- Domestic market quiet at the start of new fiscal

- Price adjustments expected post-Eid holidays

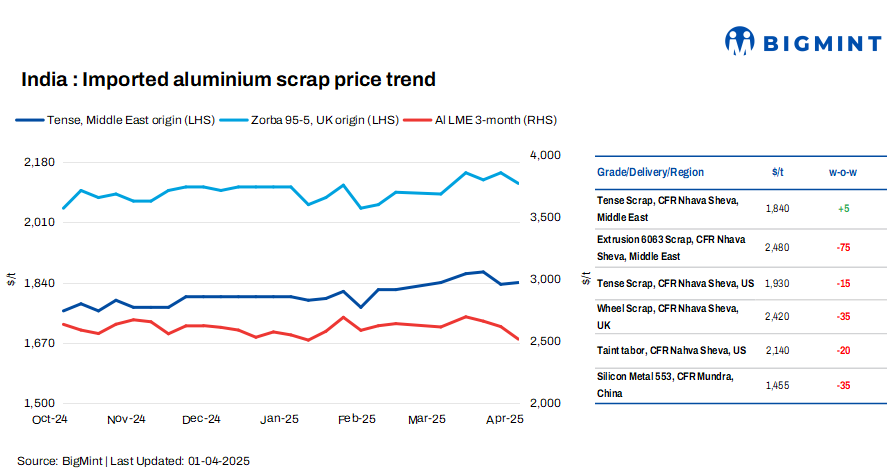

India’s imported aluminium scrap prices remained range-bound week-on-week (w-o-w) despite the previous drop of up to $75/tonne (t).

BigMint’s assessment of Tense scrap from the US was steady at $1,930/t, while Wheels from the UK were also stable at $2,420/t, both CFR west coast, India.

This week, aluminium prices on the London Metal Exchange (LME) decreased by 5% to $/t from last week’s $2,662/t. Meanwhile, stocks at LME-registered warehouses stood at 462,450 t, down 3.7% from 480,250 t last week.

Domestic scrap prices dip w-o-w

In the domestic market, Tense scrap prices in both Delhi and Chennai inched down by INR 1,000/t compared to last week. According to BigMint’s assessment, domestic Tense scrap stood at INR 187,000/t ex-Delhi-NCR and INR 187,000/t ex-Chennai.

Market sentiments

Following the conclusion of the financial year, domestic market activity remains quiet, with buyers adopting a cautious stance as they wait to for price trends to emerge.

With the start of the new fiscal year, the aluminium scrap market is anticipated to stabilise further, though short-term activity will remain limited. Following the Eid holidays, the imported scrap market is expected to experience price adjustments.

According to a source, “The official notice of scrap export ban from Saudi Arabia may be released soon, impacting the flow of non-ferrous scrap, as this region is the third-largest source of scrap for India. Additionally, reports indicate that the expected percentage of red and yellow metals in the US and UK Zorba is currently not being met, with these metals either in lower quantities or entirely absent. This shortfall is largely due to a significant decline in automobile shredding in both regions, driven by the Trump tariffs, which has led many to stop selling their old vehicles.”

Additionally, US Taint Tabor scrap is not being offered, due to higher domestic demand in the US.

The quality of EU/UK TT scrap has deteriorated, with reports indicating an increase in attached materials. As a result, claims for such scrap have become more difficult to process.

Meanwhile, the primary players are bidding significantly low for UBC scrap, offering terms with a one-week credit payment. Additionally, there is a shortage of UBC Taint/Tabor in local markets.

Sources stated that “Suppliers are currently experiencing significant delays in the release of export VAT by the government and are prioritising the domestic market to meet robust demand.”

Recently, a deal for 40 t of extrusion 6063 scrap from Australia was traded at 83% LME and Talk at 54% for 40 t, CIF Chennai.

Chinese market updates

According to BigMint’s assessment, prices of China’s 553-grade silicon decreased by $35/t w-o-w, reaching $1,455/t CFR Mundra. Additionally, freight rates for a 20-ft container from China to Mundra were recorded at approximately $1,650.

Outlook

In the near term, the market outlook will depend on the resumption of normal trading activities and potential price shifts following Eid.

Leave a Reply