- Firm LME prices, bid-offer gaps slow down trade

- Market expected to recover after Diwali festival

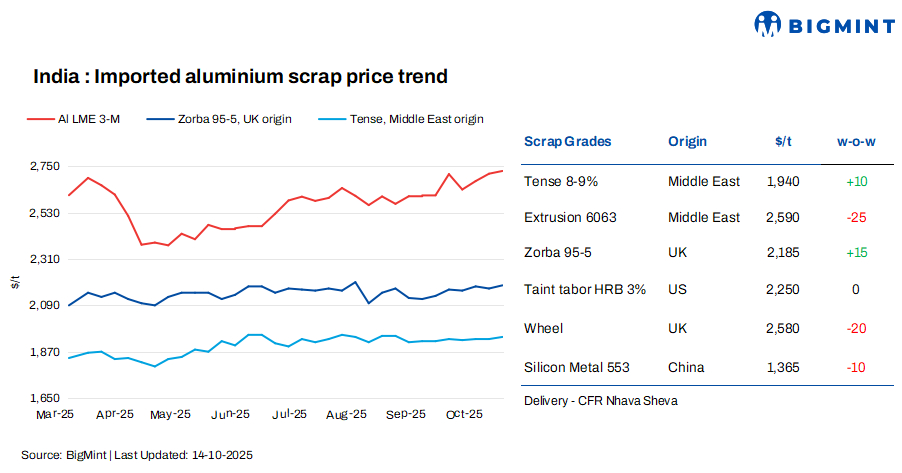

India’s imported aluminium scrap prices saw mixed trends w-o-w, though London Metal Exchange (LME) benchmarks witnessed positive movements. BigMint assessed UAE-origin Tense scrap at $1,940/tonne (t), up by $10/t w-o-w, while US-origin Taint Tabor HRB (2-3%) remained stable at $2,250/t.

UK-origin Zorba 95/5 increased by $15/t w-o-w, while UAE Extrusion 6063 dropped by $25/t and UK-origin Wheel fell by $20/t w-o-w.

LME aluminium prices rose to nearly a 3.5-year high during week 41 of CY’25. The price rise was primarily driven by renewed optimism in global commodity markets following the US Federal Reserve’s 50-basis-point rate cut. The rate cut boosted investor sentiment and lifted overall commodity prices, including those of base metals.

LME prices increase w-o-w; inventories decline

At the time of reporting, LME aluminium prices stood at $2,774/t, up by around $61/t as compared to $2,713/t last week.

Meanwhile, aluminium inventories at registered warehouses declined by 1,300 t to 506,000 t from 507,300 t in the previous week.

Market insights

The imported aluminium market remained extremely sluggish, with almost no active buying at present. Traders were largely inactive unless they were direct suppliers to factories. Of those active, most buyers focused on sourcing cheaper materials from regions such as Malaysia, Israel, and the US, as Middle East-origin offers were not competitive.

Extrusion exports from the UAE also slowed sharply, with only around 10% of the usual volume currently moving. Overall, trading sentiment was weak, and market participants expect the market to stay subdued until after Diwali, when some recovery in buying interest is anticipated.

The domestic aluminium market remained largely subdued this week. Most buyers preferred domestic scrap, with imported material purchases limited to need-based buying. Despite several high offers in the market, deals failed to materialise as bids were lower and overall buying interest remained weak.

With LME prices firm but local markets under pressure, many importers faced a cash crunch and paused or delayed purchases. Market participants noted that current price fixations at existing aluminium levels are resulting in losses, as arriving containers are priced 2-3% higher, while local prices remain below cost.

Overall, trading activity was minimal, with no major deals heard. Shippers sought higher prices compared to previous levels, but the local market continued to resist. Market participants expect some improvement in demand and activity after Diwali.

Domestic Tense scrap prices edged lower to INR 191,000-192,000/t across northern and southern India, pressured by improved supply, as scrapyards liquidated inventories before the quarter-end.

In the Extrusion segment, prices rose by INR 2,000/t w-o-w to INR 217,000/t ex-Delhi, supported by steady demand from the automotive and construction sectors. However, ongoing BIS inspections at extrusion units led buyers to remain cautious about placing large-volume orders.

India’s aluminium ADC12 alloy ingot prices saw a slight m-o-m increase in October 2025, primarily due to the positive auto demand following the cuts in GST. The recent increase in ADC12 offers in India has been driven by a surge in auto sales during September, particularly following the government’s GST 2.0 reforms.

BigMint’s monthly assessment for OEM-grade ADC12 showed firm pricing across key regions:

- Delhi: INR 230,000/t, up by INR 1,500/t m-o-m

- Pune: INR 230,000/t, an increase of INR 2,000/t m-o-m

- Chennai: INR 231,000/t, up by INR 500/t m-o-m

Silicon price trends

According to BigMint’s assessment, silicon 553 prices from China declined by $10/t w-o-w to $1,365/t CFR Mundra, due to softening demand amid the ongoing Chinese holidays, along with improved availability from Chinese producers.

Outlook

The aluminium market is expected to remain subdued in the near term, with limited buying activity and cautious sentiment among traders. However, post-Diwali, demand is likely to pick up modestly, supported by steady automotive and construction sector requirements. Imported scrap may see selective buying, especially from cost-competitive regions, while domestic Tense scrap and ADC12 ingot prices could stabilise as inventory liquidations ease. LME trends and global investor sentiment will continue influencing price movements, but overall market recovery is expected to be gradual.

Leave a Reply