- Falling inventories, production disruptions lift LME prices

- Market remains cautious amid potential Hormuz blockades

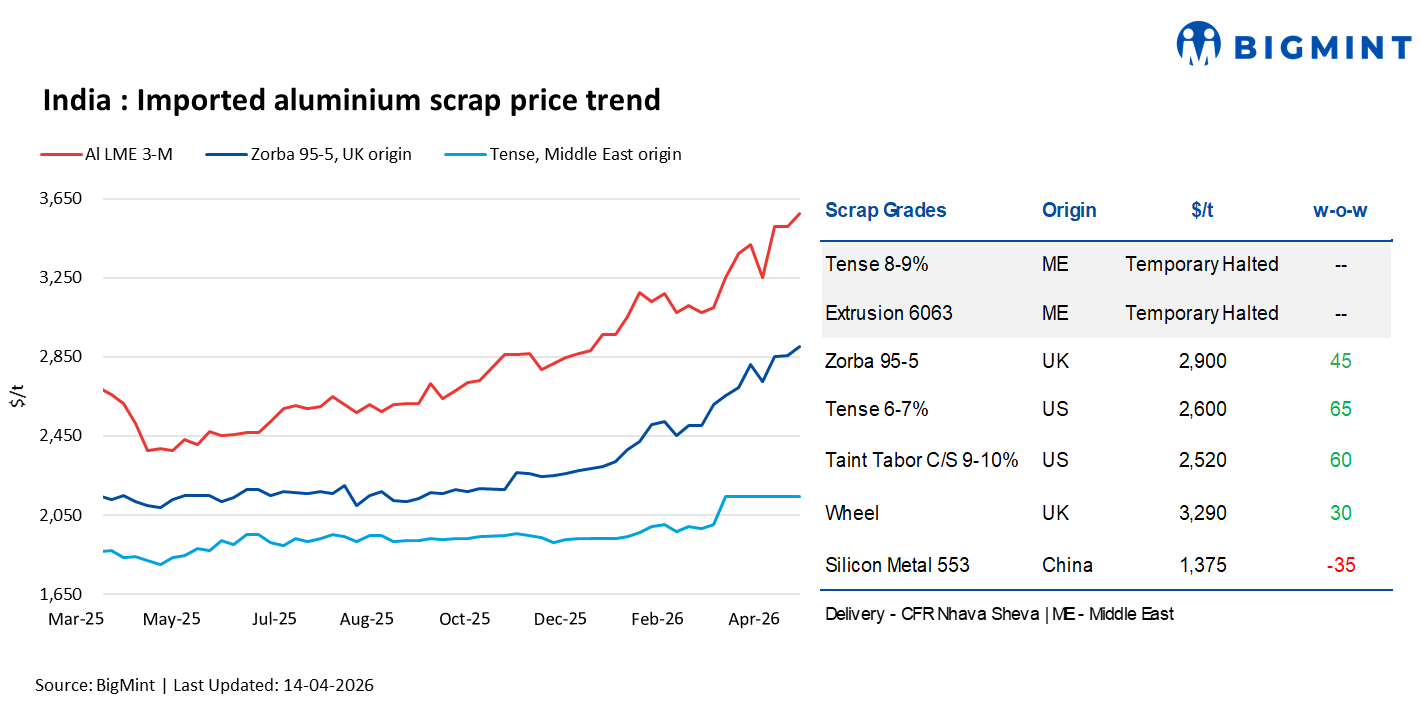

India’s imported aluminium scrap prices strengthened w-o-w on 14 April 2026, tracking an uptrend on the London Metal Exchange (LME), supported by ongoing geopolitical tensions and constrained global supply.

As per BigMint’s latest assessment for CFR Nhava Sheva deliveries, UK-origin Zorba 95-5 scrap increased by $45/t w-o-w to $2,900/t, while US-origin Tense 6-7% scrap also rose by $65/t w-o-w to $2,600/t.

LME aluminium strengthens w-o-w

Three-month aluminium prices on the LME strengthened by $62/t to $3,571/t on 13 April 2026 from $3,509/t on 7 April 2026, reflecting a firmer underlying market tone.

In parallel, aluminium inventories on the exchange declined by 12,800 t to 397,100 t from 409,900 t over the same period, indicating a drawdown in stocks alongside the price gains.

Market scenario

Indian imported aluminium scrap markets remained largely subdued, with limited active trade and muted participation across regions.

Sources indicated that sentiment continues to be weighed down by ongoing logistical constraints and intermittent disruptions, including restricted flows via the Strait of Hormuz route, which has kept import availability tight.

Participants are also adopting a cautious approach to assess the impact of recent blockades, while supplier-side activity remains limited due to external commitments and travel-related factors. Additionally, some participants stated that they are not receiving offers from suppliers.

Domestically, aluminium prices have surged in line with stronger LME cues, while scrap markets remain tight, particularly for casting-grade Tense scrap, amid acute supply shortages.

Secondary producers continue to face procurement difficulties, resulting in cautious buying activity and subdued operating rates.

In Chennai, Tense scrap offers were at INR 298,000-305,000/t, while bids were lower at around INR 285,000-290,000/t, highlighting the persistent supply tightness and constrained import availability.

Chinese silicon prices

According to BigMint, China-origin silicon metal 553 prices decreased w-o-w by $35/t to $1,400/t from $1,375/t on a CFR Nhava Sheva basis.

Outlook

Imported scrap markets are likely to remain firm in the near term, supported by elevated LME aluminium prices and tight global supply conditions. However, liquidity may stay limited amid ongoing logistical disruptions and cautious buyer sentiment. Domestic scrap availability is expected to remain constrained, keeping spreads firm and supporting secondary aluminium prices.

Leave a Reply