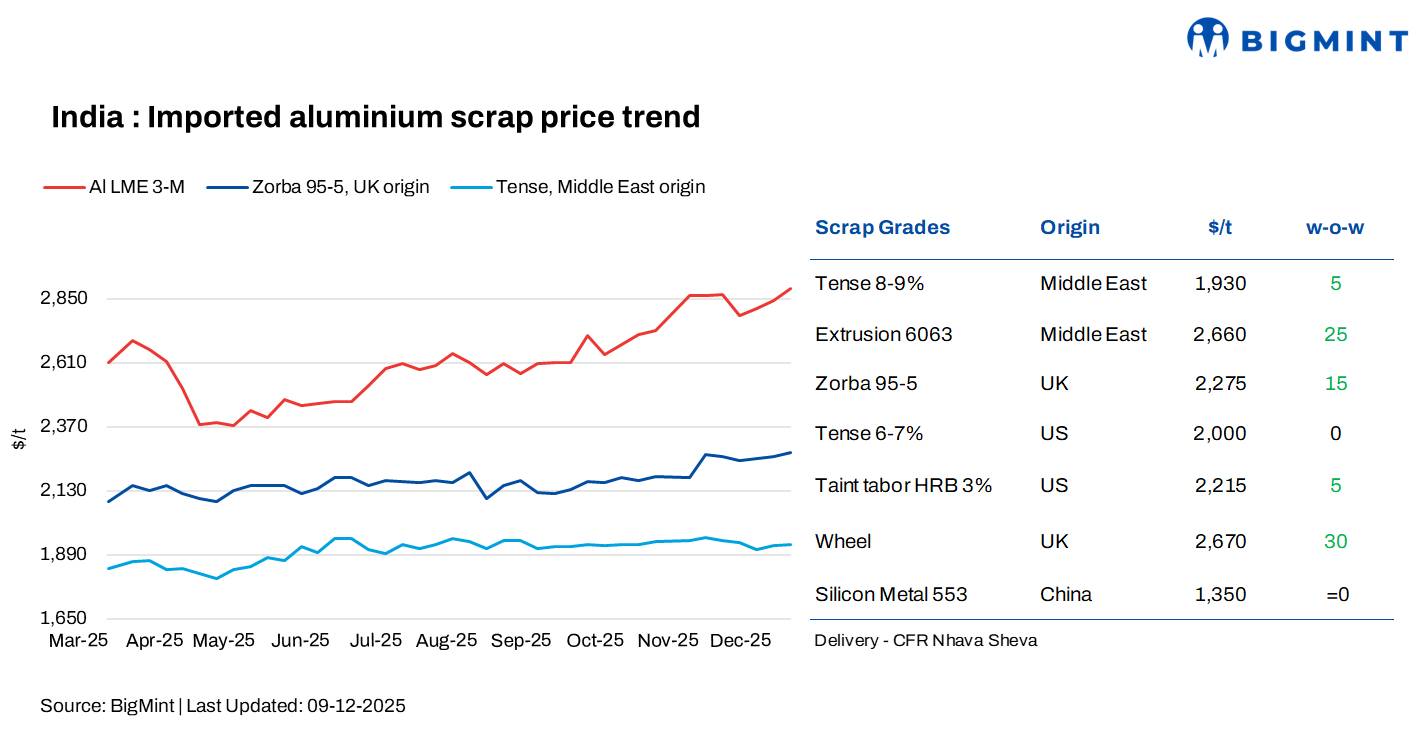

India’s imported aluminium scrap prices saw an uptrend w-o-w in the week ended 9 December, following an increase in prices on the London Metal Exchange (LME). BigMint assessed UAE-origin Tense (8-9%) at $1,930/t, up by $5/t w-o-w, while US-origin Tense (6-7%) remained unchanged at $2,000/t.

UK-origin Zorba 95/5 was assessed at $2,275/t, rising $15/t w-o-w, whereas US-origin Taint Tabor HRB (3%) increased by $5/t to $2,215/t. Meanwhile, UAE-origin Extrusion 6063 climbed $25/t to $2,660/t, and UK-origin Wheel rose $30/t to $2,670/t w-o-w.

LME prices increase w-o-w; inventories fall

At the close on 8 December, LME aluminium prices stood at $2,897/t, rising by $13/t from $2,884/t recorded on 1 December. Meanwhile, inventories at LME-registered warehouses declined to 525,800 t, down 12,100 t from 537,900 t a week earlier, reflecting tightening supply conditions.

Aluminium prices on the LME moved higher w-o-w as tightening supply aligned with firmer demand signals. The market gained strength through the week, supported by steady upward momentum. Inventories posted minor declines, reinforcing concerns about limited near-term availability. Supply remained constrained by capacity limits at Chinese smelters, lower exchange stocks, and global production disruptions, while demand sentiment improved on the back of stronger import flows into China and healthy export activity earlier in the year. Together, these factors lifted market confidence and supported the overall rise in aluminium prices.

Market insights

Imported aluminium scrap prices have strengthened in line with the uptrend in LME aluminium. The rise in LME prices, supported by tightening global supply conditions and growing expectations of US Fed rate cuts in December, has pushed benchmark levels higher. In turn, this has kept imported scrap offers across major grades elevated.

Buying activity remains weak as year-end seasonality slows market participation. With only a few weeks left in the year, trading activity has softened, especially as suppliers across Western regions prepare for winter holidays, during which shipments typically pause until after the New Year. This has resulted in quieter negotiations and limited buying interest.

In the Indian market, demand has also eased, partly because several auto manufacturers are expected to undertake planned maintenance shutdowns during December. This is likely to keep procurement subdued and overall scrap consumption lower through the month.

Despite the softer buying environment, domestic aluminium scrap prices have moved higher w-o-w across most grades, in line with the rise in imported scrap offers. Casting scrap prices have also increased in both Delhi and Chennai, supported by steady downstream requirements.

On the macroeconomic front, markets are closely watching the upcoming US Federal Reserve meeting in 9-10 December. Traders widely expect a 25-basis-point rate cut, which could offer short-term support to industrial sentiment by easing borrowing costs.

However, its immediate impact on metals demand may remain limited, as broader manufacturing momentum and supply-side developments continue to weigh on near-term market dynamics.

China silicon

According to BigMint’s assessment, China’s 553-grade silicon prices remained stable at $1,350/t CFR Mundra.

Outlook

Aluminium scrap prices are likely to continue a steady rise over the course of December, supported by higher LME prices and tightening global supply, even as buying interest stays muted due to year-end seasonality and holiday shutdowns. Imported scrap availability in India may tighten further as Western suppliers pause shipments, while domestic demand is expected to stay soft until auto-sector operations normalise in early January.

Any confirmation of a US Fed rate cut could lend mild sentiment support, but meaningful demand recovery will likely unfold only after year-end slowdowns ease and manufacturing activity picks up. Overall, the short-term outlook points to an uptick in prices, with limited downside risk as supply constraints keep a high floor under prices.

Leave a Reply