- Rupee at record lows dampens buying activity

- Tight Tense scrap supply supports domestic prices

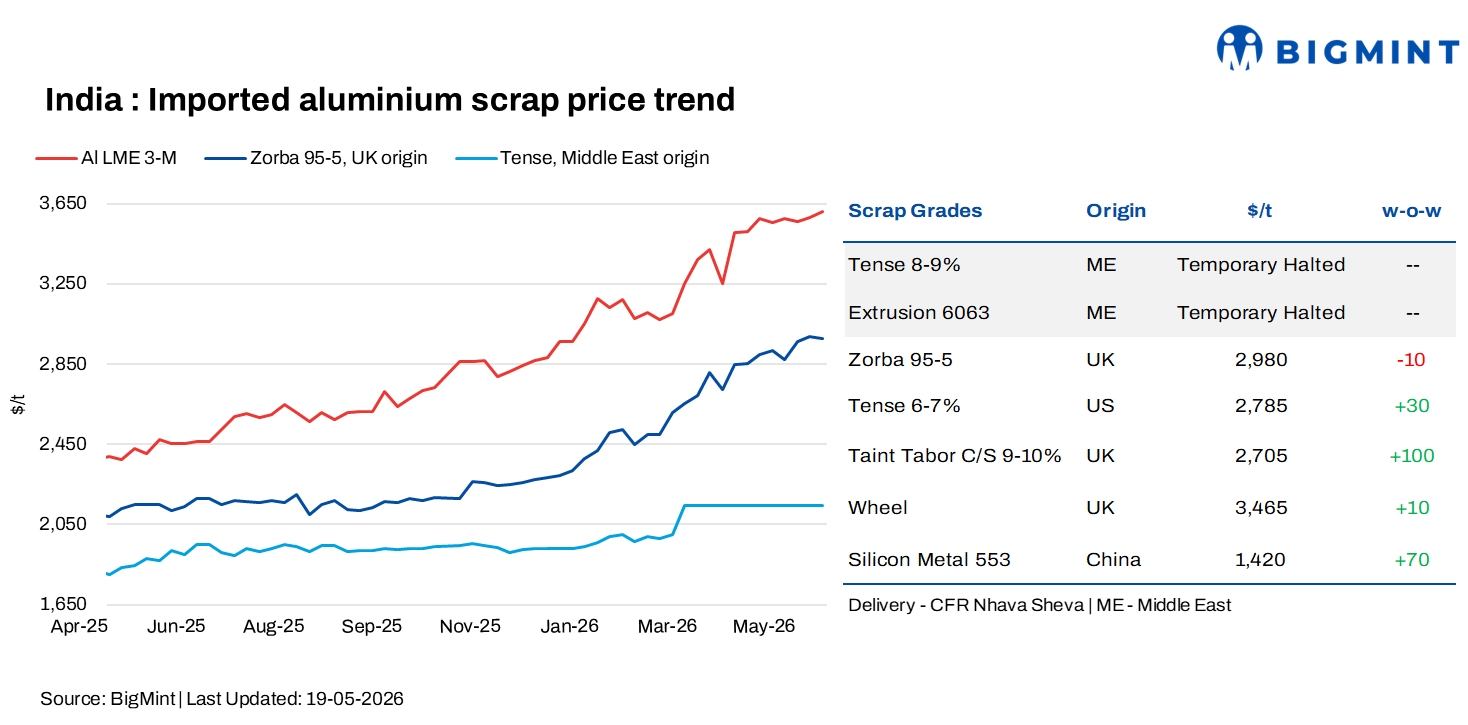

India’s imported aluminium scrap prices traded mixed w-o-w as of 19 May 2026 despite elevated London Metal Exchange (LME) aluminium prices and continued volatility in the global scrap market.

According to BigMint’s latest assessment for CFR Nhava Sheva deliveries, UK-origin zorba 95-5 scrap declined by $10/t w-o-w to $2,980/t from $2,990/t previously, reflecting relatively softer buying interest in the imported shredded scrap segment.

Meanwhile, US-origin tense 6-7% scrap increased by $30/t w-o-w to $2,785/t from $2,755/t last week, supported by relatively firm demand in the imported aluminium scrap market

LME aluminium rises w-o-w

Three-month aluminium prices on the London Metal Exchange (LME) traded higher w-o-w, closing at $3,602/t on 19 May 2026 against $3,580/t on 12 May 2026, up by $22/t. Prices remained volatile during the week, rising to $3,666/t before easing in subsequent sessions amid profit booking after the recent rally.

Market sentiment remained supported by tightening visible stocks, elevated LME cash prices and continued ex-China supply tightness. Easing China-US trade tensions and persistent concerns over potential Middle East supply disruptions also supported broader aluminium market sentiment, although high Chinese inventories and macroeconomic caution continued to limit sharper upside in prices.

Meanwhile, LME aluminium inventories declined by 15,200 t w-o-w to 340,575 t from 355,775 t over the same period , indicating continued stock drawdowns across exchange warehouses and reinforcing tightness in the physical aluminium market.

Market scenario

Imported aluminium scrap market sentiment remained subdued, with limited trading activity across regions despite a w-o-w increase in LME aluminium prices. Demand conditions continued to stay weak amid ongoing uncertainty linked to the global oil and gas situation, elevated energy costs, and geopolitical tensions in the Middle East. Sentiment was further impacted by the sharp depreciation in the Indian rupee, which recently touched a record low of around INR 96.96 per US dollar and is now moving close to the INR 97 mark amid rising crude oil prices and persistent external market pressure. Domestic aluminium scrap prices, however, continued to remain firm due to tight material availability across the market, preventing any major correction in rates.

Buying activity stayed cautious, with market participants largely postponing fresh procurement amid uncertainty surrounding LME direction, volatile exchange rates, and expectations of further price fluctuations. Market participants also expect conditions to weaken further from June onwards as the broader impact of the ongoing geopolitical conflict begins reflecting more visibly on industrial demand, manufacturing activity, and global trade flows.

On the domestic front, aluminium prices remained elevated, while scrap availability stayed tight across both northern and southern India, particularly for casting-grade Tense scrap amid acute supply shortages. Secondary producers continued to face procurement challenges and margin pressure due to higher replacement costs and rupee depreciation, resulting in cautious buying behaviour and subdued operating rates across the secondary aluminium industry.

Chinese silicon prices

According to BigMint’s latest assessment, China-origin silicon metal 553 prices increased by $70/t w-o-w to $1,420/t on a CFR Mundra basis as of 19 May 2026, compared with $1,350/t last week, supported by relatively firm import offers and improved market sentiment.

Outlook

Imported aluminium scrap prices in India are expected to remain firm in the near term amid tight scrap availability, elevated LME aluminium prices and continued rupee weakness. However, cautious buying activity and weak downstream demand may limit sharp upside across the market.

Leave a Reply